The 10-Year Treasury Yield Outlook After Fed Cuts

It’s becoming clear that the 10-year Treasury yield outlook is shifting as the U.S. Federal Reserve enters the second leg of its long-delayed rate-cut cycle.

That raises an obvious question: what comes next for long-term yields, especially the benchmark 10-year Treasury?

The answer matters not only for bond investors but for the global capital-allocation landscape. Long-term U.S. yields influence equity valuations, mortgage affordability, and corporate financing costs worldwide – in short, they define the financial gravity of the system.

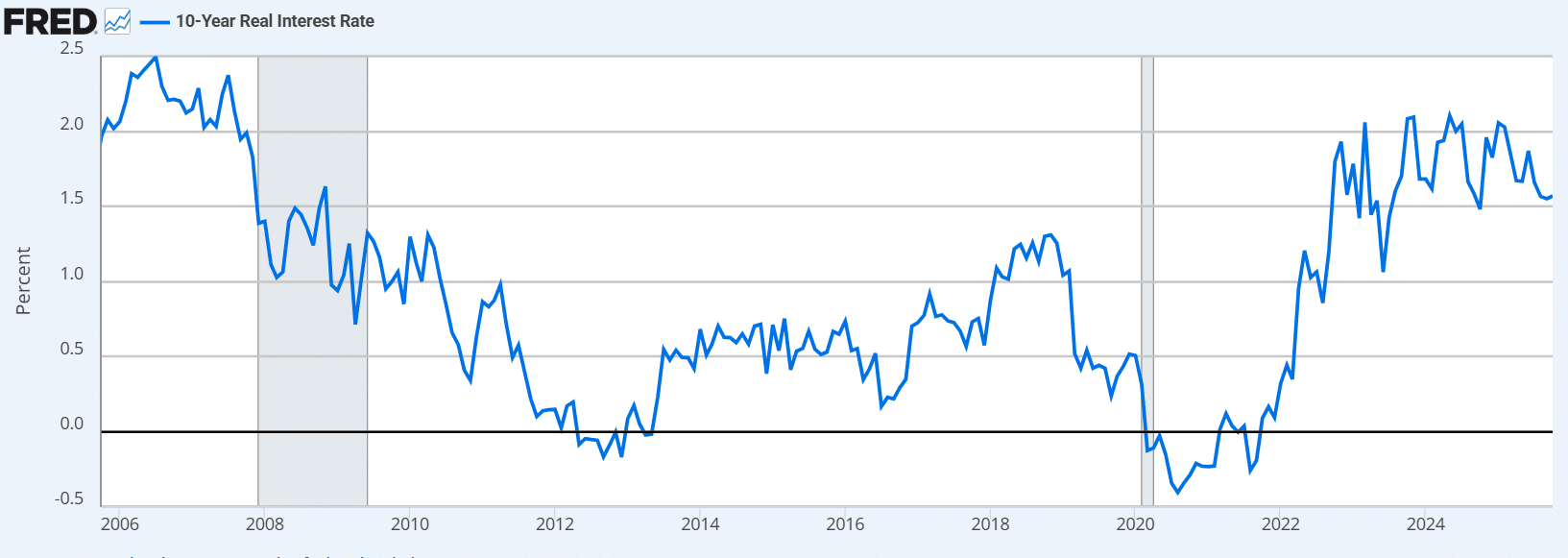

What Are 10-Year Real Interest Rates?

Source: Federal Reserve Economic Data (FRED)

The 10-year real interest rate, derived from Treasury Inflation-Protected Securities (TIPS), represents the return investors expect above inflation.

TIPS adjust their principal with inflation while their coupon rate remains fixed, isolating the real return.

This makes real yields a reliable measure of monetary stance, inflation credibility, and long-term investor confidence – not only in the U.S. but also for global markets that track U.S. Treasury benchmarks.

Observation #1 — Still Near the Top of Its Range

Over the past 20 years, real 10-year yields have fluctuated between –0.5% and 2.5%; over the last decade, between –0.5% and 2.0%.

Even after the Fed’s initial rate cuts, the real-rate premium remains elevated at around 1.56%, near the top of its 10-year range.

This reflects lingering uncertainty about inflation’s persistence and the market’s cautious optimism regarding a soft landing in the U.S. economy.

Observation #2 – The Long-Term Mean Is Lower

The 20-year average real yield is about 0.97%.

Even as monetary policy eases, inflation anxiety keeps long-term real yields unusually high.

If the Fed’s confidence proves justified and inflation stabilizes near target, the premium could compress toward its historical mean.

That would ease financial conditions — welcome relief for U.S. consumers, mortgage borrowers, and leveraged companies, while also supporting global capital flows into risk assets.

From Real to Nominal – Estimating Fair Value

To estimate a fair nominal yield, add expected inflation to the real rate.

-

Current 10-year inflation expectations (“breakeven rate”): ≈ 2.28%

-

Long-term average real yield: ≈ 0.97%

-

Fair value = 3.25% nominal yield

That level represents a normalized environment — inflation near target, steady growth, and a market that once again prices time, not fear.

Where We Stand Today

The actual 10-year Treasury yield hovers around 4.13%, nearly 90 basis points above fair value.

This divergence reflects two simultaneous dynamics: equity exuberance and bond caution.

At current levels, 10-year Treasuries may deliver equity-like returns, potentially 10%+ per year with far less volatility.

Such opportunities are rare. When fundamentals and sentiment diverge this widely, patient capital usually wins.