European Bonds Yield Review: Insights from Eastern Europe

We last reviewed European bonds yield trends, focusing on Eastern European Government Bonds, in January 2024. With the passage of time and shifts in the market, it is an opportune moment to reassess these assets.

Let’s begin with a historical overview of how selected European bonds yields have performed:

| Date | AAA | BBB- | BBB | BBB- | BBB |

| Germany 5 Yr | Greece 5 Yr | Bulgaria 5 Yr | Romania 5 Yr | Hungary 5 Yr | |

| Jan-23 | 2,30% | 3,44% | 3,96% | 5,46% | 4,55% |

| Jan-24 | 2,07% | 2,70% | 3,58% | 5,00% | 4,10% |

| Jan-25 | 2,31% | 2,64% | 3,50% | 5,10% | 3,50% |

At first glance, it would appear that prices have largely stagnated for the last 12 months. The German 5-year rate is marginally higher, by 0.24%, while most other countries like Greece, Hungary, and Bulgaria have 5-year rates lower.

Hungary’s 5-year rate is actually down a bit more than marginally—0.60%. Romania’s 5-year rate, however, is up by 0.10% since the last time we looked at the bonds one year ago.

Bulgarian Bonds: An Attractive Opportunity

As you can see, while Bulgaria and Hungary have similar credit ratings (BBB) and similar 5-year rates, those rates are much higher than the rates of Greece (BBB-). The reason for that “mispricing” is that Greece is a member of the Euro Area. With Bulgaria largely expected to become a member soon, it is reasonable to expect that Bulgarian Government Bonds could see the price rising and yields falling, along with credit upgrades from the credit agencies.

Unfortunately, we can not say the same for Hungarian debt. It is very clear that given the 5 rates of Greece and Hungary, Bulgarian bonds are cheap. It is not unreasonable to assume that if Bulgaria enters the Euro Area, 5-year rates could drop below 2.5% a year, as evidenced by the fact that Greek 5-year rates are at 2.64% and Greece has worse credit rating than that of Bulgaria.

Romanian Bonds: A Value Proposition Amid Challenges

Romanian Government Bonds continue to look like the best value in the region, just as with our previous reviews. While their yields appear to have “stagnated”, there has been quite a bit of action in those bonds. As recently as November 2025 yields in 5-yr Romanian bonds were much lower. However, recent political events like the cancelled December 2024 Presidential Elections are causing some nervousness amongst foreign investors.

What is really going on underneath the surface in Romania?

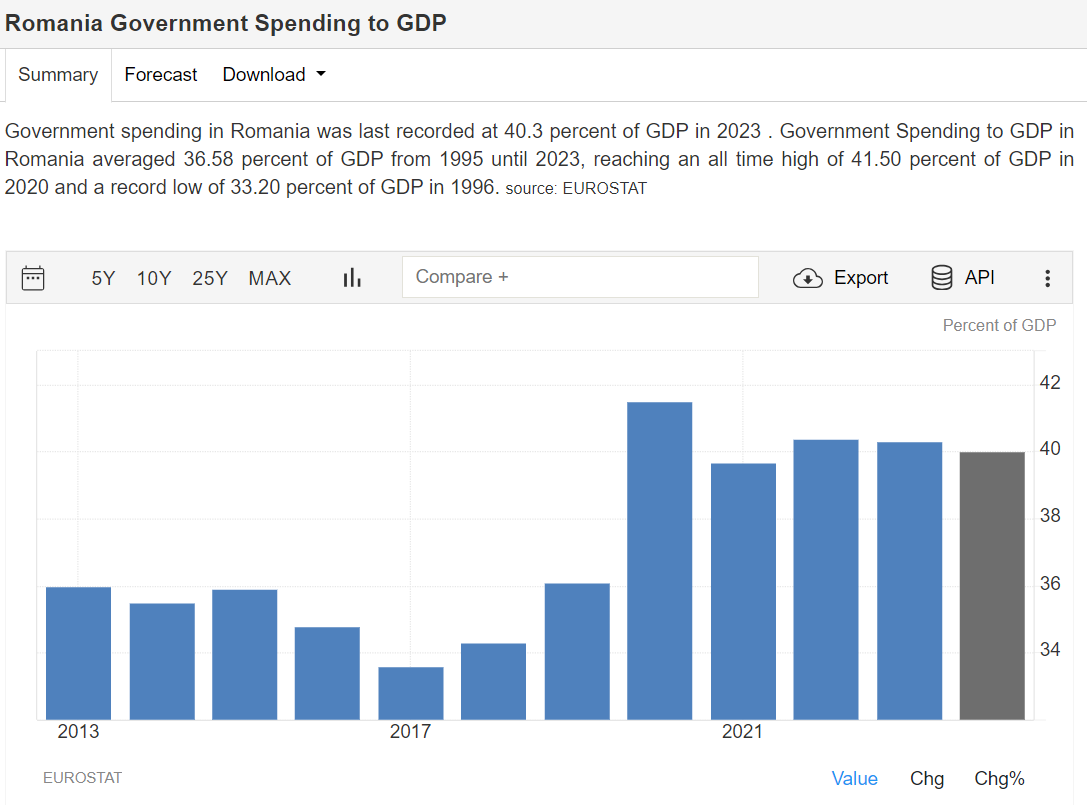

The problem is high government spending. It would appear that after COVID, the Romanian government started spending around 40% of the GDP, while historically, it has been 35%- 36% of the GDP. Unfortunately, the higher spending is not associated with increased investments but rather higher salaries for government workers and pensions for retirees—not exactly the recipe for success.

The government spending to GDP ratio is much higher in countries like Germany (around 48%), but German taxes are, on average, much higher than those in Romania. Romania’s government is spending way above what it is collecting. The extra external financing needs, around 8% of GDP in 2024, is what is keeping the yields high. Even that would not be a big problem if Romania was a member of the Euro Area. Still, unfortunately, it is not a member of the Area, and foreign investors demand extra return for their money.

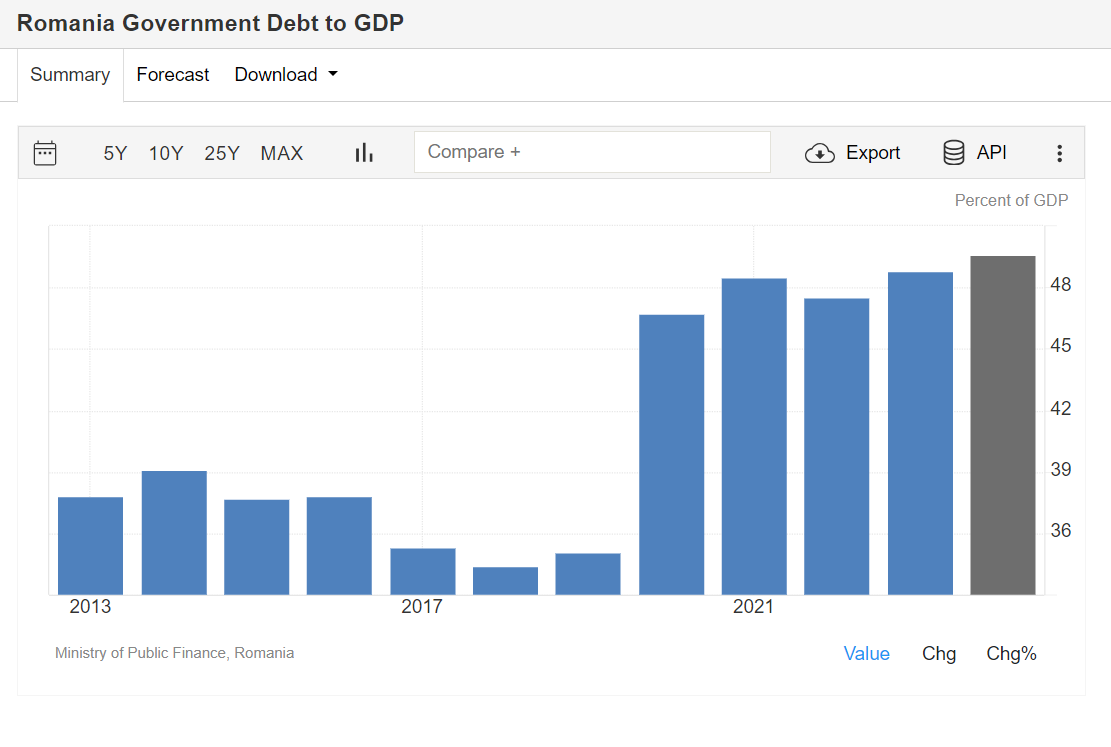

The Debt/GDP Perspective

On another hand, Romania is not Greece. While, indeed, the high percentage of government spending relative to GDP is a concern, the overall Debt/GDP is quite low:

In other words, while current financing needs are indeed worrisome, the overall level of Debt/GDP of around 50% is quite low compared to most other Euro Area countries. What is also helping the situation is that growth in Romania is expected to increase in 2025 and 2026. The Romanian economy grew by 1.4% in 2024. However, growth is expected to accelerate to 2.5% in 2025 and 2.9% in 2026. Thus, the external financing needed in 2025 and 2026 is expected to be noticeably lower.

Conclusion and Key Takeaways

The review of European bonds yield highlights both challenges and opportunities in Eastern Europe. Bulgaria’s bonds stand out as a strong opportunity, driven by its potential entry into the Euro Area, which could bring yields closer to Greece’s levels. Romania’s bonds, despite issues like high government spending, remain undervalued due to the country’s low Debt/GDP ratio and expected economic growth.

Both markets offer potential for investors, but staying informed on political and economic developments will be key to making the most of these opportunities.

Get the trading edge you need in today’s markets – sign up for our monthly newsletter featuring in-depth expert analysis, hot market insights, and exclusive trading strategies.