Stock Market Outlook 2026

The S&P 500 is up a little over 16% year-to-date, excluding dividends, and is trading near all-time highs. Most Wall Street analysts expect an additional 10%–14% appreciation in 2026. Under normal circumstances, this would be enough for us to endorse a constructive, even bullish, outlook.

However, 2026 is different.

We believe this is a year where an exception should be made.

The critical reason is the 2025 U.S. Government Shutdown, the longest on record. As a result, the shutdown delayed the release of several essential macroeconomic indicators, leaving investors without updated unemployment or inflation data since September. This prolonged data blackout has significantly reduced economic visibility and investor confidence, a risk we examined in detail in our analysis of the post-shutdown U.S. economic outlook.

The prevailing view on Wall Street is that the shutdown “should not matter,” pointing to the 2019 shutdown as an example where both the economy and markets performed well. Unfortunately, this comparison overlooks a crucial distinction.

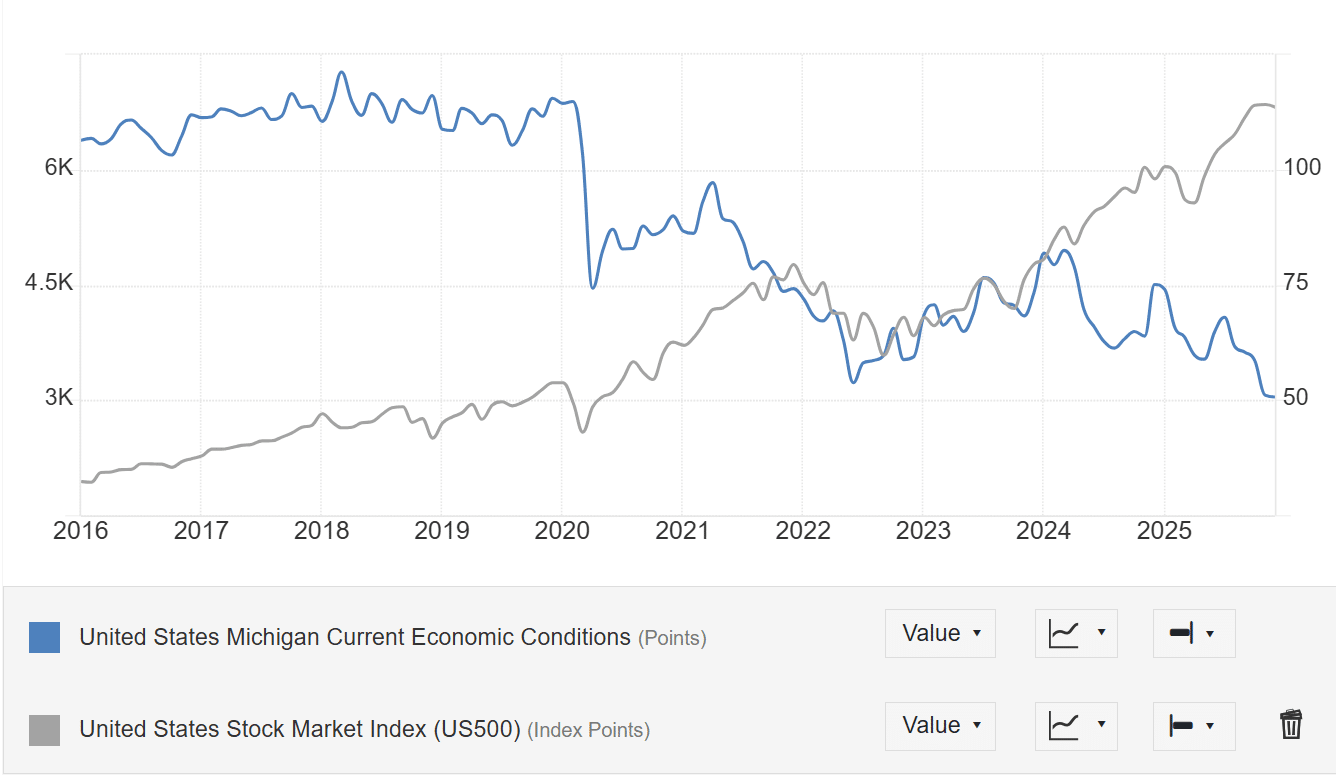

U.S. Consumer Confidence

Consumer confidence tells a very different story.

Unlike 2019, where the shutdown barely moved sentiment, the 2025 shutdown caused a sharp deterioration in the University of Michigan’s Current Economic Conditions index:

- September 2025: 60.4

- December 2025: 50.7

- New 10-year low

This matters for three reasons:

- It is a concurrent indicator — it moves with actual economic activity, not ahead or behind.

- It is not subject to revision — this makes it more reliable than GDP estimates or monthly labor data.

- The U.S. economy is 70% consumption — when consumers lose confidence, the economy feels it immediately.

In short: The most timely and reliable gauge of U.S. economic health is flashing its weakest signal in a decade.

What We Know — and What We Don’t

We do know:

- Consumer conditions have deteriorated sharply.

- The indicator is real-time and reliable.

- No unemployment, inflation, or GDP data has been available for months.

We do not know:

- How much the labor market has weakened.

- Whether inflation remains stable.

- How GDP has evolved during the shutdown.

Given this data vacuum, it is inappropriate to anchor on the usual bullish forecasts.

We do not present an ironclad bearish case. Rather:

The level of uncertainty is far higher than consensus assumes.

And in periods of uncertainty, the S&P 500 is generally vulnerable to downside—particularly in early 2026.

Therefore, we cannot endorse Wall Street’s expectation of +10% to +14% for the S&P 500 in 2026. A more cautious, risk-aware stance is appropriate.

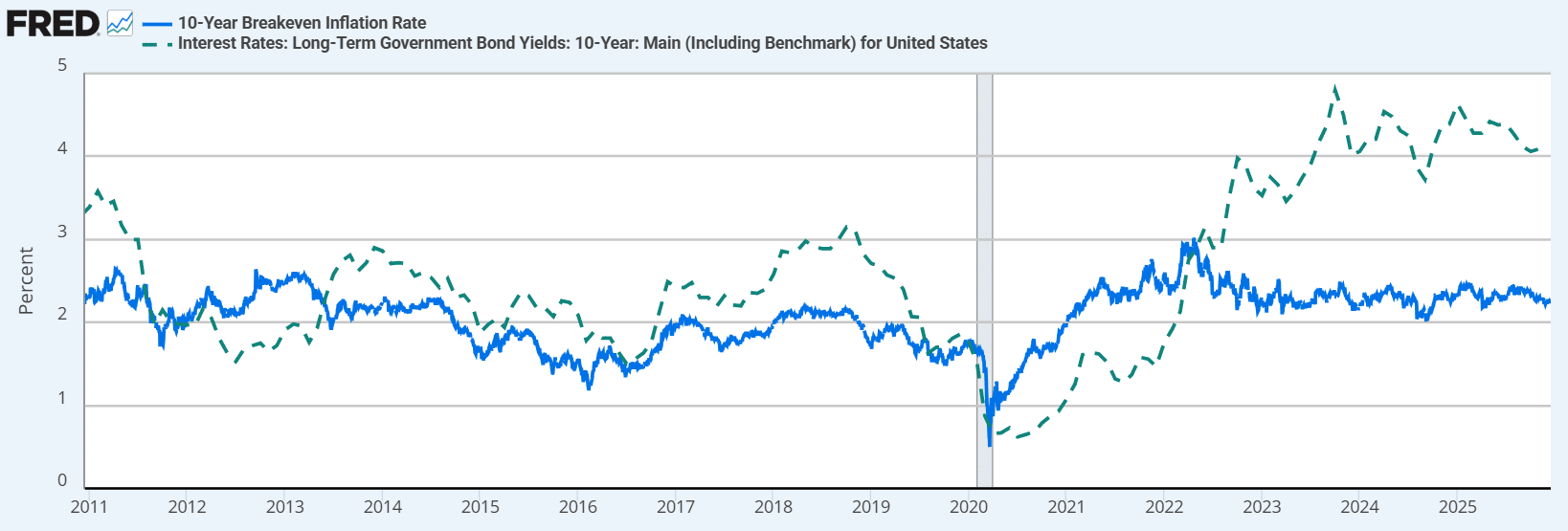

US Treasuries

Turning to interest rates, consider inflation expectations relative to current 10-year yields:

Inflation expectations have largely stabilized in 2025. The market-implied 10-year breakeven rate is 2.25%, which represents the tradeable, neutral inflation outlook.

While this is slightly above the Federal Reserve’s 2% target, the key point is not inflation. It is the spread between inflation expectations and long-term nominal yields:

- 10-year Treasury yield:18%

- 10-year inflation breakeven:25%

- Real-yield spread:93%

Historically—before 2020—this spread has been between –0.2% and +1.0%.

Today’s nearly 2% spread is unusually high and, in our view, unsustainable.

The change in leadership at the Federal Reserve in 2026 increases the probability of more dovish policy, especially if consumer-driven data continues to soften. Under such conditions, long-term rates could fall meaningfully.

Our estimate of fair value for the 10-year Treasury yield is:

Breakeven inflation + 1% = ~3.25%

This implies:

- Current yield: 18%

- Fair value: ~3.25%

- Potential appreciation: 10%–15% in long-duration Treasuries

In other words:

U.S. long-term Treasuries offer equity-like returns in 2026, with considerably lower economic risk.