Start every trading day with a quick, actionable snapshot of global markets, key earnings, and the biggest movers across US, Europe, and Asia. Get the insight before your first coffee is gone.

May 20, 2026 | Issue 156

US Bond Market Outlook May 2026

Nikolay Stoykov

Managing Partner at Alaric Securities

We have written positively about bonds before, most recently in October 2025. However, the war in the Middle East has increased inflation expectations for 2026. As a result, we decided to take another look — are US Treasury bonds a buy, a sell, or a hold?

With all these factors in mind, the current outlook in the bond market has become more complex than before.

US Treasuries, especially long-dated ones with maturities of 10 years or more, continue to offer compelling value for long-term investors. Yes, prices have declined, and yields have risen.

However, the rationale for owning those securities remains largely intact compared to the end of 2025. To further clarify, our bond market outlook now reflects this shift in sentiment.

Here is why:

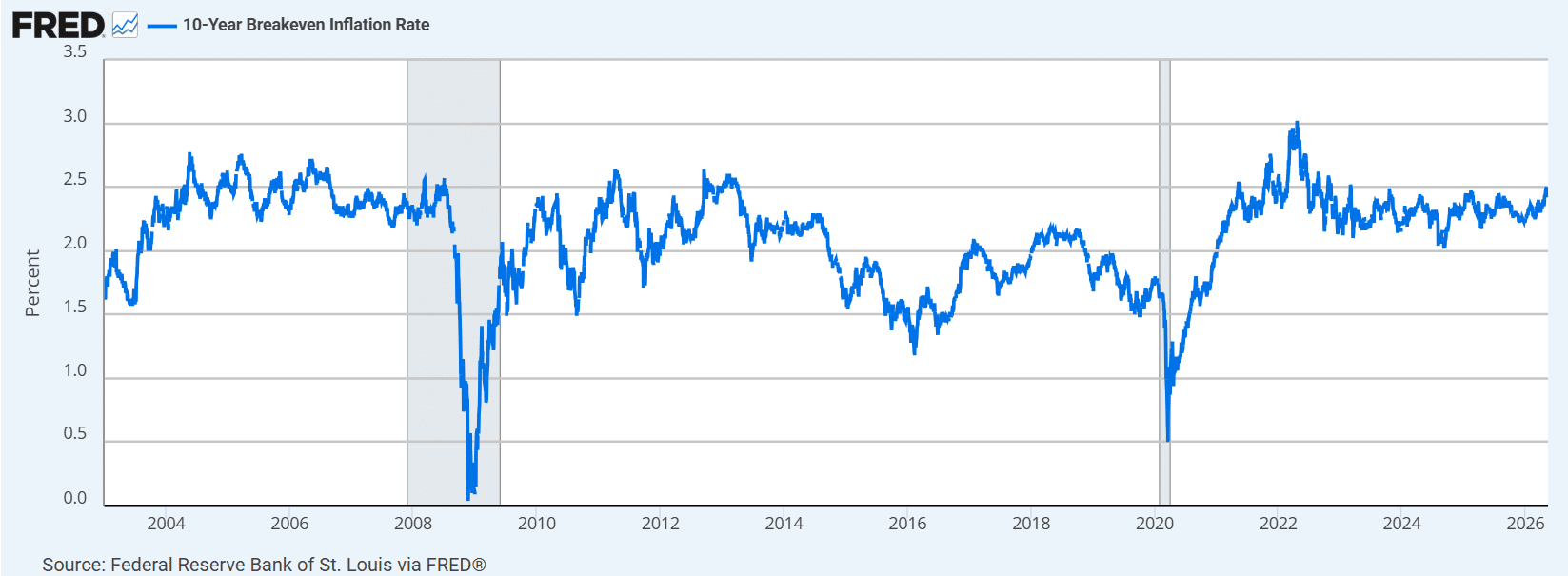

1) 10-Year Inflation Expectations Remain Relatively Benign

Courtesy of the Federal Reserve Bank of St. Louis, you can see that despite oil prices nearly doubling over the last three months, 10-year inflation expectations remain relatively subdued at 2.47% per year. That is up from 2.25% at the end of 2025.

These inflation expectations are an essential factor shaping current expectations for the bond market outlook. Especially for long-term investors.

Yes, the conflict in the Middle East will likely have an inflationary impact. However, markets currently do not expect that impact to be particularly significant over the long term.

Taken together, this continues to support a constructive outlook for the bond market. Investors may want to review this when considering their own portfolio decisions.

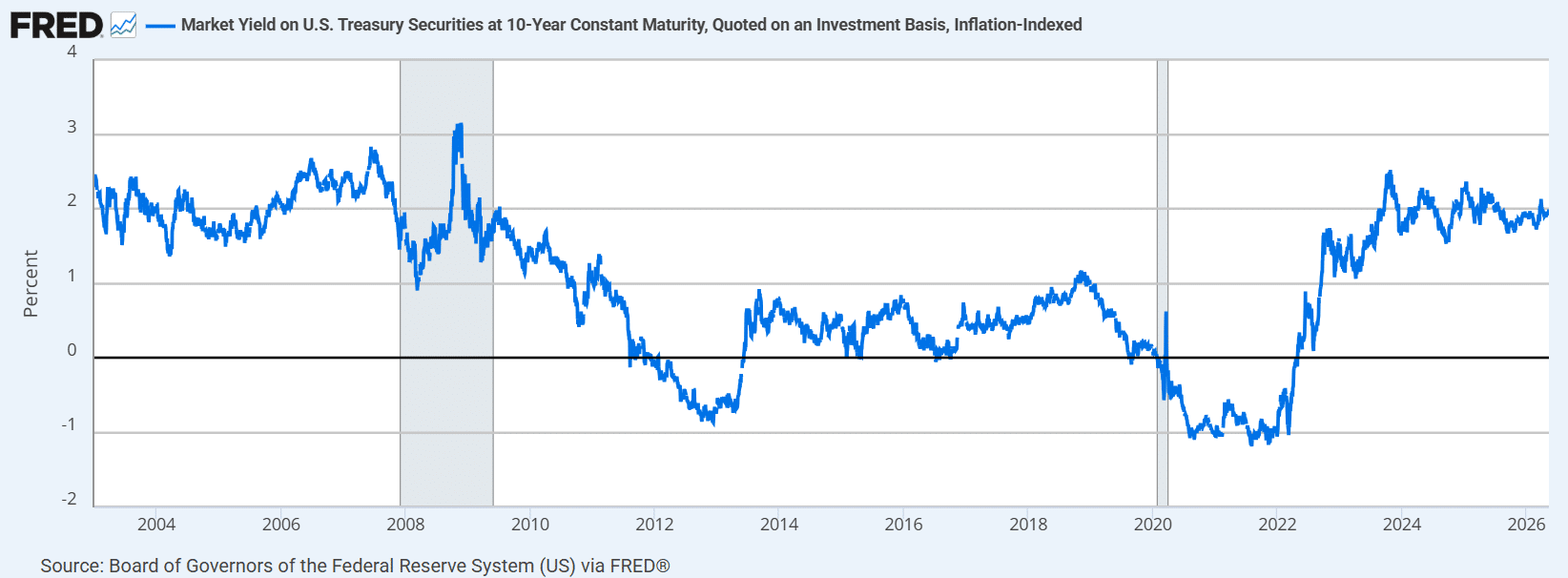

2) Real Rates Are Near 20-Year Highs

Pictured above, again courtesy of the Federal Reserve Bank of St. Louis, are 10-year real interest rates. These rates are closely monitored when discussing the bond market outlook for investors.

The current level of nearly 2% per annum suggests that long-term real rates are already historically restrictive relative to post-2000 norms. The post-COVID shock in interest rates was driven partly by rising inflation expectations.

Still, a substantial portion of the move was also due to long-term real rates normalizing from deeply negative levels.

In the current environment, this suggests that while rates can continue to rise, further increases would likely need to be supported primarily by a meaningful rise in inflation expectations. All of these factors play into the bigger picture for the bond market outlook.

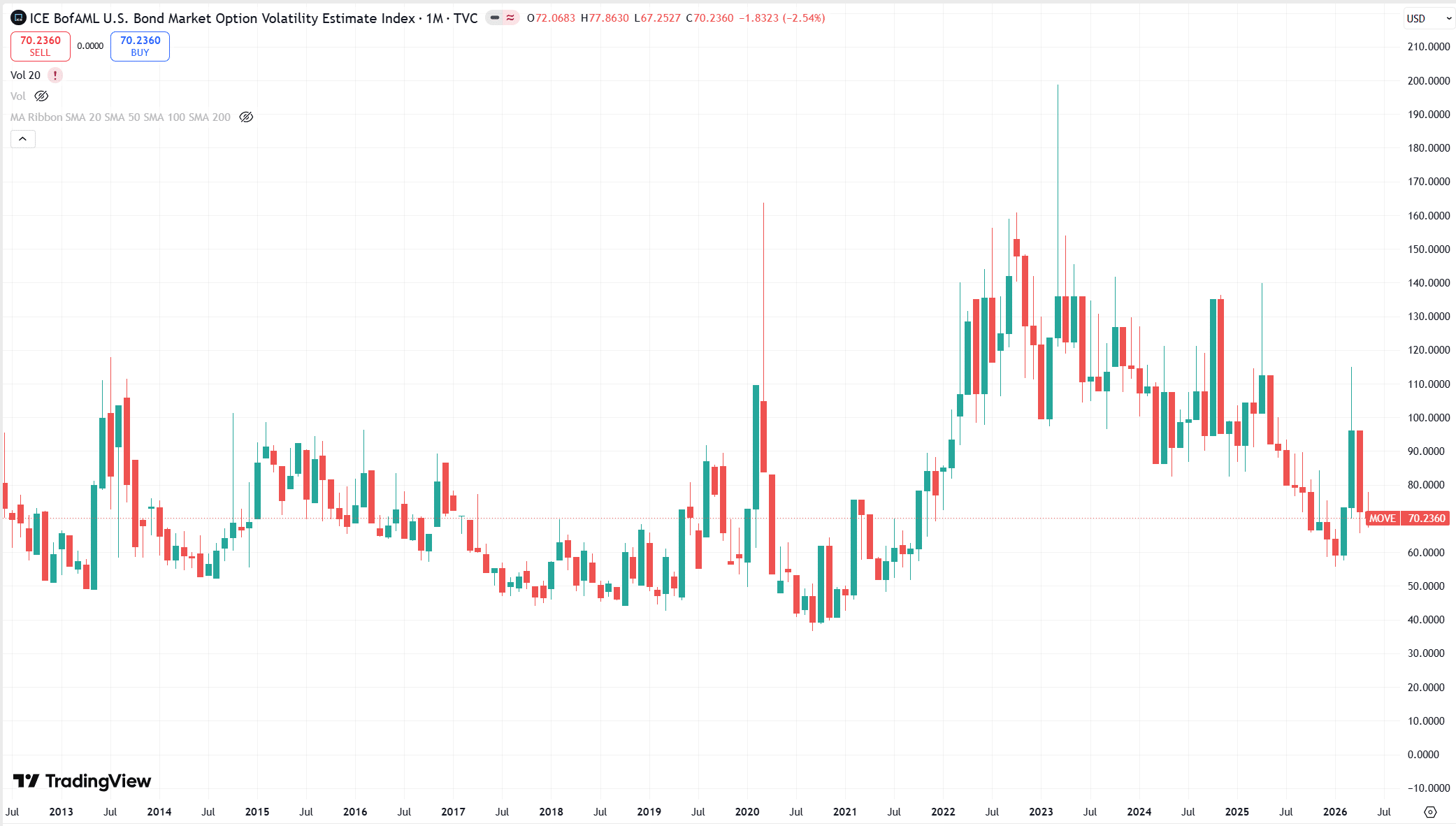

3) Volatility Expectations for US Treasuries Remain Contained

Shown above (source: TradingView.com) is the MOVE Index, a volatility measure tracking a broad basket of U.S. Treasuries.

As you can see, despite the inflationary impulse created by the conflict in the Middle East, Treasury volatility expectations remain relatively subdued.

This does not necessarily mean that yields are expected to decline. Rather, it suggests that markets are not currently pricing in large moves — either higher or lower — over the foreseeable future. This is relevant to any bond market outlook assessment investors may consider.

Even if yields continue to rise, the move would more likely resemble a gradual drift higher rather than a disorderly repricing.

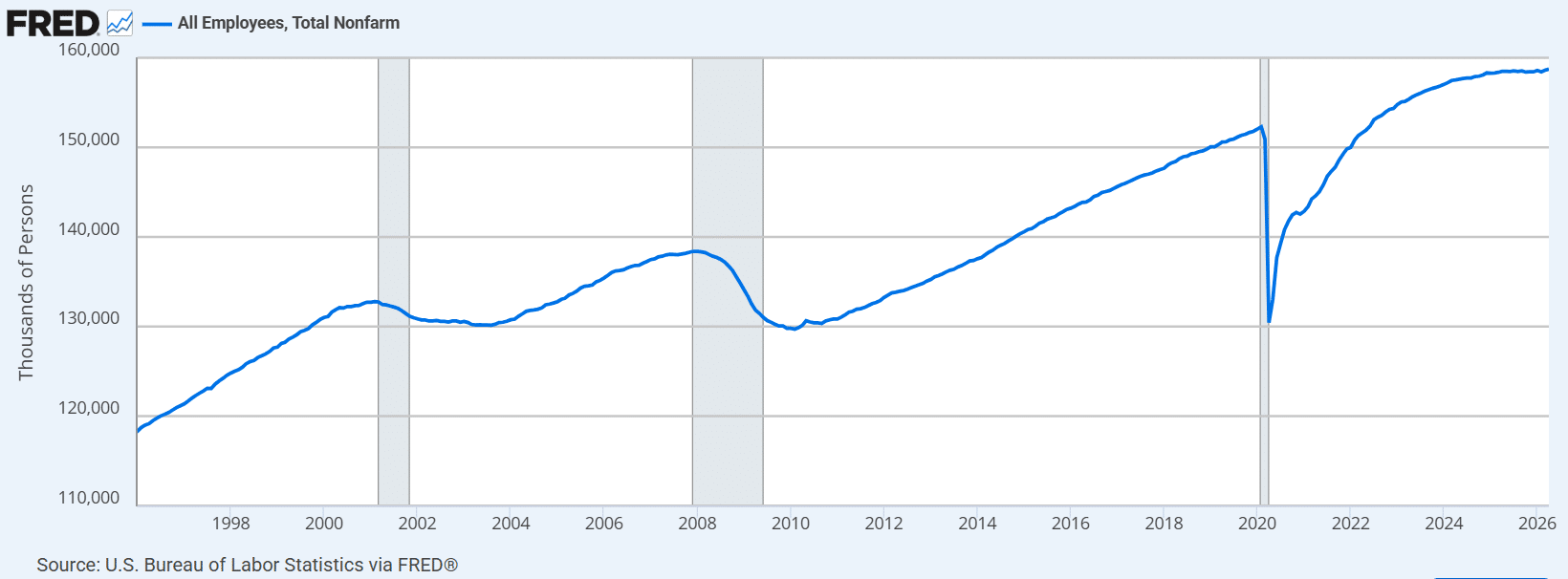

4) We Are Likely in the Late Stages of the Business Cycle That Began in 2020

According to the Federal Reserve Bank of St. Louis, the total number of employees in the US has been flattening.

Historically, this has often been a reliable indication that the business cycle is approaching its later stages — particularly during periods such as 2000–2001 and 2007–2008.

As we look at the late-stage business cycle, it’s important to factor in the bond market outlook. This should be considered when planning for the next economic phase.

This does not necessarily imply that a deep recession is imminent. However, it does suggest that future economic growth in the US is likely to be more subdued and increasingly dependent on lower borrowing costs, which is closely tied to the evolving outlook for the bond market.

Disclaimer

The articles, podcasts, and newsletters from Alaric Securities OOD are classified as marketing communications. The views expressed are solely those of the individual authors affiliated with Alaric Securities OOD and do not necessarily reflect the views of the company, its subsidiaries, or affiliates. This content is provided for informational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security, digital asset (such as cryptocurrency), or other financial instrument. Third-party content is included solely for informational purposes and does not reflect the views of Alaric Securities OOD. All investments involve risk, including the possible loss of principal. Past performance is not indicative of future results. References to third-party companies, logos, or trademarks are used under fair use/fair dealing principles for analysis and commentary.

Stay Ahead with Alaric Securities Newsletters

Traders and investors don't need more information - they need better information. That’s what we deliver!

Step back from the daily noise. Each issue explores market trends, industry shifts, trading opportunities, and exclusive updates — learn what's shaping the markets, not just what's trending online. Ready to get the edge?