Inflation Expectations vs Breakeven Rates

It seems that, one way or another, the Chairmanship of Mr. Jerome Powell of the Federal Reserve will come to an end, either through his scheduled retirement within a year or sooner, if Mr. Trump has his way. In our view, Mr. Trump is right to be dissatisfied with Powell’s performance.

Over the last year, the European Central Bank (ECB) cut rates eight times, lowering short-term rates from 4% to 2%. In contrast, the Federal Reserve only reduced rates three times, from 5.5% to 4.5%.

Yes, U.S. inflation has been slightly higher than in the Euro Area – 2.7% versus 2%, but not enough to justify such a stark difference in interest rate policy. So why are U.S. short-term rates still so much higher than inflation?

What Are Inflation Expectations?

Inflation expectations are forecasts about future inflation. They can come from:

-

Consumers, often measured by surveys such as the University of Michigan’s Survey of Consumers.

-

Professionals and markets, usually measured through financial indicators like breakeven inflation rates.

Expectations matter because they influence spending, saving, and Federal Reserve decisions on interest rates.

Inflation Expectations According to Consumers

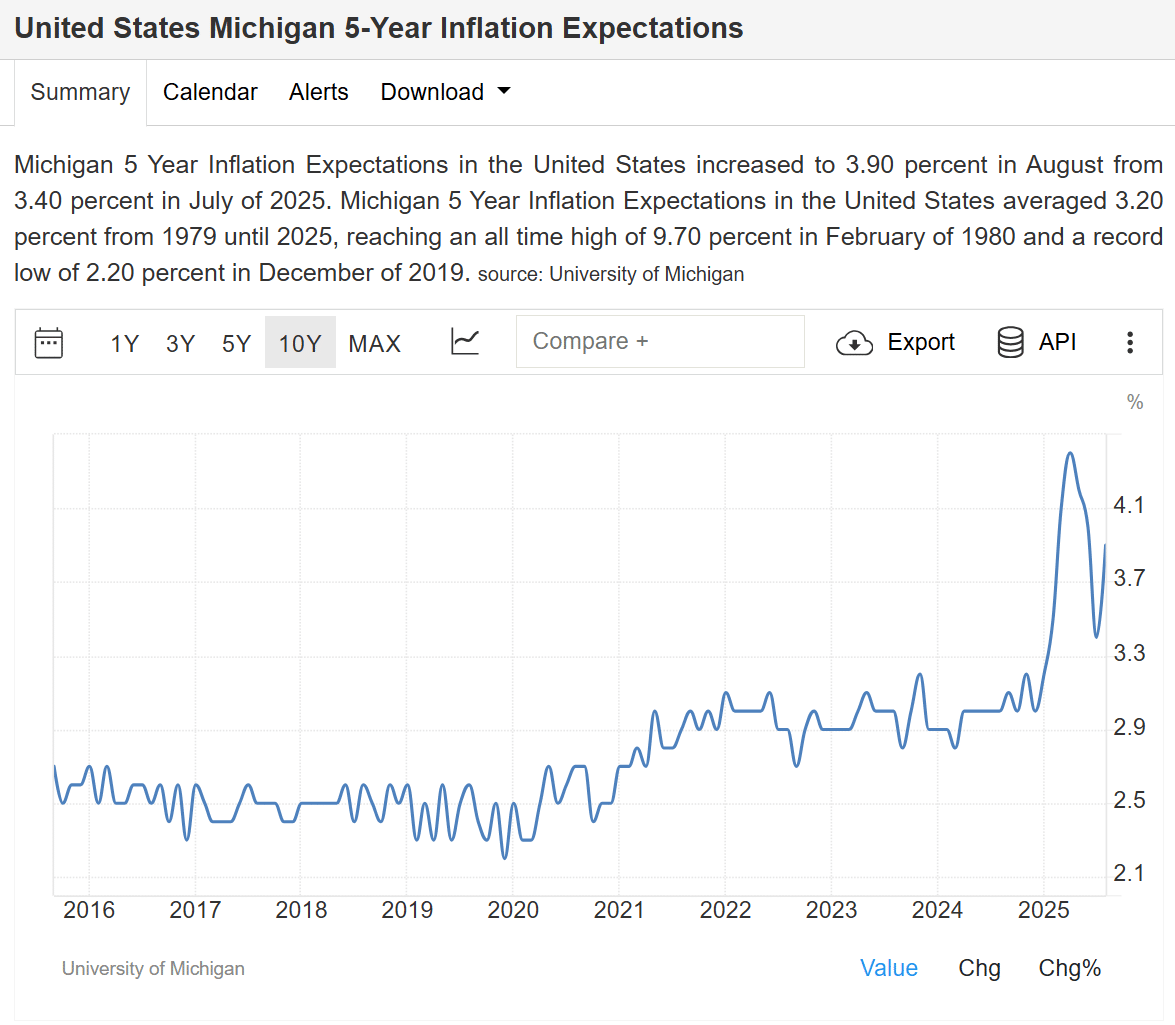

If we listen to Mr. Powell, the main concern is that tariffs could reignite inflation. The most common way to measure that concern is through consumer inflation expectations, captured in the University of Michigan Survey of Consumers, which tracks expected inflation over the next five years (source: Trading Economics).

In our opinion, consumer expectations can be summed up as: “Once you burn yourself on hot milk, you blow even on yogurt.”

This is not to say consumers are unintelligent, but historically, their track record of forecasting inflation is poor—often the opposite occurs. For example, consumers completely missed the inflation surge of 2021–2022. Having been caught off guard once, are they now overestimating inflation risks?

What Is the Breakeven Inflation Rate?

The Breakeven Inflation Rate is a market-based measure of expected inflation. It is calculated by comparing the yields of regular Treasury bonds and Treasury Inflation-Protected Securities (TIPS).

In simple terms:

-

If breakeven inflation is 2.5%, markets expect average inflation of 2.5% per year over the specified time horizon.

-

It represents professional and market-based expectations, often more reliable than consumer surveys.

Comparing Consumers vs Professionals

Here’s how current inflation expectations differ:

| Group | Current 5-Year Expectation | Historical Accuracy | Notes |

|---|---|---|---|

| Consumers (Michigan Survey) | 3.9% | Poor – missed 2021–22 spike | Often biased upward, reacting emotionally |

| Professionals (Breakeven Rates) | 2.5% | Stronger – predicted 2021–22 surge | Market-driven, closer to long-term averages |

This contrast shows why breakeven rates are a more trustworthy guide for policymakers.

Why Inflation Expectations Matter for the Fed

We believe consumers are wrong. Tariffs can be inflationary, but primarily in the short term. Over time, tariff levels can be adjusted, and many products may be exempted.

This brings us to the bigger problem: the Federal Reserve’s decision-making process. The Fed controls more than $6.5 trillion in assets, making it the world’s largest hedge fund. Yet its policy choices seem based more on beliefs and random indicators than on a structured framework.

As a former hedge fund manager, I can confirm that successful portfolios are not built on vague expectations. They are built like business plans, addressing multiple scenarios before any position is taken. The Fed should adopt the Breakeven Inflation Rate as a core part of its decision-making process, given its proven track record.

Instead, journalists often reference the Fed’s “favorite gauge for inflation” with misplaced respect, even though it frequently leads to poor forecasts. Markets remain the best predictor of future inflation.

The issue is not just whether Powell is right or wrong. The real problem is that Powell never outlined a clear decision-making framework for interest rates before his appointment. He was effectively given a blank check. That is the true error.

Key Takeaways

-

Consumer inflation expectations (3.9%) are historically unreliable, often too high.

-

Breakeven inflation rates (2.5%) reflect professional forecasts and are a better predictor.

-

The Federal Reserve should base decisions more on market indicators and less on survey data.

-

The problem is not only leadership but the absence of a clear, structured decision-making process