Start every trading day with a quick, actionable snapshot of global markets, key earnings, and the biggest movers across US, Europe, and Asia. Get the insight before your first coffee is gone.

April 10, 2024 | Issue 58

The Best Investment to Outpace Inflation in 2024

Nikolay Stoykov

Managing Partner at Alaric Securities

Balancing Risk and Reward

The best investment in 2024’s shifting landscape amid Federal Reserve rate changes. In December 2023, the Federal Reserve indicated they would gradually lower rates, confirmed in March 2024 despite inflation above the 2% target.

Performance of Global Equity Markets

Global equity markets surged: the S&P500 is up 28% over the past year, the German DAX rose 22% in 12 months, and the NASDAQ-100 soared 43% over the year.

The S&P500 is up 28% over the last year and 10% year-to-date. The German DAX is up 22% over the previous 12 months and similarly 10% on a year-to-date basis. Some sectors, like the technology-heavy NASDAQ-100, are showing even better performance – 43% for one year and 9% year-to-date.

Clearly, the train has left the station. Gone are the days when one could reasonably expect a pull-back, and most volatility indexes indicate that investors should not expect significant market volatility anytime soon. So, what should investors do? Clearly, the option to jump and try to catch the fast-moving train is there, but the danger of overpaying is quite real. Yes, equities are and most likely will always be an attractive asset class, but not at any price.

The surprising fact about this equity rally is that while it was driven by the expectations of lower interest rates in the future, the very same interest rates in both the US and the Euro Area are higher! The US 10-year yields were 3,5% a year ago and 3,85% at the beginning of the year, while they are 4,2% at present:

The 10-year German rates were 2,35% a year ago and 2,03% at the beginning of the year, while they currently stand at 2,30%:

Clearly, interest rates are high. They have never been so high, not only on a 10-year basis but also when looked at on a 20-year basis, at least in the US.

However, since returns are fixed, could inflation return and “eat” into those high nominal returns?

That is possible but highly unlikely. As we wrote in our article Inflation-Linked Bonds, the expectation for inflation in the US is 2,4% per year for the next 2 years, while those for Europe were 1,8% per annum for the same period.

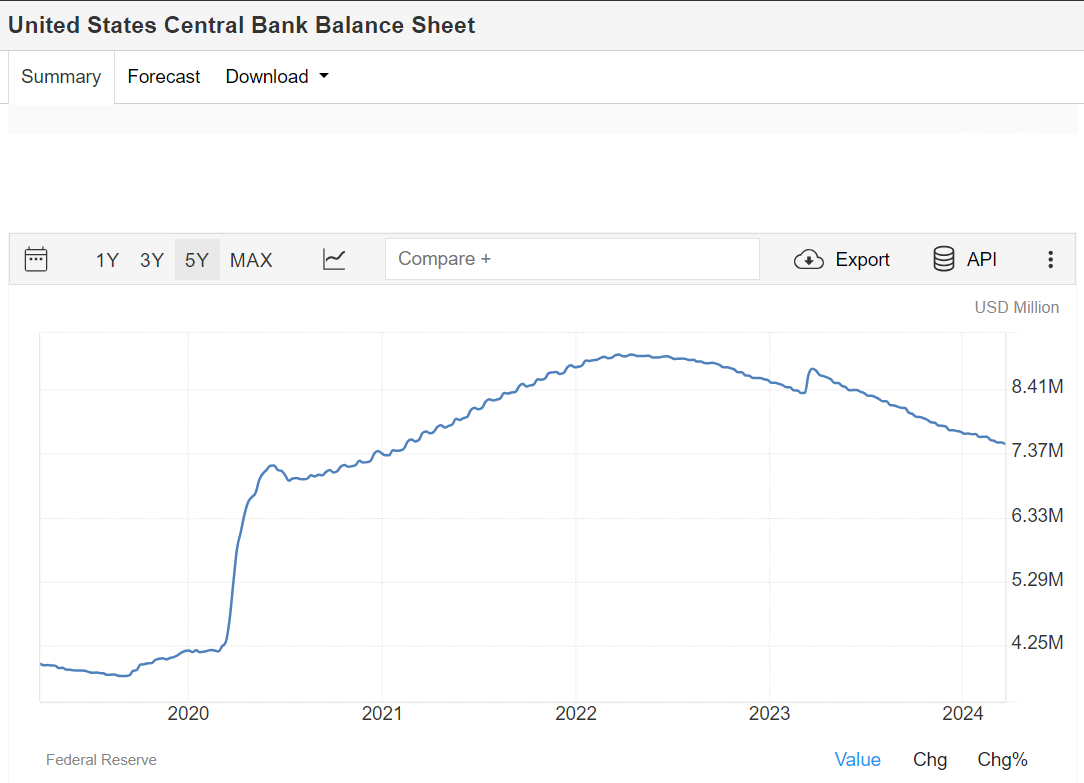

Central Bank Balance Sheets as Indicators

Human beings, however, tend to be visual creatures – as they say, a picture is worth a thousand words. We will look at the Central Bank’s Balance Sheets.

Let’s start with the Federal Reserve Balance sheet.

The Fed is serious about fighting inflation.

There has never been a pattern of runaway inflation while the Central Bank is reducing the size of its balance sheet. And that reduction is substantial – from 8,92 Trln USD to 7,51 Trln USD or nearly 16%..

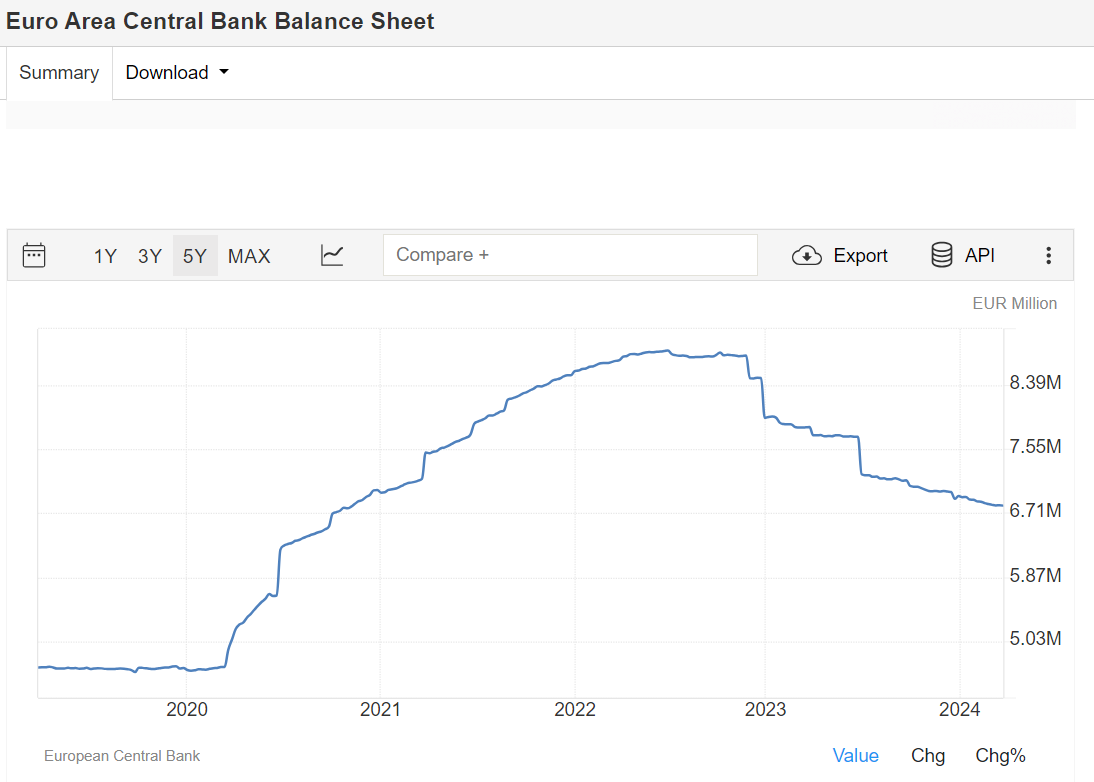

And what about the ECB? Here it is:

If you are impressed by the efforts by the Fed to contain inflation, you for sure might be in disbelief at how even more forceful had the ECB been. The size of its balance sheet is down from 8.81 Trln EUR to 6.81 Trln EUR – or nearly a 23% reduction.

The Best Investment in the Current Landscape

While it appears that inflation will be effectively managed, the window for significant equity investments may have closed due to increased risks. However, the fixed-income market presents compelling opportunities when considering value and risk. We believe that Romanian Government Bonds stand out as the most attractive assets in this space.

On our investment platform for retail investors at www.alaric.bg, we offer a range of Romanian government bonds with varying maturities. While one matures in just 6 months and may not offer the best value, the others are particularly appealing. This is especially true given that expected inflation in Europe is projected to remain below 2% for the next two years. The remaining two Romanian government bonds available on our platform offer yields of 3.55% maturing in October 2025 and 4.09% maturing in March 2028.

It is not an income that you will be able to comfortably retire but it is an yield that for sure offer returns above the expected inflation.

Disclaimer

The articles, podcasts, and newsletters from Alaric Securities OOD solely represent the authors’ views affiliated with the company. They do not mean the perspectives of Alaric Securities OOD or any of its subsidiaries or affiliates. They are provided for informative purposes and do not constitute recommendations for or against purchasing or selling security. Digital assets (such as cryptocurrency) or other assets in any account. They are neither research reports nor meant to be the foundation for any investing decisions. Any third-party information given does not represent the views of Alaric Securities OOD or any of its subsidiaries or affiliates. All investments carry risk, including the potential loss of principal, and past success does not assure future success.

Stay Ahead with Alaric Securities Newsletters

Traders and investors don't need more information - they need better information. That’s what we deliver!

Step back from the daily noise. Each issue explores market trends, industry shifts, trading opportunities, and exclusive updates — learn what's shaping the markets, not just what's trending online. Ready to get the edge?