Liquidity Crisis 2025: The Hidden Risk in Crypto and Emerging Equities

The year 2025 has emerged as a critical turning point for understanding market risk. Investors, traders, and regulators alike have watched as a series of liquidity crises swept through both the crypto space and emerging equity markets, particularly in Asia. Though each situation had its own unique triggers and timelines, the core issue remained consistent: when real liquidity dries up, the illusion of stability disappears, leading to chaotic price movements.

This analysis takes a closer look at the dynamics at play in both the crypto market and Asian equities. We’ll explore how structural obstacles, confusing regulations, and shifting global capital flows have all contributed to the increasing significance of liquidity in today’s investment landscape.

A closer look at this complex narrative reveals three key insights: understanding the essence of liquidity (and illiquidity), comparing crypto to traditional emerging equities (with a spotlight on Asia), and examining why the US market continues to represent a benchmark for reliable, tradeable liquidity – especially when it comes to short selling and active trading strategies that support genuine price discovery.

1. What Is Liquidity, Really? Why It Matters in 2025

Liquidity is often described in simple terms – how easily assets can be bought or sold without moving the price dramatically. In practice, it’s much more than raw trading volume. It is the total of market depth, diversity of participants, regulatory and operational clarity, and the presence of functioning hedging instruments (like derivatives and futures). Real liquidity means that assets can be monetised – at transparent prices – under both normal conditions and in moments of market stress.

In the past, investors may have taken this for granted – at least in the largest global markets. But 2025 has shattered complacency. From altcoins crashing by 70% in three weeks, to prominent Asian equity indices swinging wildly after single fund outflows, the message is clear: liquidity is both a technical and psychological phenomenon. When confidence in access vanishes, so does much of the perceived value of an asset.

2. Crypto: A Liquidity Mirage and the Fallout of Sudden Drought

Let’s look closer at the anatomy of the 2025 crypto bear market. In October 2025, the crypto sector faced one of its sharpest, deepest sell-offs since the “DeFi winter” of 2022-23. The proximate cause was clear – a confluence of new regulations (especially in Asia), cyberattacks against leading protocols, and enormous liquidations triggered by over leveraged participants. Asia is undergoing a transformative shift in its approach to cryptocurrency regulation, moving from cautious observation to proactive integration. The crypto space remains exceptionally responsive to regulatory news. Announcements of compliance obligations or enforcement actions can instigate immediate price fluctuations. But beneath the headlines, another pattern emerged: order books on major centralized and decentralized exchanges thinned out rapidly as the market declined, revealing that much of the “liquidity” counted in normal volume statistics was illusory when sellers vastly outnumbered buyers.

As prices tumbled, even “blue chip” coins saw spreads widen and volatility spike, with some digital asset pairs seeing intraday drops exceeding 30%. Decentralized finance protocols essentially shut down as collateral was force-liquidated algorithmically, swamping any attempt at organized market-making. The result: a cascading cycle where price declines forced liquidations, which in turn drove prices ever lower in a self-reinforcing loop.

Why did this happen?

Crypto’s liquidity is highly pro-cyclical: When sentiment is positive, trading volume surges, but almost entirely from one-sided flows and short-term “hot money.” When fear arrives, few want to take the opposite side, and there are no large, committed institutional liquidity providers to cushion the fall.

Infrastructure is fragmented: Assets trade across dozens of exchanges with little true cross-venue arbitrage once volatility spikes. Settlement and margining happen off-chain, introducing extra layers of risk.

The bulk of ownership is concentrated: A small number of whales and early investors control a disproportionate share of supply. This is similar to the low free float seen in certain emerging equity markets, with the added wrinkle that on-chain transparency occasionally speeds up, rather than dampens, panic.

Crypto Market Structure Matters: The suddenness of the October crypto crash isn’t just a technical issue; it is a lesson in what happens when a market lacks foundational plumbing and a deep, natural two-sided flow. There are no reliable hedging vehicles, regulatory frameworks remain inconsistent across jurisdictions, and operational risk is enormous, ranging from hack risk to sudden exchange outages. Unlike traditional markets, no central bank or lender of last resort stands ready to provide emergency liquidity. Ultimately, as the Bank for International Settlements has long warned, crypto remains “a market built on liquidity illusion”.

This is not to say there is no value in blockchain or digital assets. When liquidity is based on hope and FOMO, rather than steady institutional participation and robust market structure, disaster is always only a bad week away.

3. Asian Equities: Structural Liquidity Constraints and Market Behavior

While crypto’s liquidity problems stem largely from newness and regulatory hesitation, Asian equities face a very different – yet equally daunting – set of structural challenges.

The Hard Numbers: Free Float and Market Depth

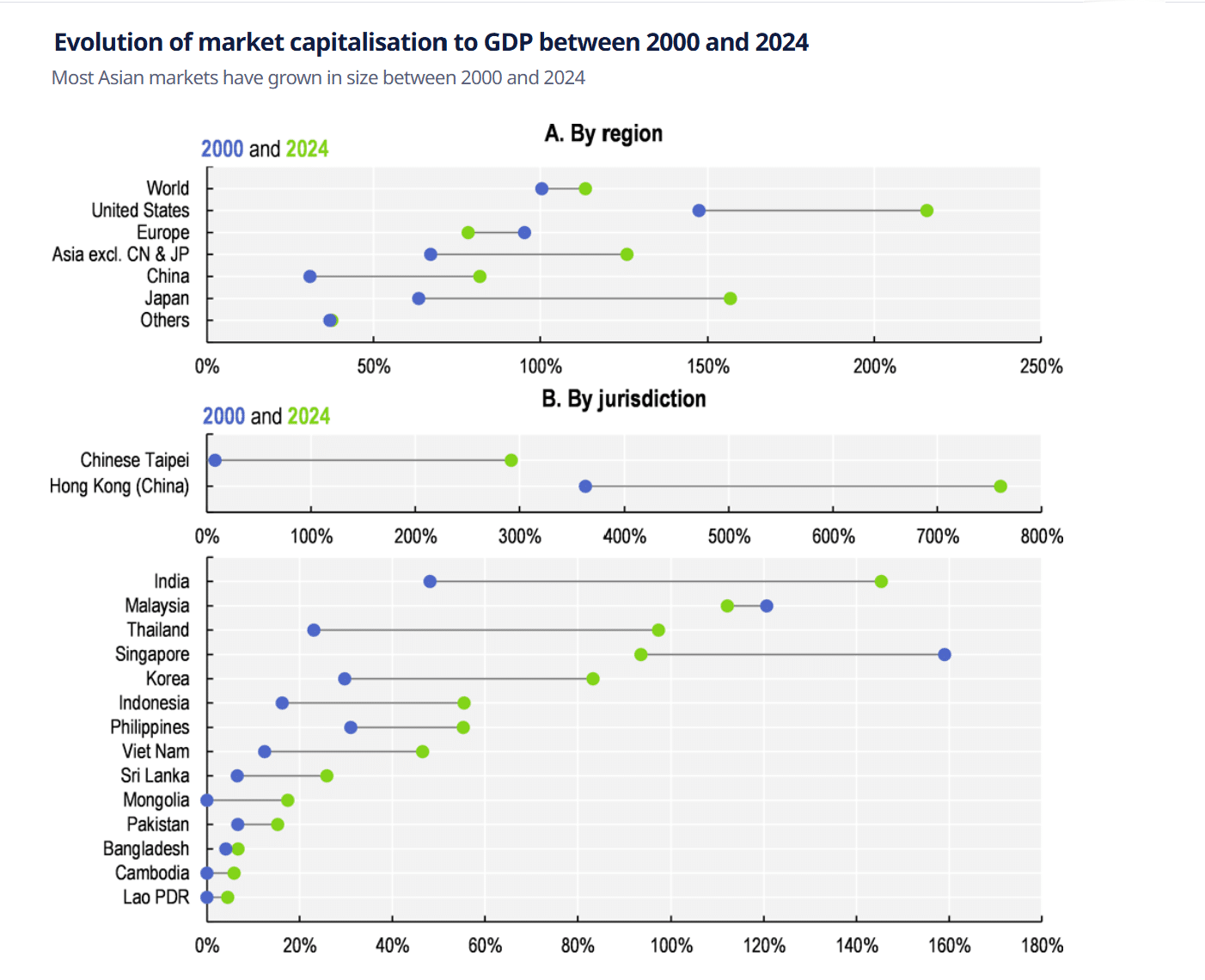

Over the past two decades, Asian equity markets have grown massively in both size and sophistication. Yet for all that growth, the underlying structural issues remain: public float is low, many shares are locked up by governments, families, or strategic investors, and true depth is hard to find outside of a handful of blue chip names.

According to the 2025 OECD Asia Capital Markets report, average free float in Asia is just 35%, compared to more than 80% in developed Western markets. Some markets – like Korea and Hong Kong – are even lower, with free floats dipping below 20% by late 2024. By contrast, in the United States, S&P Dow Jones Indices reports that the S&P 500’s float-adjusted market capitalization methodology typically excludes only 5-10% of shares from index calculations, meaning the vast majority of shares are available for trading.

This isn’t simply a numerical oddity. It fundamentally alters price action and risk management. With so much of the share base locked up, even modest institutional buying or selling can swing prices. When passive global funds rotate in or out (often in response to macro or currency factors, not corporate fundamentals), the resulting volatility resembles that of illiquid penny stocks. Retail investors make up an unusually large share of trading – up to 80% in Korea and over 60% in China. Retail flows are quicker to reverse, more sentiment-driven, and less likely to provide liquidity in stressed conditions.

Operational Roadblocks: Settlement, Regulation, and Currency Risk

Operational friction is another key driver of illiquidity in Asia. There are 17 different settlement cycles across 23 jurisdictions – T+2 in Hong Kong, T+1 in China, T+3 in Indonesia, and so on. These differences aren’t just a paperwork hassle; they mean that cross-border strategies are much more difficult, expensive, and prone to operational mishaps.

Other issues?

Currency convertibility is limited, and restrictions on capital movement make it challenging for international investors to confidently repatriate gains or hedge exposures. Currency hedging itself is expensive and unreliable – forward markets for currencies like the rupiah or ringgit are thin, and hedging costs can wipe out potential returns.

Sectoral restrictions prevent foreigners from fully participating in many of the region’s most exciting industries (for example, banking, telecoms, and natural resources), limiting the benefit of index inclusion and keeping global capital on the sidelines.

Regulatory reporting and corporate governance remain uneven, with inconsistent disclosure standards, related-party transactions, and modest board independence outside a few large markets.

The cumulative effect is visible. Even when valuations in Asian markets look attractive compared to the US or Europe (as measured by price-to-book ratios, which have consistently lagged global averages), the lack of reliable two-way liquidity keeps long-term capital from flowing in.

Reform Efforts in Korea, China, and Japan: The Push for Value

We saw a renewed effort by Asian leaders to improve liquidity and market quality.

Japan’s Corporate Reform and Governance Improvements: The Tokyo Stock Exchange (TSE) initiated significant reforms in 2023, focusing on corporate governance and cost-of-capital management. This includes encouraging shareholder-conscious management and raising the threshold for independent outside directors on boards. These reforms have led to many companies adopting shareholder-friendly measures, improving disclosures, and increasing dividends.

Korea’s Value-Up Program: South Korea introduced the Value-Up Program in 2024, aiming to enhance corporate culture, transparency, and accountability, particularly targeting chaebols to reduce controlling-family shareholder influence. This program has garnered bipartisan support and includes measures like reducing the financial investment income tax to encourage shareholder participation.

China’s Market Reforms: China began implementing reforms in 2023 to improve stock market performance. These reforms include enhancing corporate governance, strengthening market oversight, raising IPO standards, and increasing shareholder protections. Authorities are also focusing on expanding institutional equity ownership and boosting shareholder returns through higher dividends and buybacks.

Regional Impact and Expansion: The success of Japan’s reforms has encouraged other Asian countries to follow suit. Various governments are now rolling out their own corporate reform programs aimed at raising dividends and share buybacks. These efforts across Asia are part of broader economic restructuring goals, emphasizing more sustainable growth and better alignment with global investor expectations.

Overall, these reforms aim to strengthen market fundamentals, increase transparency, and enhance shareholder value across Asian markets. In 2025, traders in Asian markets are facing a uniquely complex and dynamic environment shaped by persistent volatility, shifting trade frameworks, and rapid technological disruption. These factors are directly impacting both risk management and opportunity sets for active participants.

Key 2025 Developments in the Region Relevant for Traders

Heightened Volatility and Trading Opportunities: The first half of 2025 brought sharp swings in Asian equities, driven by global macro uncertainty, currency fluctuations, and rapidly evolving trade policies – particularly the newly negotiated US-China and pan-Asian tariffs. This volatility, while challenging, has created tactical opportunities for traders who can identify short-term dislocations and respond flexibly.

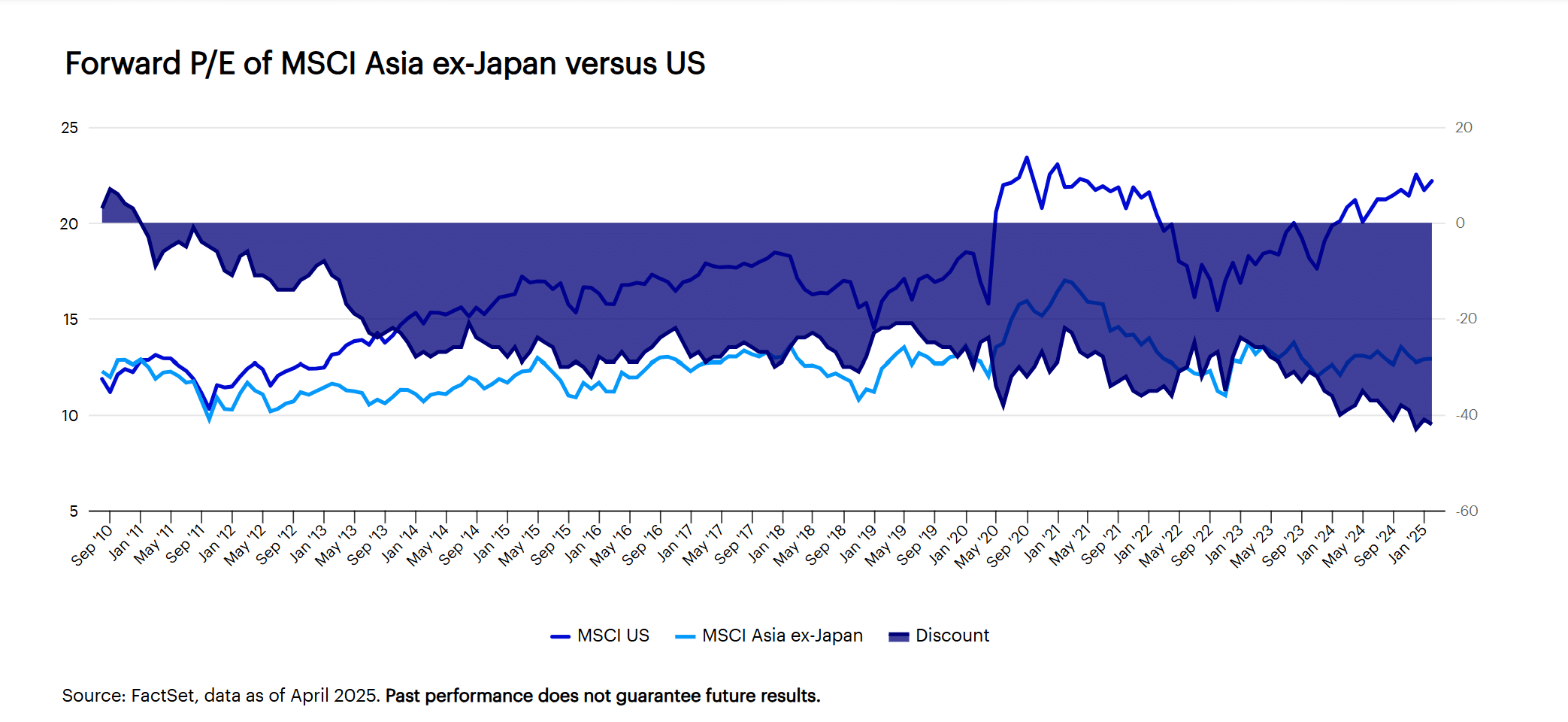

Valuation Rebound and Liquidity Windows: Asian equities now trade at a significant discount relative to developed markets, especially as recent corrections in late 2024 reset valuations. With earnings growth stabilising and macro risks being repriced, this has opened attractive entry points, especially for those with a longer time horizon and the ability to navigate short-term noise. Active traders can leverage these apparent mispricings – particularly as market sentiment whipsaws between fear and relief.

Diverging Country and Sector Themes

The region is no longer moving in unison; instead, country-specific drivers dominate. For example:

Japan: Corporate governance and index reforms (TOPIX rebalancing) are incentivizing smaller companies to enhance liquidity and engage shareholders, generating flows into previously neglected names.

China: Despite headline economic slowdown and deflation risk, targeted government intervention and AI innovation have fueled sharp rally attempts, but also quick reversals. Opportunities exist for those nimble enough to navigate sector rotations and state-influenced policy shifts.

India and Taiwan: India’s favorable tariff status and Taiwan’s emergence as an AI hardware hub have created relatively resilient pockets for traders seeking lower correlation to China-driven risk.

Korea: Defense companies are benefiting from global tensions, while the market’s structural reforms continue to attract focused flows.

This fragmentation means cross-market relative value and rotation trades are increasingly important. Additionally, we observe:

Technology and AI as Trading Drivers: The “DeepSeek effect,” with the dramatic drop in AI computing costs, led to a valuation de-rating of semiconductor stocks but also set the stage for a new cycle of sector leadership, creating both risks and outsized opportunities in tech names linked to AI and automation.

Persistent Macro Risks and Tail Events: The 2025 environment remains headline-driven. Shocks related to tariffs, central bank moves, or geopolitics can trigger rapid de-risking. Traders must maintain robust risk management and position sizing, especially as correlations spike during high-impact news.

Short Selling and Tactical Approaches: With frequent sharp rallies and drawdowns, short-term short selling and long-short equity strategies are finding renewed relevance. The infrastructure for shorting remains best in Japan, Hong Kong, and Korea, while trading liquidity can still evaporate in smaller or more restrictive markets, requiring active monitoring and flexibility.

Liquidity Management Remains Central: Despite improvement efforts, actual liquidity conditions can change rapidly—with order books thinning during selloffs and spreads widening, particularly in mid- and small-cap names. Traders should favor high-turnover instruments and remain alert to sudden shifts in bid-ask dynamics, especially around macro headlines or earnings cycles.

2025 is a year where macro-driven volatility, policy adaptation, and technological innovation create both significant risks and rich opportunity for sophisticated traders in Asia. The most successful participants are those combining granular, bottom-up fundamental research with nimble, tactical trading, robust risk controls, and a readiness to capitalize on rapidly shifting sentiment and liquidity regimes.

China’s large SOEs were pressed to focus on return-on-equity (ROE) rather than just net profits, as new regulatory frameworks pushed for greater transparency and dividend discipline. Korea launched its “Value-Up Program,” modeled on Japanese reforms, to incentivize voluntary value-enhancement plans, improve investor engagement, and create new indices to focus investor attention on best-in-class performers.

These are steps in the right direction. However, as the OECD notes, progress remains slow, and the combination of low free float, inconsistent infrastructure, and fragmented markets continues to weigh on their global standing.

Private Markets and Financial Inclusion

Private equity and venture capital are growing in Asia, but from a much lower base than in the West. Many fast-growing Asian companies remain bank-financed or government-supported, not turning to capital markets until much later in their lifecycle. This means early-stage innovation stays walled off from broader investor participation, reducing market dynamism and reinforcing the “liquidity bottleneck,” which traps much of Asia’s real economic potential.

Retail investor participation, vital for true market depth, is rising but remains low as a share of the population, despite the equity trading boom in some locations during the years leading up to 2025. Efforts at boosting financial literacy and fintech penetration are ongoing, but more will be needed to build a large, resilient base of stakeholders who view markets as a long-term destination for savings.

4. Macro Backdrop: Global Capital Flows, Trade, and Policy Shifts

Asia’s growth is impressive amid fragility. In 2025, Asia’s macro story is one of resilience challenged by structural headwinds. The IMF projects regional growth at a robust 4.5% this year – much stronger than developed markets – but also warns of vulnerability to external shocks: new trade risks, fluctuating currency values, rising financial costs, and potential debt issues across several economies.

US-China trade tensions remain the largest wild card. The past twelve months have seen reciprocal tariffs lowered and a 90-day truce between major partners, injecting some optimism and propelling sharp rallies in markets like Japan (with the Nikkei hitting all-time highs). But volatility remains high; a single new export control or incident can ripple through supply chains, sparking sharp selloffs and reveals just how quickly “liquidity” can disappear in segmented, shallow markets.

India, by contrast, is cited as a more resilient story, leveraging its exemptions in global trade and booming domestic consumption. Taiwan, now a hub in the global AI and hardware supply chain, benefits from a much healthier PBR, underpinned by sector innovation and global investor confidence.

Domestic Efforts: Policy and Infrastructure

Policymakers across Asia are acting to shore up trust and liquidity:

- Countries are simplifying listing procedures, creating alternative exchanges, and working on bringing in more institutional participation via pension reform.

- New digital and fintech platforms are being rolled out to lower retail entry barriers, boost transparency, and improve trade execution

- Governments are refining bankruptcy and insolvency rules, aiming to direct capital to its most productive use.

Still, these reforms are coming alongside the realization that global capital is both selective and quick to flee. When market structure is weak, reversals can be self-reinforcing.

5. US Equities: The Benchmark for True Liquidity

When compared to the difficulty of exiting positions in crypto or Asian equities, the US stock market stands out as a liquidity superpower. Why?

Market depth: US markets feature deep order books and massive institutional participation. Even in times of volatility, there’s always a two-sided market for both stocks and options.

Regulatory clarity and operational efficiency: Centralized clearing, a single settlement cycle (T+2, moving to T+1), and strong investor protections mean execution risk is largely contained.

Hedging and risk management: The breadth and depth of derivatives in the US is unmatched. Index, sector, and single-name options allow institutional and retail traders alike to hedge exposures. Short selling is well regulated but almost always possible – a crucial mechanism for price discovery when fundamentals deteriorate.

Transparency and governance: Disclosure requirements in the US, coupled with active and diverse board structures, make it easier for investors to analyze risks and opportunities.

For trading firms and investors focused on short selling, risk management, and tactical execution, US equities remain the reference point: if you need to place a large trade without moving the market, hedge your risk, and exit when needed, the US is still the best game in town.

6. Short Selling and Market-Making

The liquidity crises of 2025 in both crypto and Asian equities underscore a key truth – active risk management isn’t possible in structurally illiquid markets. For a trading or investment firm, the ability to short sell, hedge, and actively manage positions is not a luxury, but a necessity.

Short selling: In the US, efficient borrowing programs, transparent reporting, and robust institutional participation make it possible for traders to profit from overvaluation or hedge downside exposures. In Asia, this is possible in a limited way in the biggest markets (Hong Kong, Japan, Korea), but is often expensive, restricted, or operationally complex.

Arbitrage and systematic trading: Systematic strategies rely on both the presence of liquidity and the absence of significant market frictions. Fragmentation, high frictional costs, and inconsistent settlement stymie such strategies in most Asian markets and nearly all crypto venues.

Market-making: The presence of active market-makers – backed by deep pools of capital – ensures two-way markets and tight spreads in places like the US, while their absence in more fragmented markets exacerbates volatility and widens spreads during stress.

7. The Path Forward: Reform, Technology, and the Global Search for Liquidity

The themes of 2025 – crypto’s crash, Asia’s volatility, and America’s comparative resilience – are not simply stories of regional fate. They are actionable blueprints for how liquidity can be strengthened and how investors should strategize in a multipolar, riskier world.

Policy Priorities for Asia

Boosting free float and institutional ownership. Governments and exchanges must incentivise existing owners to free up more shares for open-market trading and lower restrictions for foreign capital.

Deepening derivatives markets. Regulators must encourage the development of robust, transparent index and single-stock futures and options that are both liquid and accessible.

Harmonizing settlement cycles and reporting standards. Moving toward pan-regional cycles, compatible regulation, and shared infrastructures would reduce operational risk and increase accessibility.

Championing digitisation. Blockchain solutions (real-time settlement, atomic swaps) have promise for reducing settlement times and increasing transparency if implemented with appropriate regulation.

Lessons from Crypto

- Liquidity illusions are dangerous. Exchanges, protocols, and investors alike must prepare for pro cyclical liquidity and design mechanisms to dampen forced liquidation spirals.

- Better risk management. Collateral frameworks, insurance pools, and coordinated circuit breakers are crucial to prevent structural fragility.

- Bridging to traditional markets. True institutional participation will only happen when regulatory frameworks are harmonized and operational risks are minimized.

Strategic Implications for Investors and Traders

Strategies should prioritise markets with deep, reliable liquidity, especially when active trading, short selling, and systematic risk management are essential. For product providers, this reinforces the US equity market’s appeal over riskier, less developed venues.

In thinner or emerging markets, position sizing and risk controls are paramount. Forcing capacity into a shallow market increases impact costs and compounds downside risk.

Periods of volatility create tactical opportunities for nimble, well-capitalized participants – if market plumbing provides the ability to get in and out reliably.

8. From Crisis to Opportunity

The liquidity crises of 2025, though disruptive and painful, are wake-up calls for market participants, regulators, and policymakers. They lay bare the dangers of ignoring structural weaknesses and the illusory promises of “volume” in the absence of foundational depth and trust.

Crypto’s unwind shows the speed and violence of liquidity flight in new, under-infrastructured markets. Asian equities demonstrate the costs of incomplete reform and ongoing fragmentation. The US market, for now, remains the gold standard for tradeable, reliable liquidity, short selling, and risk management.

For every trader, investor, and policymaker, the story of 2025 is a challenge: Fix the pipes, deepen the pools, remove the roadblocks – or risk watching value evaporate the next time confidence falters.