Opinion: These 7 Stocks Could Profit Handsomely from a Cashless Future

My kids constantly remind me how fast technology moves. The latest instance was when I said something about the telephone poles by the side of the road.

My 7-year-old asked, “Why do they call them telephone poles?”

There are plenty of other examples of my kids asking a question and I say without a hint of irony that “when daddy was a kid, a long time ago,” people had to use crazy things like encyclopedias or paper road maps that were impossible to fold.

Soon, the old phrase “cash is king” may be one of those old-timey sayings that kids can’t intuitively understand. In the very near future, the idea of cash — tangible paper money — may be as much of an anachronism as landline telephones.

Digital research firm eMarketer estimates that mobile payment apps that don’t use a traditional financial institution — dubbed peer-to-peer payments systems — will process $120 billion in transactions this year, up 55% from the prior year. That figure is forecast to double by 2021.

This is a global phenomenon, and not just one of those overhyped fads of Silicon Valley futurists. Last year, the New York Times ran a piece about the rise of mobile payments in Asia with the headline “In Urban China, Cash is Rapidly Becoming Obsolete” as estimates for these kinds of payments has hit a $5.5 trillion annual pace — 50 times that of the U.S.

Most importantly for investors, of course, is the profit potential. Just look at the April acquisition of VeriFone PAY for an instant 50% premium as evidence of the opportunity in mobile payments.

While the evolution of landline telephones to iPhones is already behind us, the mobile-payments revolution is still in its early stages. And that means more big winners are still out there.

For investors who want to play this trend, here are seven mobile payments stocks to consider.

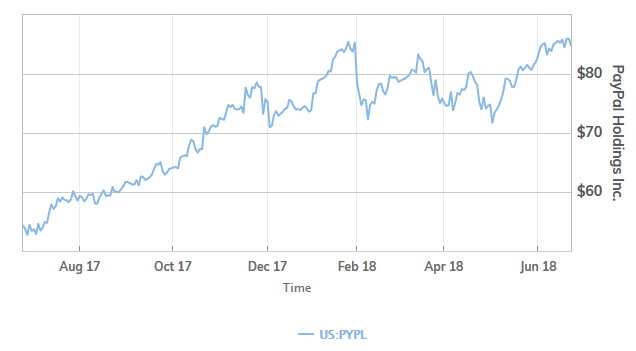

PayPal

An oldie but a goodie in the mobile payments game, PayPal PYPL is in many ways at the forefront of cashless transactions in the 21st century. The platform was one of the first digital-first providers to offer bank-like solutions such as sending money and processing payments. In fact, the mobile and cashless angle of this property was so compelling and the growth so impressive that eBay EBAY, spun off the outfit in 2015 so it could more efficiently focus on this payments mission.

Across its various properties, which include Venmo and Xoom, PayPal now boasts 227 million accounts worldwide and processes $2.2 billion transactions worth about $130 billion each quarter. And most importantly, PayPal is focused on the cashless future without the baggage of a legacy banking operation.

No wonder PayPal stock is up 140% since its July 2015 spinoff vs. just 32% for the S&P 500 SPX, and just under 50% for former parent eBay in the same period.

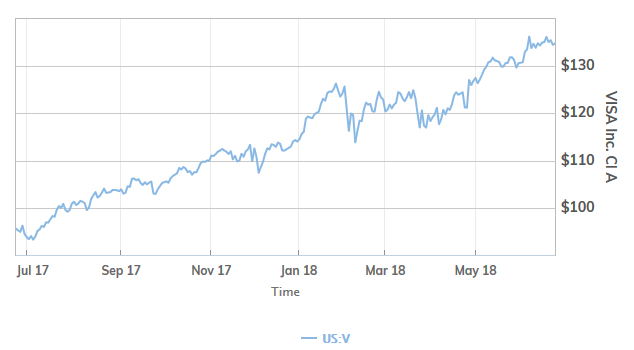

Visa

With a rather ill-timed IPO in 2008, you’d think that payments processor Visa V, would have run into trouble in its early years as a public company. Nothing could be further from the truth, as shares hung tough in the Great Recession thanks to strong growth metrics and have powered higher over the last several years. That puts this stock up about 750% since its debut about 10 years ago, vs. about 110% for the S&P 500 in the same period.

And with profit surging sixfold in the most recent quarter, momentum certainly isn’t slowing down.

With total payments processed tracking about $2 trillion each quarter and recent partnerships with PayPal to bolster its mobile offerings, this company is a force to be reckoned with in a cashless age. Its brand is unmatched and the general move away from cash and toward plastic or mobile payments creates a great tailwind for this $300 billion powerhouse.

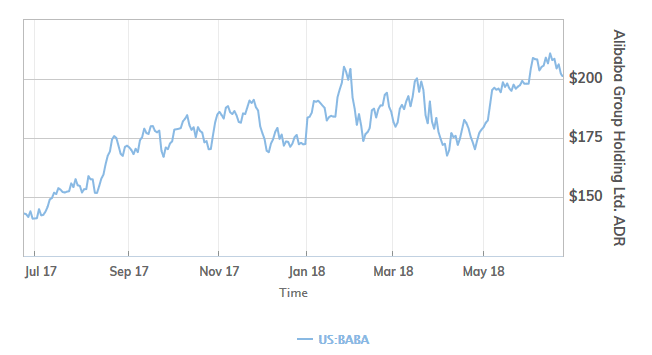

Alibaba

Alibaba BABA is already a technology powerhouse on many fronts, including e-commerce and online advertising, but investors shouldn’t shortchange its mobile-payments potential. A United Nations report last year pegged payments through Alibaba’s Alipay interface at $1.7 trillion — 23 times higher than just four years ago.

The massive scale of Alibaba in China is a huge leg up on the competition. That’s because culturally, this region is so much better equipped for a cashless future as e-commerce platforms, social media and other platforms have willingly embraced mobile payments to help make them ubiquitous.

There are undoubtedly challenges and risks inherent in emerging markets. But in the case of mobile payments, the lack of legacy financial products and the absence of deep-pocketed financial giants incentivized to keep consumers on the old model has allowed Chinese mobile payments — and Alipay — to thrive.

Apple

While admittedly lagging behind China, western markets where the iPhone is ubiquitous have provided ample runway for Apple AAPL mobile-payments technologies. Apple Pay is used by 127 million iPhone users worldwide, and the continued dominance of the Apple brand gives this tech company a massive springboard to expand this platform over time.

Detractors note that only about 16% of iPhone users bother to deploy Apple Pay — hinting at a reluctance that may be hard to overcome. However, it’s hard to tell if that low figure is because of challenges with broader customer perceptions about mobile payments or about the specifics of the Apple product itself.

History has shown it’s not exactly wise to bet against Apple in the long run, and the continued evolution of Apple beyond the hardware uprgrade cycle and instead focusing on “services” revenue from its installed user base hints that Tim Cook & Co. are serious about making this mobile payments product work.

Mastercard

Mastercard MA is in many ways the forgotten little brother of Visa and American Express AXP with most consumers finding this logo in their wallets less frequently. But don’t count out Mastercard stock, with a $200 billion market value and operating cash flow north of $5 billion annually.

Mastercard is hungry for an edge, with a very aggressive stance to adopt the blockchain tech that has become so captivating in the age of bitcoin and cyptocurrencies. This began last year, as the company allowed customers to use blockchain instead of swiping their Mastercard-branded cards to transact. At the Money20/20 conference in Amsterdam, a Mastercard executive boasted that the company has built blockchain technology that can run its whole network, providing security and portability of transactions around the world.

From hiring engineers to opening up access to its blockchain API, Mastercard is one of the few big players to openly chase blockchain as a key part of its cashless future. That could give it an edge over the competition if the broader appeal of this tech continues to grow and move it from a fad to widespread adoption.

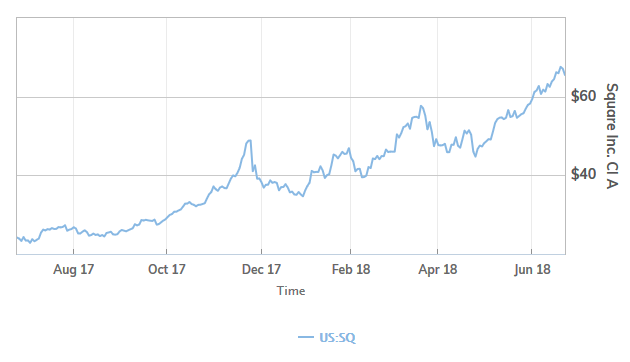

Square

This company has long been investors’ go-to name for riding the mobile payments revolution. Aside from a few months around the company’s November 2015 IPO, where investor interest seemed tepid, it has been off to the races; Square’s stock SQ is up 400% since entering the public market vs. just 30% for the S&P 500 in the same period.

There’s good reason for that, too, as growth shows no sign of slowing down. In its most recent earnings, Square reported that revenue jumped 51% — objectively impressive, and up from a 47% year-over-year rate the prior quarter. The company also has moved into consistent profitability, and is still aggressively expanding its offerings, such as a recent effort to help smaller companies launch omnichannel sales operations via a partnership with e-commerce engine Weebly.

The growth is real, and after finally achieving consistent profitability it is clear that Square stock is a front-runner in the mobile payments age for a reason.

Fiserv

Though not a household name, Fiserv FISV is a $30 billion payments-technology company that all investors should make note of, not the least of which because the stock is up an impressive 250% or so in the last five years, compared with about 70% for the broader S&P 500 index.

So what exactly does Fiserv do? In an nutshell, it’s a technology company that provides the platform for financial-oriented businesses to succeed in a digital age. With clients that include big-time banks, small credit unions, insurance companies and plenty of institutions in between, it is well connected across the sector and fuels everything from payment processing to risk management to customer-relationship-management tools.

Consumers may never know this company exists on the back end. However, if you’d prefer not to go all-in with a front-end payments processor, then consider a stock that is helping financial institutions of all sizes meet the challenges of a cashless and mobile age.

Article nad media was originally published by Jeff Reeves at marketwatch.com