What Markets Are Pricing Into US Government Debt

How worried should investors really be about US government debt?

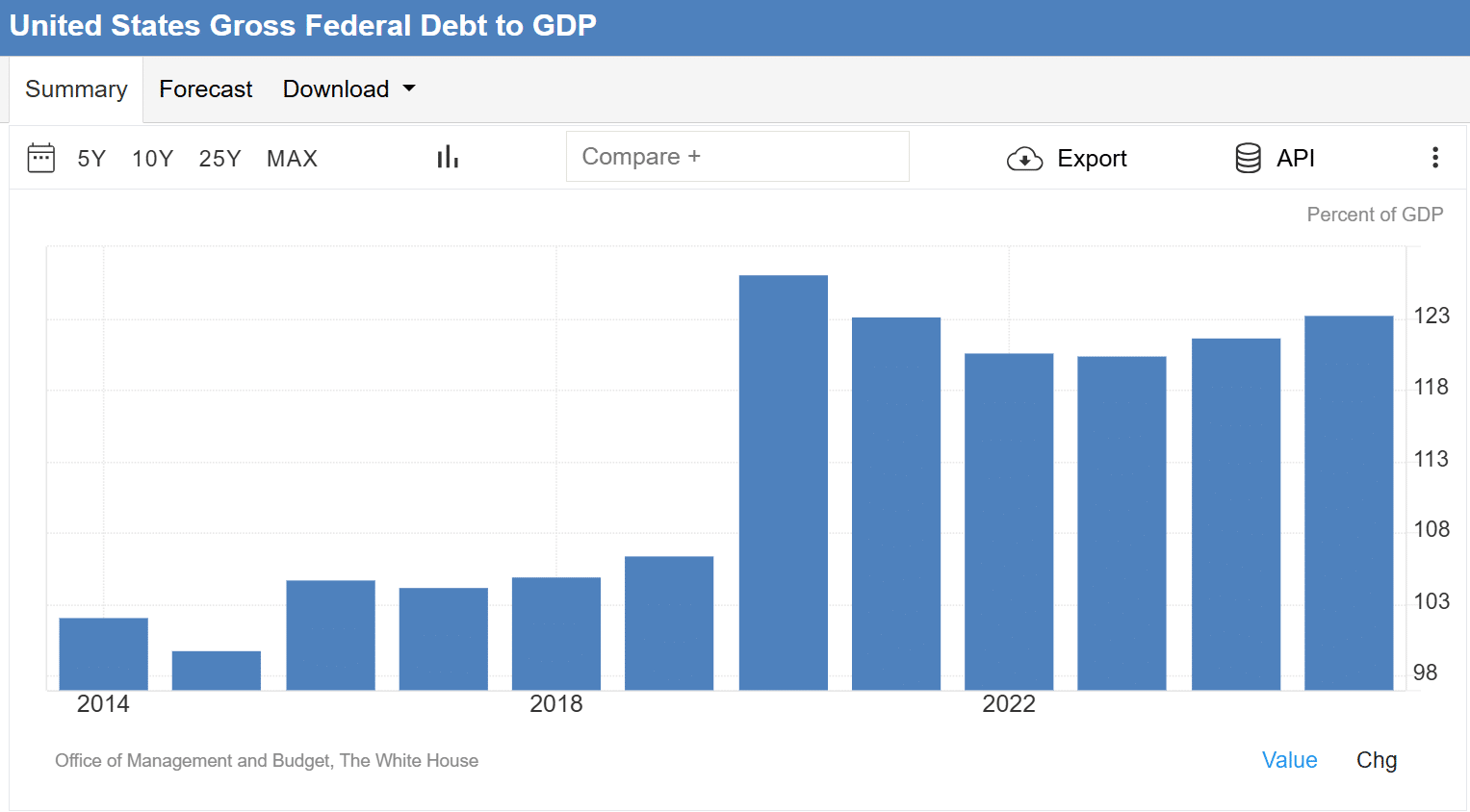

At first glance, the numbers justify the alarm. US debt-to-GDP has risen from around 100% before COVID to approximately 123% by the end of 2025.

Total federal debt now stands at roughly USD 36.5 trillion, according to TradingEconomics. That trajectory has already cost the US its AAA rating. Major agencies have downgraded the U.S. sovereign credit rating to AA+.

So the concern looks legitimate. But do markets actually share it?

What Credit Default Swaps Reveal About US Default Risk

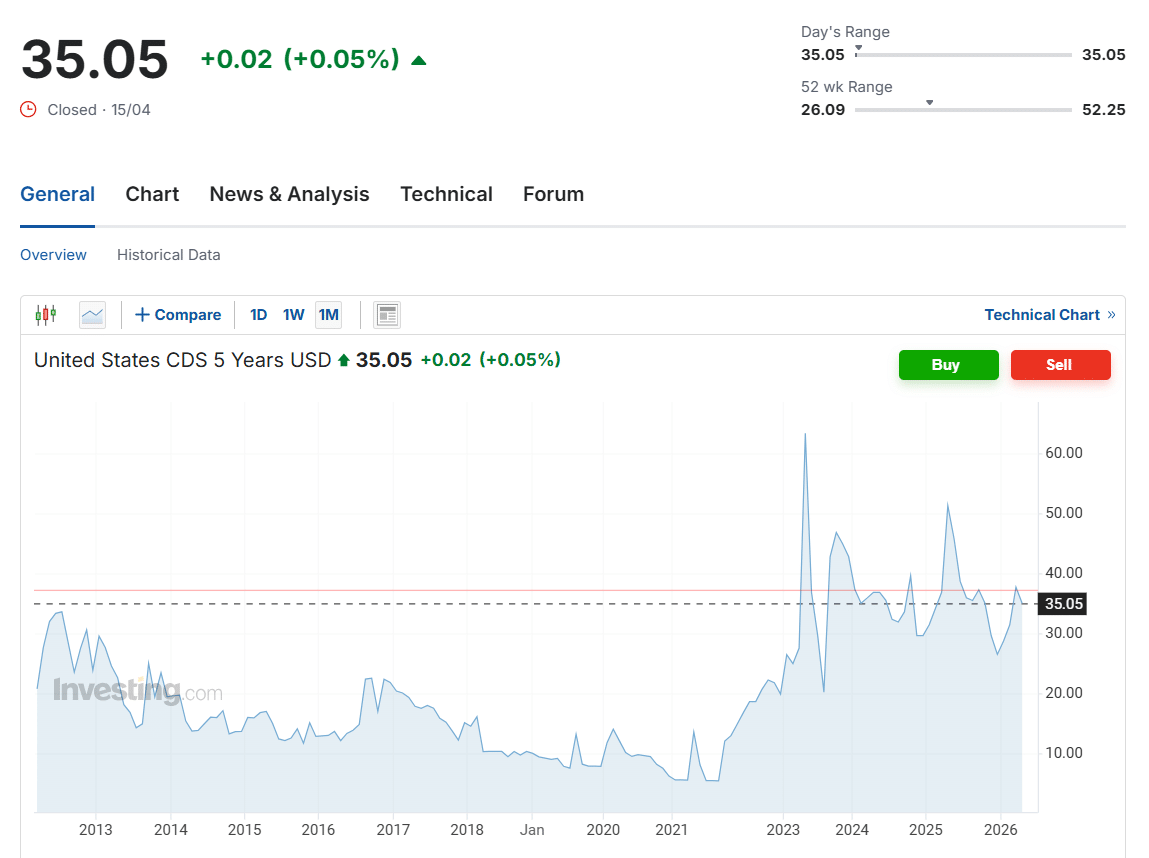

Let’s turn to the credit default swap markets, courtesy of Investing.com.

CDS markets broadly track the dynamics of the debt/GDP ratio. However, current pricing tells a different story. Insurance on US sovereign debt costs around 0.35% per annum on the notional amount. That figure suggests the probability of a US default remains largely theoretical. CDS dealers also report very limited demand for this protection. Global CDS notional outstanding totals roughly USD 30 trillion, yet only USD 3–4 billion links to US sovereign risk.

So what do we have?

- Debt/GDP at 123%.

- Outstanding debt of USD 36.5 trillion.

- Insurance is priced at 0.35% per year, with a few buyers.

Markets are not pricing in a meaningful probability of default.

Do Markets Expect Runaway Inflation

Fine, perhaps the US will not default. But surely this debt burden will eventually trigger runaway inflation? That narrative is common. Does market pricing support it?

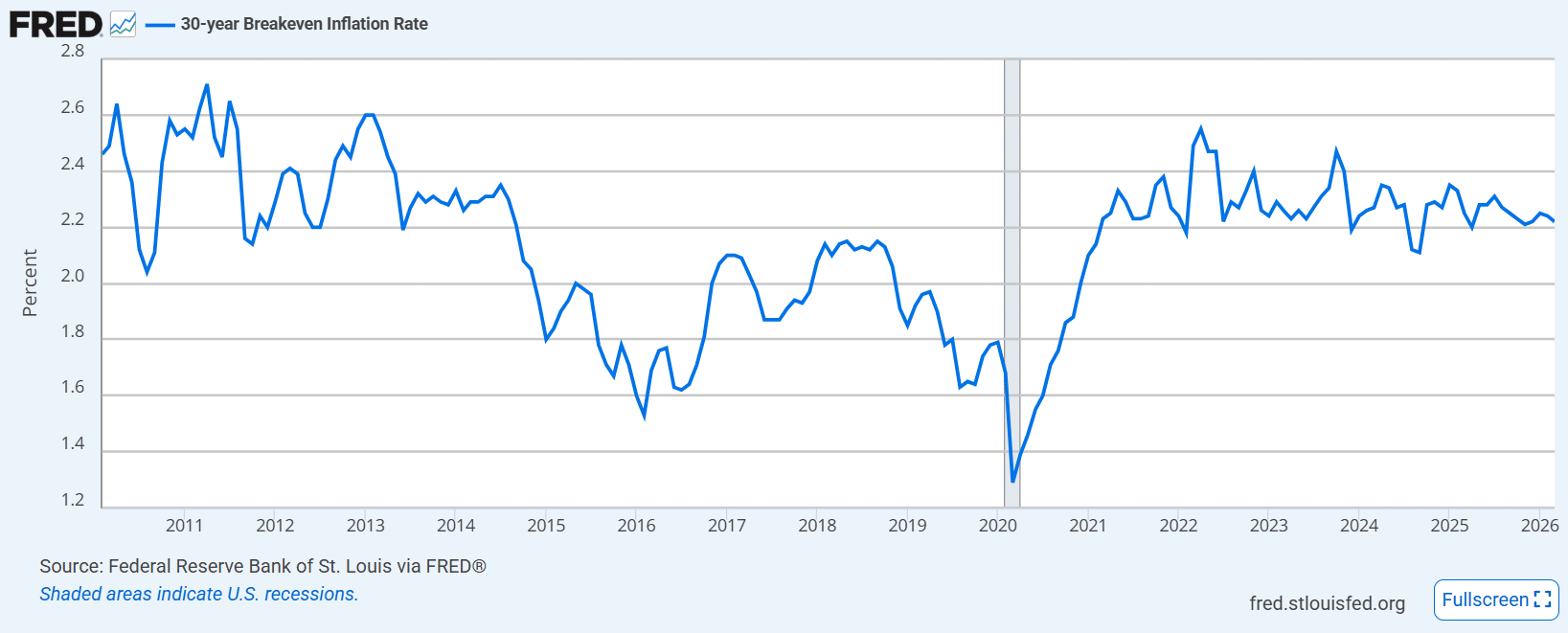

Let’s turn again to the markets. Specifically, the 30-year breakeven rate — the market-implied average inflation over the next 30 years, courtesy of the Federal Reserve Bank of St. Louis – FRED.

Somewhat surprisingly, the answer is no. Markets do not expect runaway inflation. Instead, they imply roughly 2.2% annual inflation over the long term. That level broadly matches expectations from the early 2010s. Long-term inflation expectations have stayed relatively stable over the past several years, clustering around that figure.

The Implicit Market View: Financial Repression

This brings us to our conclusion. Yes, US Government Debt/GDP at 123% is elevated. Yes, rating agencies have downgraded the US sovereign credit rating. Yet market pricing suggests investors expect neither a default nor runaway inflation.

If markets expect neither scenario, what do they expect? The implicit answer is financial repression — a prolonged period of moderate growth during which nominal GDP expansion gradually absorbs the debt burden, rather than an abrupt resolution.

Where Policy Could Realistically Act: Healthcare Spending

We cannot know with certainty why markets hold this view. However, we ran a simple comparison of US government expenditures with those of other OECD countries and found something noteworthy. US healthcare spending runs at roughly 17% of GDP. Most other developed economies spend only 7–9%. The US also spends somewhat more on defense and interest. Still, the most significant divergence lies in healthcare.

In that sense, the most obvious low-hanging fruit is not higher taxes, reduced government services, or default. It is structural efficiency improvements in healthcare spending.