Start every trading day with a quick, actionable snapshot of global markets, key earnings, and the biggest movers across US, Europe, and Asia. Get the insight before your first coffee is gone.

July 1, 2026 | Issue 162

Fed Rate Hike 2026: What Breakeven Inflation Is Telling Us

Nikolay Stoykov

Managing Partner at Alaric Securities

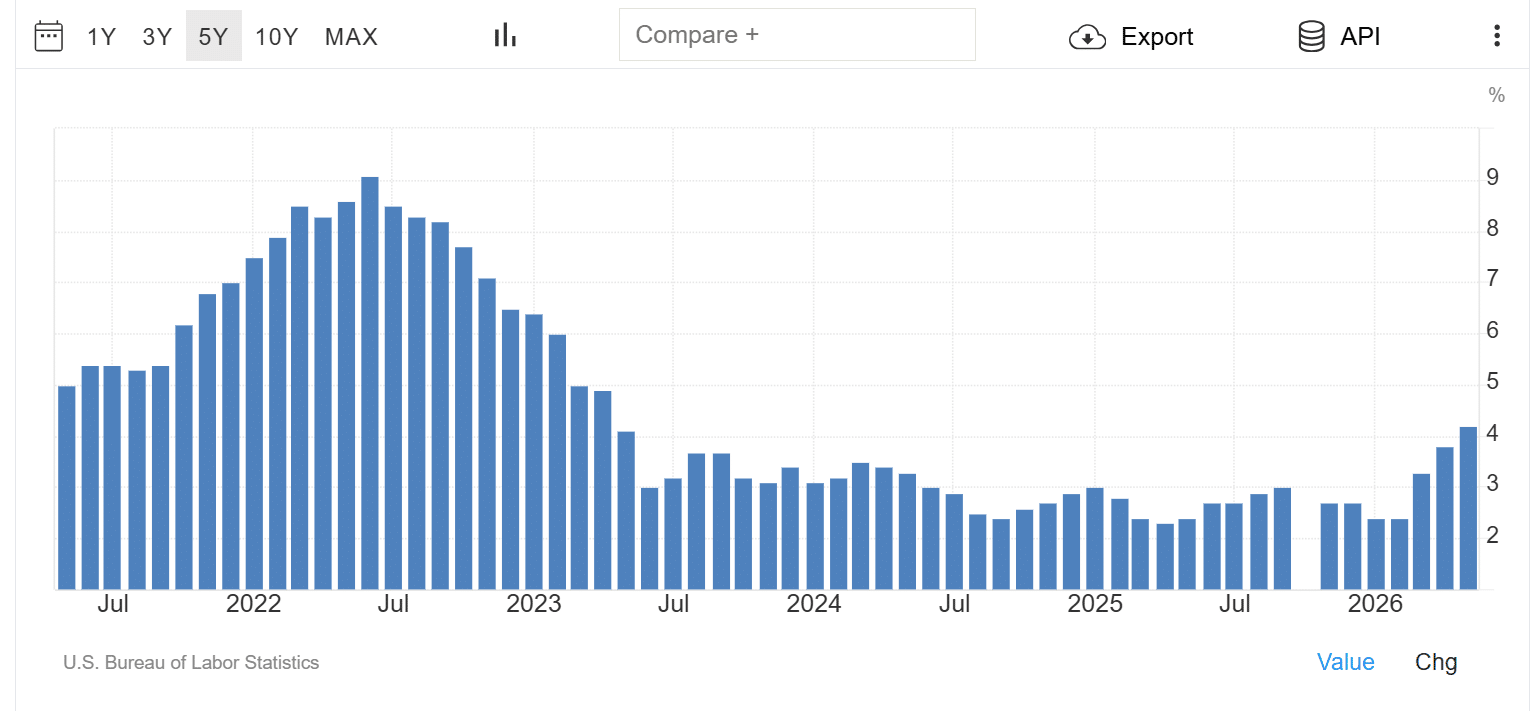

First, we will start with an obvious fact: following the onset of the Iran-US conflict, the US economy, along with most other world economies, experienced a surge in inflation. As a result, there came rising expectations of a Fed rate hike before the end of 2026. Courtesy of the US Bureau of Labor Statistics, please see the annual inflation chart for the last five years in the United States.

Current Inflation Data and Fed Rate Expectations

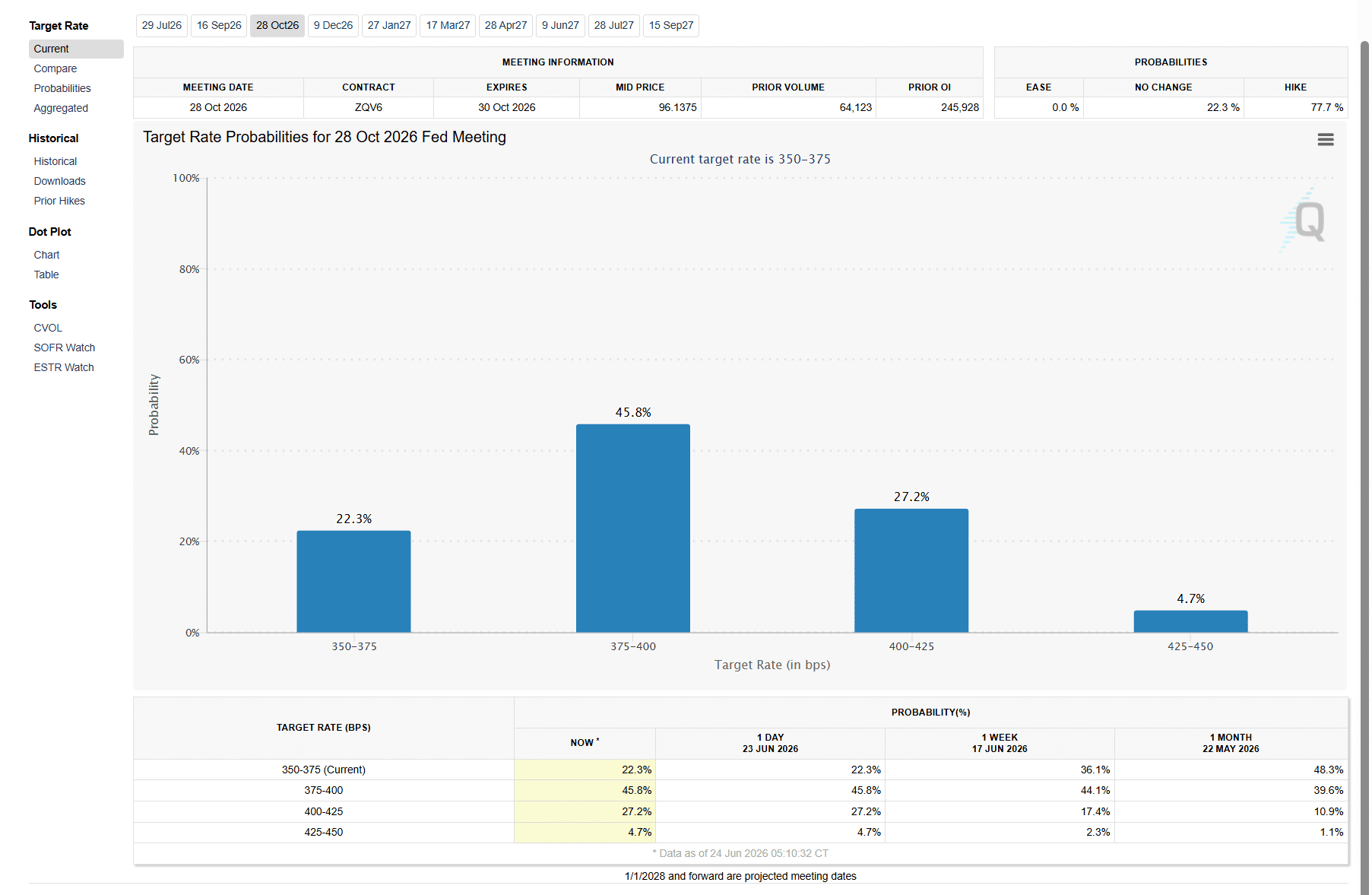

Given that short-term rates are between 3.50% and 3.75%, current inflation readings are above them. Usually, that calls for rate hikes. Some Central Banks have already done it – most notably the ECB. For example, the ECB raised rates from 2% to 2.25% amid annual inflation above 3% in the Euro Area. Given this information, market participants widely expect the Fed to raise rates in late summer/early fall 2026 — and market data confirms it. Courtesy of Fed Watch, please see the market expectation for the October 2026 levels of Fed Fund Rates:

Considering that the current Fed Funds Rate is 3.50%–3.75%, the market assigns only a 25% probability that rates will remain unchanged by October 2026. Most participants expect the Fed to raise rates by at least 0.25% by that date (approximately 50% probability). Meanwhile, a further 25% probability is assigned to a cumulative increase of 0.50%.

The logic behind these expectations is understandable. With annual inflation running above 4%, it would appear prudent for the Fed to keep short-term rates near that level. Under that framework, an additional 0.25%–0.50% increase seems reasonable. It is difficult to argue with that logic if the only data we consider are current inflation readings.

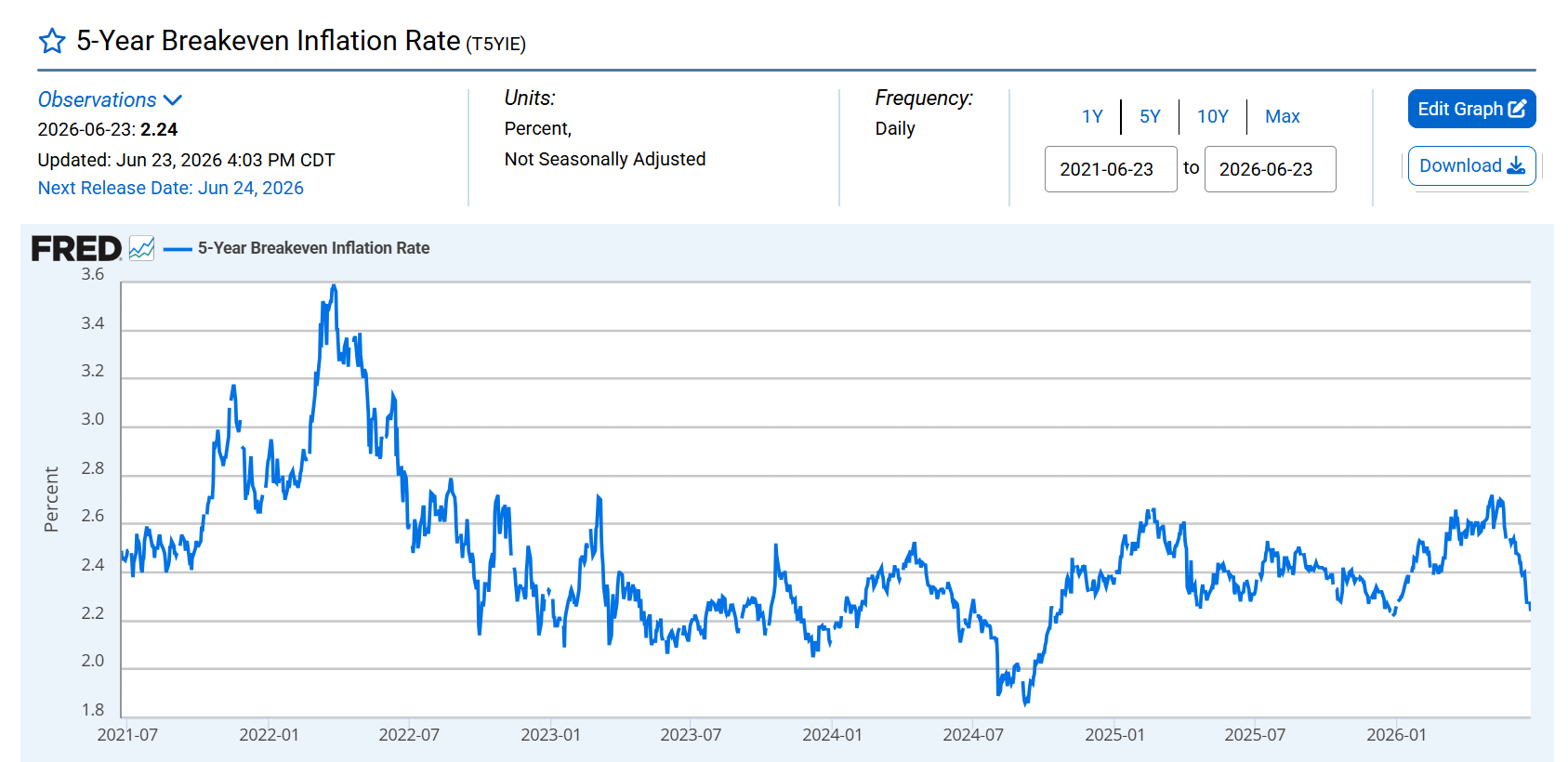

What the 5-Year Breakeven Inflation Rate Shows

However, markets exist not only to reflect current conditions but also to provide insight into future expectations. While market expectations can be volatile and are certainly not infallible, they remain among the most useful forward-looking indicators available. Additionally, market expectations for inflation over the next five years, as measured by the 5-Year Breakeven Inflation Rate, suggest a very different picture.

The chart below, courtesy of FRED, shows the five-year historical chart of the 5-Year Breakeven Inflation Rate — a widely used market-implied measure of expected inflation over the next five years.

Expected inflation is currently near the lower end of its 2026 range at approximately 2.24% per annum — well below the latest annual inflation reading of 4.2%. The divergence suggests that market participants expect inflationary pressures to moderate over the coming years. As a result, it is possible that the inflation surge experienced in 2026 may prove more transitory than current data alone would suggest.

Breakeven inflation rates are not perfect predictors of future inflation — liquidity conditions, risk premia, and investor positioning influence them. Nevertheless, they remain one of the most widely followed market-based measures of long-term inflation expectations.

Why the Gap Matters

Fortunately, market expectations for a Fed rate hike do not begin with the September 2026 Fed meeting. Current expectations are for the Fed to leave rates unchanged in July (approximately 65% probability). Then, the Fed might potentially raise rates by at least 0.25% in September.

Given that oil prices have largely returned to pre-conflict levels and shipping traffic through the Strait of Hormuz continues to normalize, we believe there is a reasonable chance that inflation readings may begin to moderate in the coming months. Moreover, even though the conflict appears to have eased, the impact of higher gasoline prices on consumers may persist longer than the initial inflationary impulse. Under such circumstances, additional rate increases could prove unnecessarily restrictive.

Our Outlook

In conclusion, while current inflation data appear to justify higher short-term rates in the United States, market-based inflation expectations suggest that the situation may not be so straightforward. With tensions in the Middle East easing and oil prices returning toward normal levels, there may be sufficient time for inflationary pressures to moderate without additional policy tightening.

While it is certainly possible that the Fed raises rates by 0.25% or even 0.50% in 2026, as currently expected by the market, we believe such action may ultimately prove unnecessary. At the very least, we believe additional rate hikes are far from inevitable.

Disclaimer

The articles, podcasts, and newsletters from Alaric Securities OOD are classified as marketing communications. The views expressed are solely those of the individual authors affiliated with Alaric Securities OOD and do not necessarily reflect the views of the company, its subsidiaries, or affiliates. This content is provided for informational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security, digital asset (such as cryptocurrency), or other financial instrument. Third-party content is included solely for informational purposes and does not reflect the views of Alaric Securities OOD. All investments involve risk, including the possible loss of principal. Past performance is not indicative of future results. References to third-party companies, logos, or trademarks are used under fair use/fair dealing principles for analysis and commentary.

Stay Ahead with Alaric Securities Newsletters

Traders and investors don't need more information - they need better information. That’s what we deliver!

Step back from the daily noise. Each issue explores market trends, industry shifts, trading opportunities, and exclusive updates — learn what's shaping the markets, not just what's trending online. Ready to get the edge?