Start every trading day with a quick, actionable snapshot of global markets, key earnings, and the biggest movers across US, Europe, and Asia. Get the insight before your first coffee is gone.

March 20, 2024 | Issue 56

Inflation-Linked Bonds: Insights into Market Sentiment

Nikolay Stoykov

Managing Partner at Alaric Securities

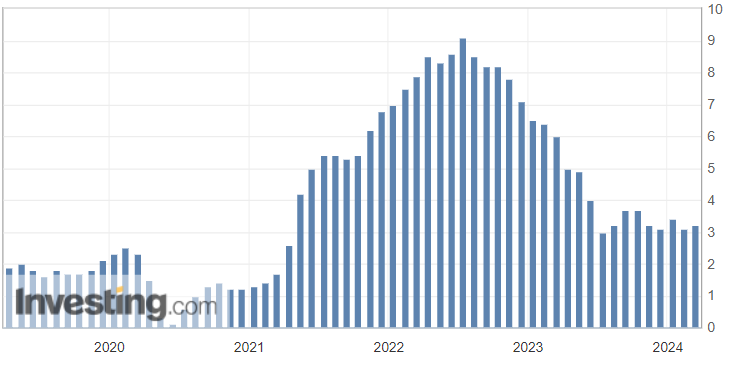

Inflation-linked bonds have become a focal point amidst the recent uptick in the US Consumer Price Index (CPI), which recorded a 0.40% increase in February 2024.

Year-over-year, the Index showed a 3.20% change, slightly surpassing the January 2024 figure of 3.10%:

US Consumer Price Index YoY

That begs the question: Is inflation bottoming? Could we see 3%, 4%, or even higher inflation in 2024?

Let’s see what the markets are saying. Fortunately, a market provides such an estimate called Treasury Inflation Protected Securities (TIPS).

The Role of TIPS in Combatting Inflation

Treasury Inflation Protected Securities (TIPS) are government-issued bonds tailored to combat inflation’s adverse impact on investors. Unlike traditional bonds, the principal value of TIPS adjusts in response to changes in the Consumer Price Index (CPI), ensuring that investors’ returns keep pace with inflation. Additionally, TIPS offers a fixed interest rate, typically above inflation, providing a reliable income stream that preserves purchasing power. As such, TIPS serves as a cornerstone in portfolios seeking to mitigate inflation risk and maintain real returns over time.

In brief, TIPS are bonds quoted in actual yield; the notional amounts are adjusted to changes in the US CPI, and bondholders are compensated at a fixed interest rate above inflation.

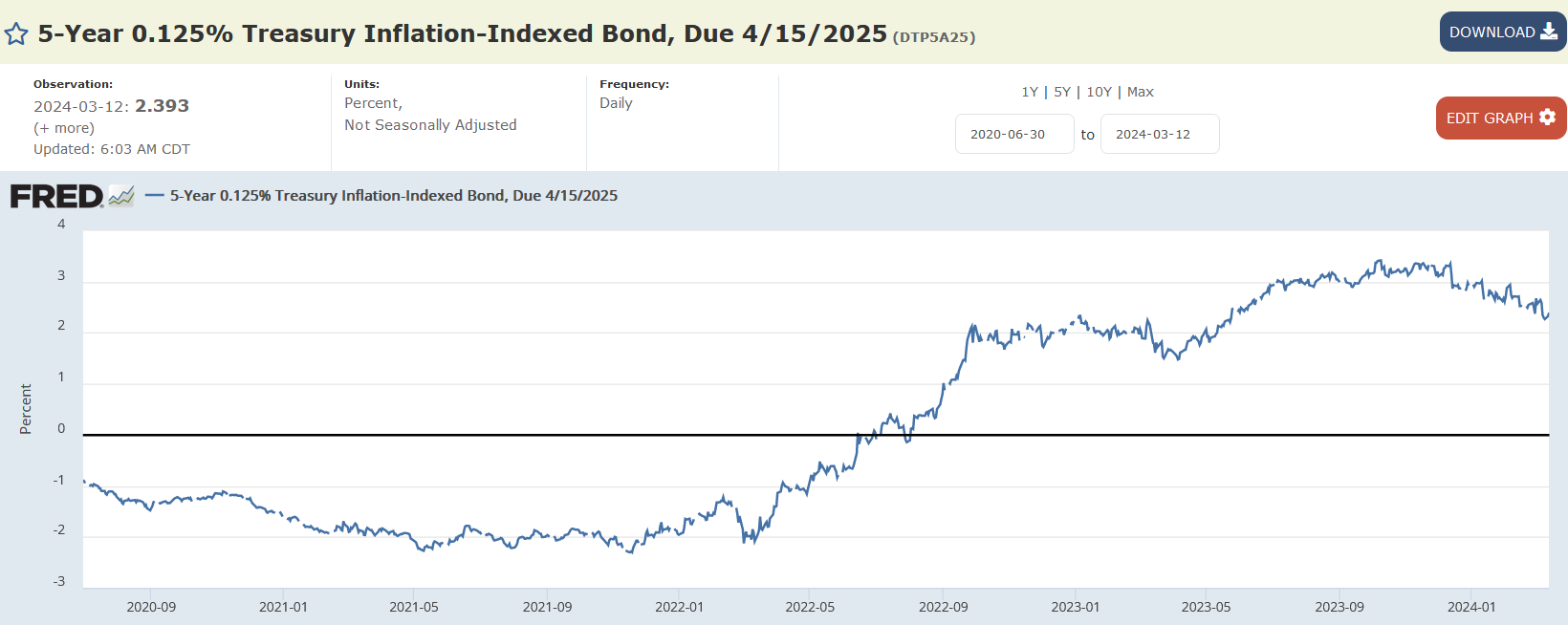

Let’s look at one such security – Treasure Inflation-Indexed Bond 0,125% 4/2025:

Source: Federal Reserve Economic Data, FRED

Currently, that bond yields 2,393% on an annual basis. So, how do we extrapolate what inflation for the period is expected to be? Very simply – we compare it to 1-year Treasury yields.

If one-year plain vanilla Treasury Bonds are yielding 5.02% and Treasury Inflation-Indexed Bonds are yielding 2,393%, then the markets are implying that:

Expected Inflation = (1+Nominal Rate)/(1+Real Rate) – 1 = 1,050243/1,02393-1 = 2,57%

Note: Sometimes, this is approximated as the difference between the two rates: 5,0243%-2,393 = 2,63%. As our readers can see, the difference is usually minimal.

Yes, markets imply that inflation for the next 12 months will be 2,57%.

Let’s do similar calculations for the inflation in 2025. The Treasury Inflation-Indexed Note due 15/1/2026 is yielding 2,15%. US treasuries with similar maturity are yielding 4,62%. Therefore, the expected annualized inflation for nearly two years is 2,41% per annum. By extrapolation, we can deduce that the expected inflation for the second year period – April 2025 to January 2026—is approximately 2,20% on an annual basis. This is very close to the 2% yearly inflation level the Fed is looking for!

What About the Euro Area

Unfortunately, there are not as many inflation-linked bonds in the Euro Area. Also, the inflation-linked bonds there reference the Harmonized Index of Consumer Prices (HICP) for the Euro Area. That index is close to CPI in the Euro Area but not the same as CPI.

Anyway, we found one for 12 months out—France 0,118% 3/2025. The bond yields 1,05% per annum. The French one-year rate is 3,52%, which implies an increase in HICP of 2,44% for the next 12 months.

We were able to find a 2-year comparison as well – Germany 0,121% 4/2026. It is yielding 1.01% per annum. Given that the yield on a similar maturity German obligation is 2.85%, the annualized change in Euro Area HICP for the next two years is expected to be 1,82% annually. Knowing that expectations for the first year are at 2,44%, it implies HICP is expected to increase by 1,20% in 2025. This indicates that inflation will also likely be contained in the Euro Area!

Again, while CPI and HICP are not the same indexes, they track each other very well, and over the long run, the difference between the two is very small.

Key Takeaways

Generally, market-derived, tradable estimates are similar to betting odds for heavily betted sports games. Any individual estimate can be wrong, but over the long run, the betting public loses while the betting houses win. In our opinion, the above estimates are the best estimates for inflation over the next 12-24 months.

Therefore, it would appear that inflation has not bottomed yet—the uptick we saw in February is expected to be just a blimp, and the downtrend of benign monthly inflationary readings is expected to continue. Those readings are expected to be more benign in the Euro Area, where inflation is expected to drop to 1.20% in 2025. US inflation is expected to subside to 2.20% in 2025, roughly in line with the level of 2% that the Fed wants to see.

What This Means For You

Interest rates in EUR and USD are at a 20-year high. The current levels are above the expected inflation for the next two years in both the US and the Euro Area.

We expect investments in government bonds at current prices with one—or two-year maturities in those two regions to give bondholders returns above inflation.

Disclaimer

The articles, podcasts, and newsletters from Alaric Securities OOD solely represent the authors’ views affiliated with the company. They do not mean the perspectives of Alaric Securities OOD or any of its subsidiaries or affiliates. They are provided for informative purposes and do not constitute recommendations for or against purchasing or selling security. Digital assets (such as cryptocurrency) or other assets in any account. They are neither research reports nor meant to be the foundation for any investing decisions. Any third-party information given does not represent the views of Alaric Securities OOD or any of its subsidiaries or affiliates. All investments carry risk, including the potential loss of principal, and past success does not assure future success.

Stay Ahead with Alaric Securities Newsletters

Traders and investors don't need more information - they need better information. That’s what we deliver!

Step back from the daily noise. Each issue explores market trends, industry shifts, trading opportunities, and exclusive updates — learn what's shaping the markets, not just what's trending online. Ready to get the edge?