Opinion: 13 Stocks These Winning Stockpickers Recommend Now

I rise, your Honor, in defense of stock picking. I admit I’m an unlikely public defender for the stockpicking industry, since I have made a career of pointing out how difficult it is to beat the market.

Just recently, in fact, I wrote a column pointing out that hardly any of the mutual funds and hedge funds that beat the market in one period are able to repeat their achievement in the subsequent one. But when a criticism goes too far, my contrarian instincts become aroused. And this past week has seen a number of claims about stockpicking that were unfair.

Take the Alternative Investments Conferencethat was held recently at the London School of Economics. Though I did not attend, media accounts reported that a number of hedge fund managers argued that the twin forces of artificial intelligence and Big Data were about to make it virtually impossible to locate stocks that would outperform the market.

One manager, for example, argued that because “computers can analyze the entire stock-picking universe instantaneously, the time of picking stocks based on inefficient flows of information is over, or will be over pretty soon.”

I’m not holding my breath. The graveyards of Wall Street are filled with those who confidently predicted that this or that strategy is “dead.” For one perspective on why the reported death of stockpicking is overblown, I checked in with Kent Daniel, a finance professor at Columbia University who has a rare combination of grounding in both academia as well as on Wall Street. Between 2004 and 2010, he was with the Quantitative Investment Strategies group at Goldman Sachs, becoming that group’s co-chief investment officer in 2009.

In an interview, Daniel argued that “we don’t have as much data as the hype would have us believe.” Consider, for example, trying to determine how wide a company’s moat is — how many barriers to entry it has erected to keep out potential competitors. What kinds of data, and how much, do you need to determine the answer? Says Daniel: “Those things are hard to quantify.”

Daniel allowed that data collection will undoubtedly improve in coming years. But for some of the tasks an analyst faces, no amount of data will ever be able to provide answers. This is especially the case for cutting-edge technologies, which by definition have never existed before. What data could you have looked at in advance of Facebook’s 2012 IPO to know that the company would be as successful as it has turned out to be, or in advance of Twitter’s 2013 IPO that would tell you that its stock would be a terrible investment?

Daniel has a strong sense of déjà vu when hearing about the triumph of artificial intelligence and the death of stockpicking. He pointed out that, in 2006, quantitative strategies were all the rage and its cheerleaders were claiming that it would rule the world. Then, after those strategies largely failed to anticipate the 2008-09 financial crisis, many were quick to declare that quantitative investing was dead.

A shrewd contrarian, of course, would have done just the opposite. And that’s why, contrary to those claiming stockpicking is dead, the next couple of years may in fact see its renaissance.

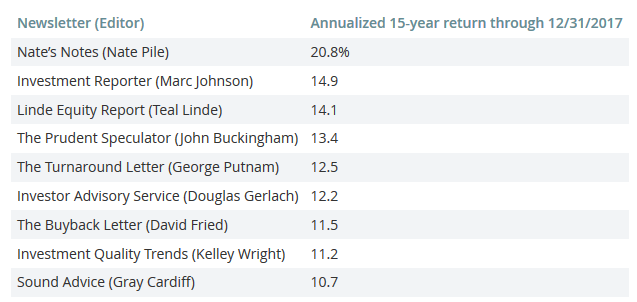

If you agree, a good place to start in your construction of a portfolio of stocks would be one or more of the top-performing investment newsletters my performance-auditing service monitors. Below are the nine stock-picking newsletters on that list whose 15-year annualized return (through Dec. 31) is ahead of the total stock market (as measured by the Wilshire 5000’s total return of 10.4% annualized):

To give you an idea of the kind of stocks these market-beaters are recommending currently, the most popular stock among them is Walt Disney Co. DIS which is recommended by five of these nine newsletters. The next most popular, recommended by four services, is IBM IBM.

Eleven more stocks are currently recommended by three of these nine services: Apple AAPL, CVS Health CVS, Cardinal Health CAH, Celgene CELG, Intel INTC, JPMorgan Chase JPM, Johnson & Johnson JNJ, Medtronic MDT, Pfizer PFE, Procter & Gamble PG, and Wells Fargo WFC.

Article and media originally published by Mark Hulbert at marketwatch.com