JD Stock Forecast: Analysts See Upside Into 2026

We’ve recently discussed two of the most followed Chinese stocks – PDD Holdings (PDD) and Alibaba Group Holding (BABA). Back in December 2024, when PDD stock was trading around $107, we suggested it could climb toward $150.

It didn’t quite reach that level, but at $127 today, we’d still call that a win. In July 2025, we looked at Alibaba at $115 and expected a move to $150. With BABA now at $158, that one worked out well too.

Now, with this track record in mind, it feels like the right time to turn to JD stock forecast and why JD.com (NASDAQ: JD, HKEX: 9618) may be the overlooked Chinese e-commerce giant with room to rebound in 2026.

A Look at the Business Behind the Stock

Founded in 1998 by Richard Liu, JD.com began as a small electronics retailer in Beijing. After pivoting online in 2004, it grew into one of China’s largest e-commerce platforms. Today, JD operates a direct sales model that distinguishes it from Alibaba’s marketplace approach. Instead of only connecting buyers and sellers, JD buys inventory directly from suppliers and sells to customers giving it tighter quality control and stronger customer trust.

The company has also built one of China’s most advanced logistics networks, capable of same-day or next-day delivery across much of the country. Its JD Logistics arm now provides services to third parties as well. Alongside retail, JD has invested in cloud computing, AI, and autonomous delivery, strengthening its long-term positioning.

JD.com Financial Highlights (as of 2025)

-

Market Cap: ~$55 billion (combined US + HK listings)

-

Revenue (TTM): ~RMB 1 trillion (≈ US$140 billion)

-

Gross Margin: ~8% (lower than Alibaba, reflecting its direct-sales model)

-

Active Customers: ~580 million

-

Forward P/E (2026): < 9x

-

YoY Earnings Growth Forecast (2026): +40%

Source: company filings, analyst consensus (Seeking Alpha, Finviz).

These numbers underline the scale: JD is not a niche e-commerce player but a top-tier Chinese retailer, with revenue on par with some of the largest global names in retail.

JD vs. Alibaba and PDD: Different Strengths, Different Valuations

To understand JD’s investment case, it helps to compare it with peers.

-

Alibaba (BABA) operates primarily as a marketplace platform, collecting fees from merchants. This asset-light model is highly profitable but has left Alibaba exposed to regulatory crackdowns on monopolistic practices.

-

PDD Holdings (PDD), parent of Pinduoduo and Temu, has captured attention with its social commerce and aggressive discounting, appealing to value-driven consumers. PDD has been the market darling over the past two years, reflected in its premium valuation.

-

JD.com (JD, 9618.HK) takes a hybrid approach, running direct sales with full control over logistics, while also operating a third-party marketplace. This makes it capital-intensive, but it also builds stronger consumer trust in product quality and delivery reliability.

Despite being a direct competitor to both, JD trades at far lower valuation multiples. While BABA and PDD often dominate headlines, JD’s more conservative model may prove more resilient and the discount may not last if earnings rebound in 2026 as analysts expect.

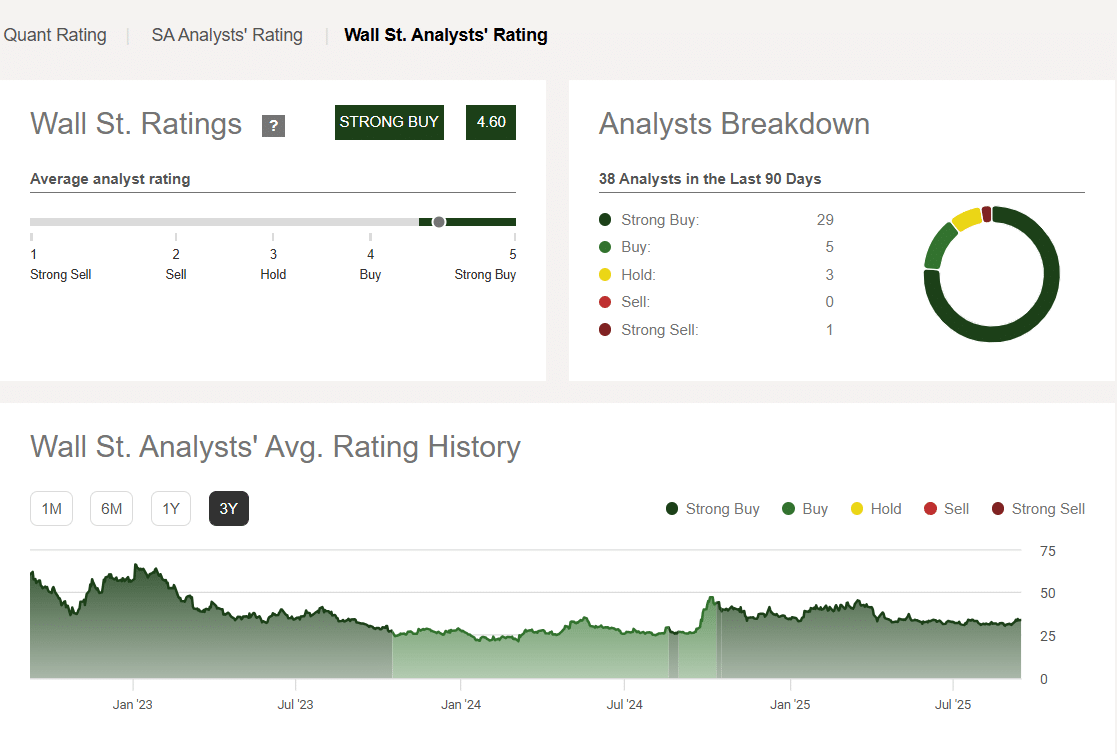

Analysts Remain Bullish on JD

Seeking Alpha data shows JD is among the most highly rated U.S.-listed companies. Analyst ratings follow a 1–5 scale (Strong Sell = 1, Strong Buy = 5), and JD currently scores 4.6. That puts it in rare company – fewer than 10 U.S. stocks hold higher ratings.

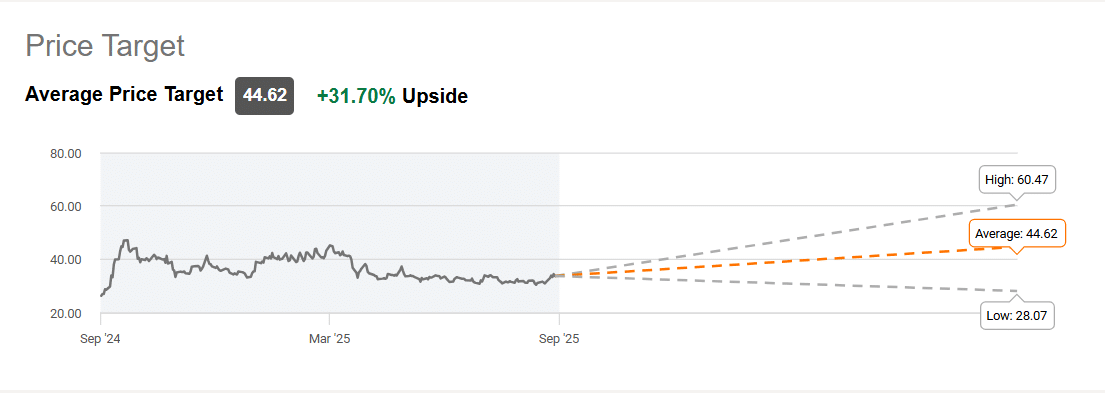

Even with such strong backing, JD trades at a 32% discount to the average analyst price target. For investors focused on JD stock forecast 2025–2026, that disconnect between sentiment and valuation is exactly what makes JD worth another look.

Valuation Points to Opportunity

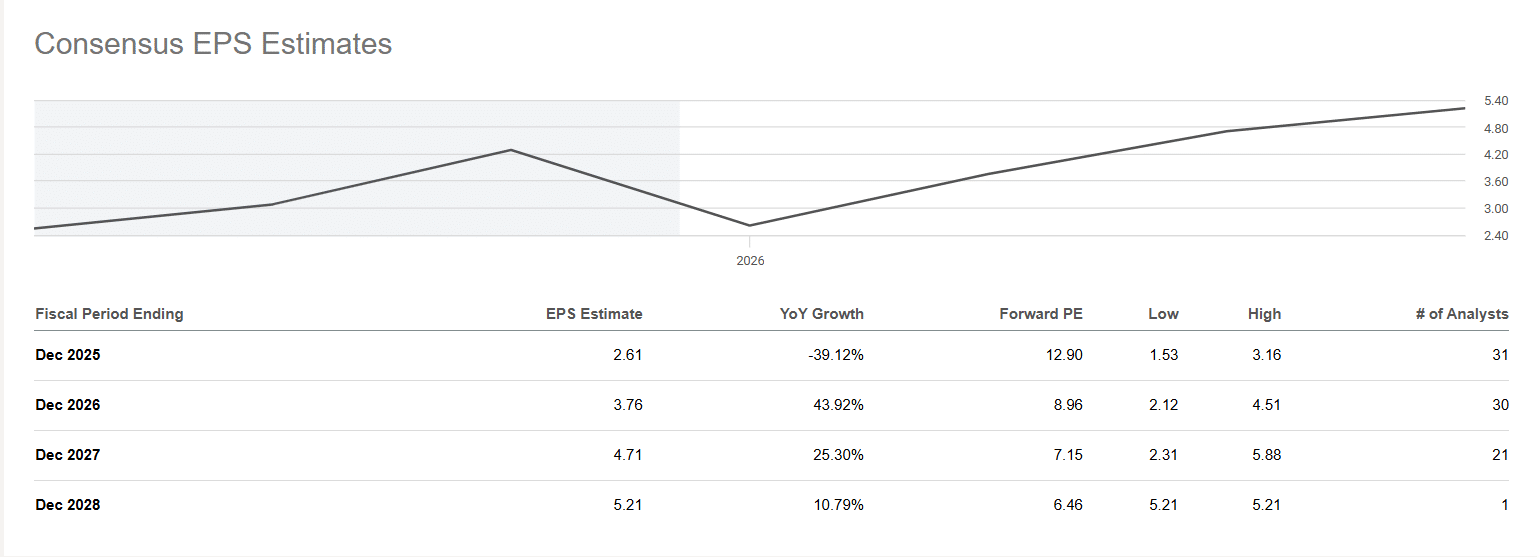

Valuation data makes the case even stronger. JD trades at less than 9x projected 2026 earnings.

True, 2025 has been a disappointing year. But analysts are forecasting more than 40% earnings growth in 2026, which could reset investor sentiment. With Chinese equities overall showing renewed strength, it may be investor skepticism, not analyst optimism, that is misplaced.

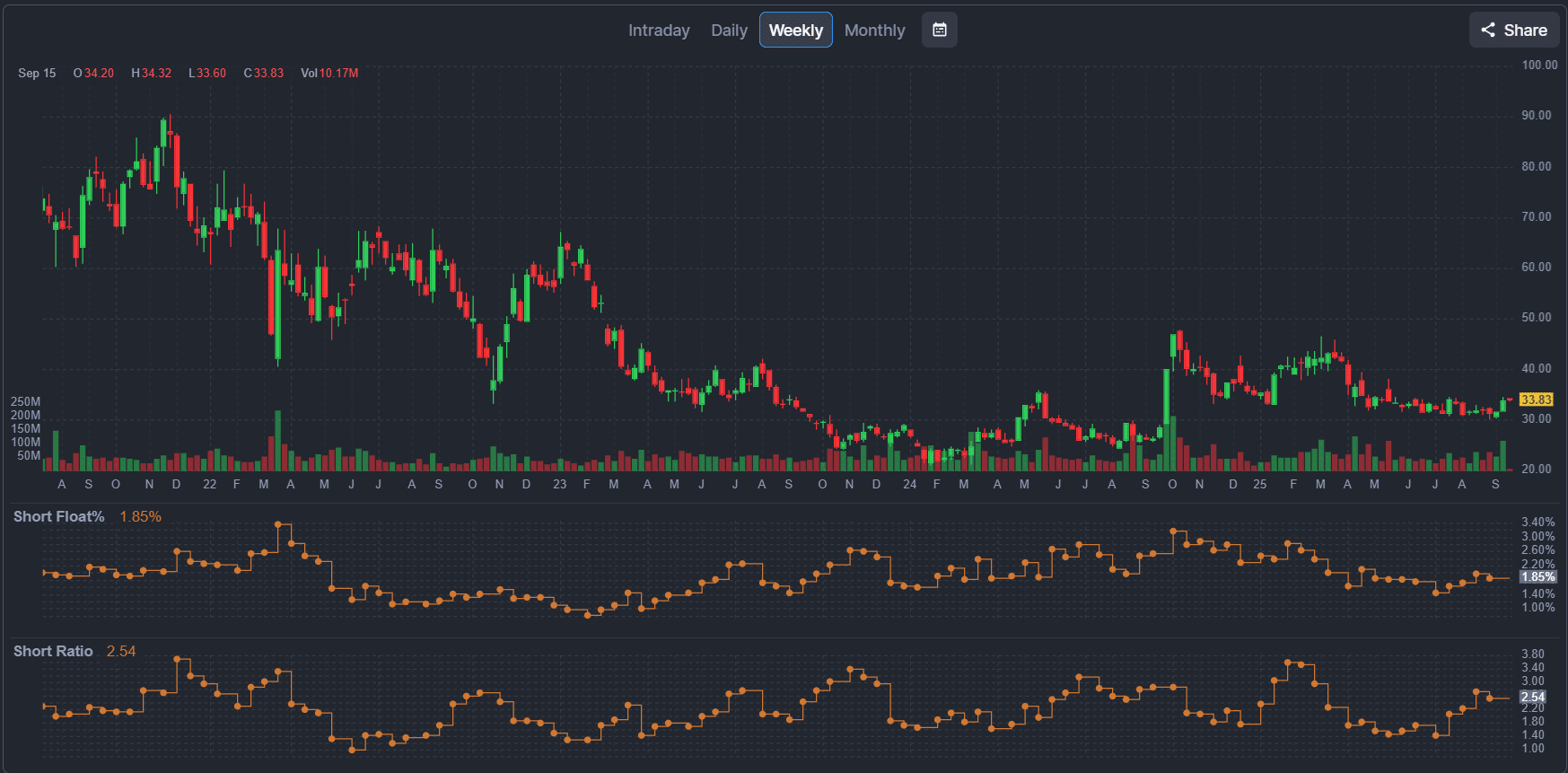

Market Sentiment – Calm, Not Bearish

Another encouraging sign – JD’s short float remains low, according to Finviz. That means there isn’t much conviction among traders that the stock is overvalued. When bearish bets are subdued, it often signals a valuation floor rather than further downside risk.

Bottom Line

JD may not command the same headlines as PDD or Alibaba, but it remains a true heavyweight in Chinese e-commerce. 2025 has been forgettable, but with earnings projected to climb over 40% in 2026, a forward P/E below 9x, and analysts firmly supportive, the outlook is far brighter than sentiment suggests.

For investors considering the JD stock forecast into 2026, the picture is clear – whether through its U.S. ticker (JD) or Hong Kong listing (9618.HK), JD.com looks undervalued, underappreciated, and potentially ready for a rebound.

JD stock is still the forgotten Chinese gem but perhaps not for long.