Trading ETFs On Leverage vs Trading Leveraged ETFs

Leveraged ETFs and the Myths Around Leverage Investing

Many investors misunderstand how leverage works in practice — and leveraged ETFs in particular are often misread. Below, we break down three of the most common misconceptions.

Myth 1: Investors Do Not Use Leverage

A widely accepted belief is that investors do not use leverage. In reality, many investors have used leverage successfully throughout financial history. The difference is that the leverage they use is often moderate. It is obtained through instruments with embedded leverage, such as options, warrants, or structured securities.

One of Warren Buffett’s most successful leveraged investments was his stake in Goldman Sachs during the financial crisis. The investment included both preferred shares and warrants (long-dated call options issued by Goldman Sachs). While Buffett has often warned against excessive leverage, this example demonstrates that leverage itself is not necessarily problematic.

This is true when used appropriately and within a well-defined risk framework.

Myth 2: Using Leverage Always Brings the Possibility of a Margin Call

Theoretically, any leveraged position can generate a margin call. In practice, however, the outcome depends on both the amount of leverage used and the structure of the instrument.

Consider an investor who purchases S&P 500 futures using 50% leverage. In other words, the investor has $100 of capital and obtains $150 of market exposure. If that investor had entered the market at the 2007 peak, the subsequent decline during the Global Financial Crisis would have been painful. Nevertheless, such a position would have remained well within historical exchange margin requirements.

Historically, exchange margin requirements on S&P 500 futures have generally been around 20% of contract value. These requirements have survived severe market events, including the 1987 crash and the 2008 financial crisis. While future market conditions may differ from the past, moderate leverage on broad equity index futures has historically proven remarkably resilient. This holds even during periods of extreme volatility.

This does not eliminate risk, but it suggests that the structure and magnitude of leverage may matter more than the mere presence of leverage.

Myth 3: Trading On Leverage and Trading Leveraged ETFs Yield Similar Results

This is perhaps the most important misconception.

Trading on leverage allows investors to:

A) Choose their desired level of leverage.

B) Control that leverage themselves.

Leveraged ETFs operate differently. Their leverage is typically reset daily. Portfolio adjustments are made by the fund manager in accordance with the fund’s methodology, rather than by the investor.

As a result, long-term performance can differ significantly from what many investors intuitively expect.

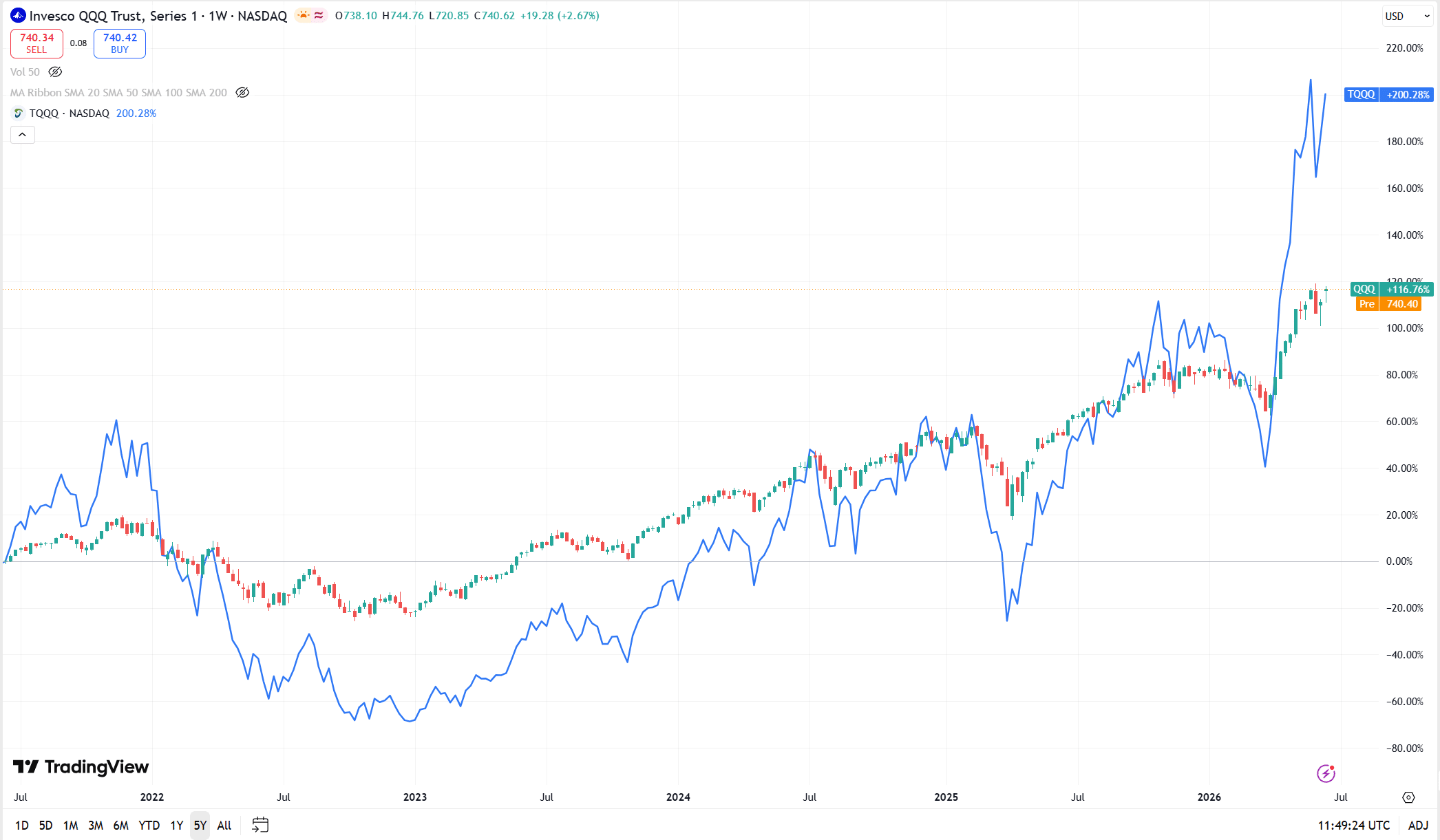

Example that matters – QQQ vs TQQQ

Our favorite example is the comparison between the Nasdaq-100 ETF (QQQ) and the triple-leveraged Nasdaq-100 ETF (TQQQ) over the last five years.

QQQ generated approximately 116% cumulative returns during that period, while TQQQ generated approximately 200%.

At first glance, some investors might expect a triple-leveraged ETF to produce roughly three times the cumulative return of the underlying index. In practice, because leverage is reset daily, realized returns can differ substantially from that expectation.

Over longer periods, TQQQ has often behaved more like a highly leveraged version of QQQ rather than a simple “three times QQQ” investment. Moreover, the difference between expected and realized outcomes is driven primarily by volatility, path dependency, and the mechanics of daily leverage resets.

An investor using moderate leverage directly on QQQ could, in certain market environments, achieve comparable or even superior returns while experiencing lower volatility than a triple-leveraged ETF.

This is one reason why many professional investors prefer to obtain leverage through margin, futures, or options rather than through leveraged ETFs.

There have also been periods during which the underlying index generated modest gains. During the same periods, the leveraged ETF significantly underperformed what many investors expected based on the leverage multiple alone.

The Structure of Leverage Matters More Than the Label

Reasonable use of leverage on highly liquid products such as the S&P 500 and Nasdaq-100 has survived numerous market cycles and stress events. Many investors and traders have used leverage successfully, and continue to do so today.

Leveraged ETFs, on the other hand, represent a specialized tool rather than a universal solution. Their daily leverage resets, management costs, and portfolio turnover can create outcomes that differ meaningfully from investor expectations, particularly over longer holding periods.

For that reason, leveraged ETFs may be most appropriate for a relatively narrow group of market participants with a clear understanding of their mechanics and intended use. For many long-term investors, obtaining moderate leverage directly may prove to be the more transparent and efficient approach.