Opinion: 5 gold stocks favored by fund managers today

If the U.S. economy softens, many of the forces hurting gold will reverse themselves.

Gold-mining investors who are smug because their stocks handily doubled or more this year got smacked this week.

The Market Vectors Gold Miners GDX, +0.70% exchange traded fund (ETF) was down almost 15% Wednesday, compared with last Friday. Companies including Barrick Gold Corp. ABX, +0.58% were down even more.

The question now is: Is it time to buy these stocks for a rebound and continued run?

It all comes down to your view of the economy and, therefore, what the Federal Reserve does next and when.

If, like me, you don’t believe any amazing improvements in the economy are on the way — and that this will curb the Fed’s enthusiasm for a December interest-rate increase — then gold and miners are now a buy.

To see why, it helps to know why the group just got hammered. There were three main catalysts this week:

- The European Central Bank suggested it might ease off on tapering its stimulus earlier than expected.

- A few Fed members were out giving hawkish speeches, apparently tilting the odds toward a December rate hike.

- There was speculation that the timeline for Brexit will narrow.

All of this boosted bond yields and the dollar, a negative for gold and miners.

That’s because as interest rates rise, gold becomes less of a “cost-free” investment from when money is cheaper, points out Ralph Aldis, portfolio manager of the U.S. Global Investors World Precious Minerals Fund UNWPX, +0.97%

As for the dollar, gold is priced in greenbacks. So a higher dollar makes gold look more expensive to people investing from foreign currencies. That reduces demand, which hurts the price of gold.

It didn’t help that Chinese gold markets are closed due to the Golden Week holiday, taking some gold buying out of the market.

Or that mining-company investors have been burned by fading rallies in the past. That makes them quick to pull the trigger now.

“People were up a great deal this year in gold and gold miners, and for three years they saw every rally get killed,” says Dan Denbow, portfolio manager of the USAA Precious Metals and Minerals Fund USAGX, +0.28% So when these companies fell this week, they said: “ ‘We have to get out.’ And they moved to profit-taking.”

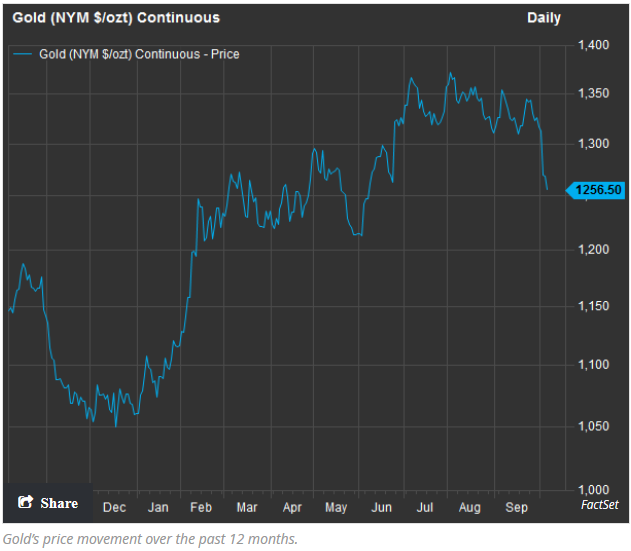

Once the selling got under way in earnest, gold broke through a perceived support level of $1,300 an ounce. That caused more selling as stop-loss orders kicked in, says Credit Suisse analyst Anita Soni. Gold traded Wednesday at around $1,260.

What’s next for gold?

Now, if economic data come in ho-hum, many of the forces hitting gold will reverse. Bond yields would fall and the dollar would weaken. That would boost gold and gold-mining stocks.

This is the near-term outlook of Michael Underhill, manager of the RidgeWorth Capital Innovations Global Resources and Infrastructure Fund INNNX, -0.38%

The next major economic data point will be U.S. September nonfarm payroll numbers on Friday. Underhill expects a “goldilocks” number, or not too hot and not too cold. Economists polled by MarketWatch expect 169,000 new jobs added, which would be an increase from 151,000 in August. “We will see more confirmation that the Fed is stuck between a rock and a hard place,” says Underhill. “I don’t think we are seeing significant GDP growth.”

Underhill says that as this realization sets in, gold could trade up toward $1,400 an ounce by the end of the year. If so, that should drive gold-mining stocks up significantly from here. Credit Suisse’s bond team is also skeptical about a December hike. It predicts no rate increases until May 2017.

Even if the Fed does hike in December, this could be good for gold after a few weeks of the inevitable market chaos that would ensue. After all, that was the scenario last year, points out Aldis, at U.S. Global Investors. “If the Fed does raise rates in December, it will be back to the races, because the market knows it won’t raise rates any time soon after that.”

Gold and miners did well earlier this year as economic data were weak and the Fed talked down expectations of rate increases. This helped weaken the dollar, which is good for gold.

Aldis expects sideways action in gold until December. “Getting the interest-rate hike out of the way is going to be the key thing in the short term.”

Denbow, at the USAA Precious Metals and Minerals Fund, expects a trading range of $1,250 to $1,350 between now and the Fed meeting in December. Gold will bounce around between now and then as economic data come in hot and cold. Since gold is now near the low end of that range, this suggests upside for gold stocks from here.

On a technical level, gold mining stocks look like they might have support. The Market Vectors Gold Miners is trading close to its 200-day moving average of around $23.30, says Mariann Montagne, senior investment analyst at Minnesota-based Gradient Investments.

Reasons to love gold

There are several good reasons to be bullish on gold for the long term.

- Chief among them: The U.S. will strive to create inflation by “debasing” the dollar, to ease its debt burden, says Tom Winmill, who manages the Midas Fund MIDSX, -0.81% He points out the U.S. has $20 trillion in debt, or upwards of $100 trillion if you include obligations like Social Security, Medicare, Medicaid and veterans benefits. “Whenever that comes home to roost that will require an inflationary response by the U.S. government to inflate away the debt,” says Winmill. Gold tends to benefit from inflation.

- Aldis thinks inflation may heat up on its own, especially now that we are near full employment, which puts upward pressure on wages.

- And then there is the potential Trump effect. If Donald Trump wins the election and sets up trade barriers such as import tariffs, that will put downward pressure on the dollar, says Winmill. That would support gold.

If you are unsure about what to do with gold and gold miners now, here is a good suggestion. Many investment advisers say you should always have a little bit of them your portfolio, say, 5%, as a hedge. “If you don’t have them in your portfolio, this gives give you an opportunity,” says Denbow.

Favored gold stocks

One thing is sure, if gold resumes its rally, gold miners — and the mutual funds that hold them mentioned in this column — are ready to enjoy another ride up. That’s because profit margins will widen, following years of cost cutting. “They’ve gotten costs under control,” says Denbow. “Gold miners have shown they have better operating margins.”

One of his favorite names is Newmont Mining Corp. NEM, -0.23% because it has done such a good job of cutting costs and reducing leverage. “They were one of the early ones to right size for a volatile gold market,” says Denbow.

A favorite of Winmill at the Midas Fund is Detour Gold Corp. DGC, -1.40% which has a big mine in Ontario. Investors are skeptical of Detour Gold because it has only one asset, which has low-grade deposits. Plus, the company has a lot of debt. But on the bright side, the property is big. “The really exciting thing is the deposit is so huge,” says Winmill. Detour has also been improving production. And it is paying down debt.

That makes it an attractive target for a big company like Newmont or Barrick Gold. Big mining companies are suffering from production declines, so they are on the hunt for acquisitions. In the past two years, for example, there have been 28 deals among companies covered by BMO Capital Markets, says Andrew Kaip, an analyst at the brokerage.

Winmill also likes West African mining company Randgold Resources Ltd. GOLD, +1.15% in part, because it is well-managed, so it produces a high return on equity. “Whether you are bullish on gold or uncertain, this is a company that will continue to deliver returns for investors,” he says. “Randgold is built to run at $1,000 gold. So everything above that is good for them,” agrees Denbow, who also likes this company.

Underhill, at RidgeWorth Capital, favors Barrick Gold, in part, because it continues to sell non-core assets to bring down leverage. Meanwhile, it’s bringing production projects online, which will spur growth, says Goldman Sachs analyst Andrew Quail, who has a “buy” rating on the stock

Finally, Aldis, at U.S. Global Investors, suggests Klondex Mines Ltd. KLDX, +0.83% even though it’s more than tripled over the past three years, to trade recently at around $5 a share. Klondex has mines with high-grade ore in Nevada, so there is minimal political risk. And it just added to its holdings with the purchase of more mining properties nearby. Aldis thinks Klondex would be profitable even if gold fell to $800 an ounce.

At the time of publication, Michael Brush had no positions in any stocks mentioned in this column. Brush suggested KLDX at $1.10 a share in 2013 in his stock newsletter, Brush Up on Stocks. Brush is a Manhattan-based financial writer who has covered business for the New York Times and The Economist group, and he attended Columbia Business School in the Knight-Bagehot program.

Article and media originally published by Michael Brush at marketwatch.com