SWMR: The Nasdaq IPO That Broke the Math

Swarmer surged 1,000% in three days. The fundamentals didn’t move an inch.

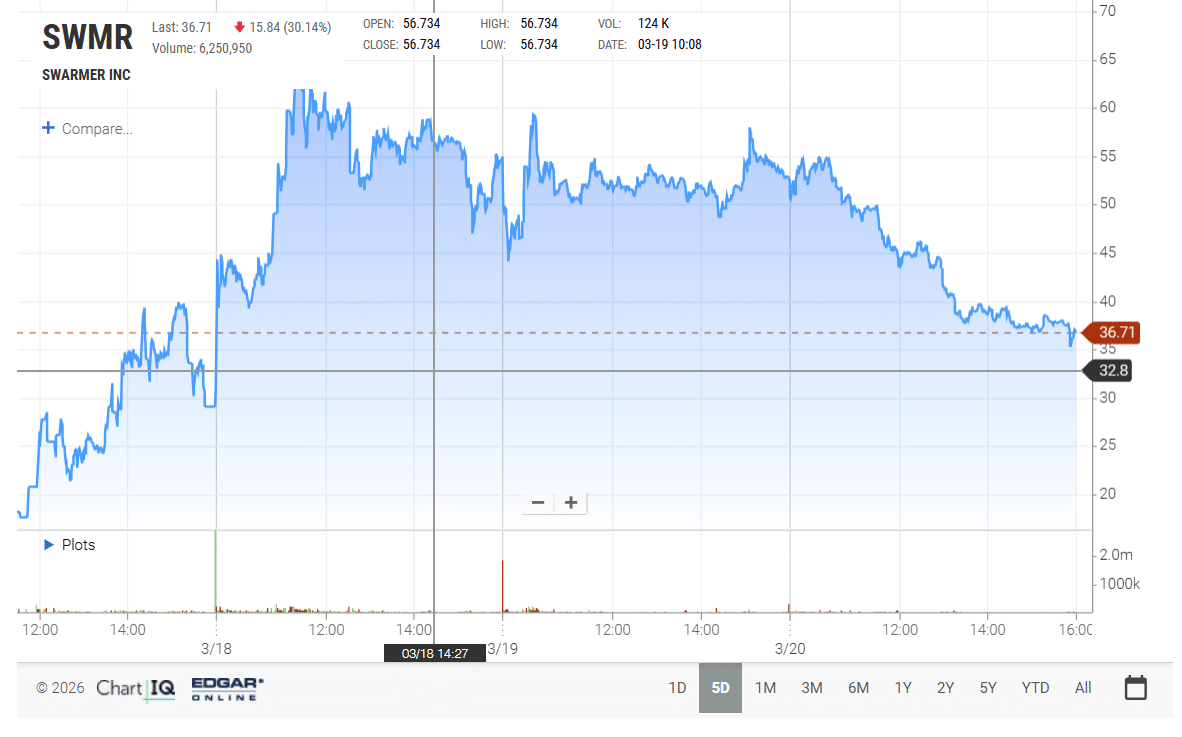

On March 17, 2026, Swarmer, Inc. (Nasdaq: SWMR) made its Nasdaq IPO debut at $5.00 per share. Four trading sessions later, the stock had touched $65.04, retraced to $36.71, and left the market asking a question no standard valuation model can answer cleanly: what just happened?

The short answer: a structural supply squeeze, a perfectly timed defense tech narrative, and retail momentum that had nowhere to go but up.

Why This Nasdaq IPO Caught the Market’s Attention

SWMR’s debut didn’t happen in a vacuum. Early 2026 brought a specific set of conditions that made this stock a lightning rod: expanding global defense budgets, the Iran conflict reshaping autonomous weapons procurement priorities, and sustained retail appetite for AI-driven narratives.

Bloomberg flagged the rally as the strongest U.S. Nasdaq IPO debut in nearly a year, second only to Newsmax’s 2,230% two-day surge in 2025.

When daily trading volume consistently exceeds the total float by 3–6x, conventional price discovery breaks down. What takes over is a momentum dynamic driven by order flow and sentiment — not earnings. In that environment, thematic positioning — AI, autonomous weapons, active conflict exposure — moves markets far more than any cash flow model.

What Swarmer Actually Does

Swarmer is an AI-driven software platform for autonomous drone swarm coordination. Its three core products :

- STYX AI Command and Control System

- MINAS Autonomy and Collaboration AI

- and TRIDENT Embedded Drone Operating System

are built to run large-scale uncrewed operations with minimal human input. As CEO, Alexander Fink put it at the debut: “One person can control 690 drones.”

Founded in May 2023 and headquartered in Austin, Texas, the company has logged over 100,000 combat missions in Ukraine since April 2024, operates across 42 military forces, and runs approximately 300 daily missions. In December 2025, Erik Prince — founder of Blackwater, currently Managing Partner of Frontier Resource Group — joined as non-executive chairman.

The IPO Structure: Why the Float Was the Story

The offering comprised 3,000,000 shares at a price of $5.00, with Lucid Capital Markets as the sole bookrunner. Underwriters exercised their full overallotment of 450,000 shares, bringing total shares sold to 3,450,000 and gross proceeds to $17.3 million. Net proceeds after fees: approximately $14.7 million, earmarked for operations, product expansion, hiring, and hardware integration.

Total shares outstanding post-IPO: approximately 12.3 million.

That left a free float of just 3.45 million shares — an exceptionally small number for a Nasdaq IPO of this profile. This single structural detail was the primary amplifier of everything that followed.

| Date | Open | High | Low | Close | Volume | vs. IPO |

|---|---|---|---|---|---|---|

| Mar 17 (Day 1) | $12.50 | $40.00 | $11.25 | $31.00 | 12.3M | +520% |

| Mar 18 (Day 2) | $40.00 | $65.04 | $38.55 | $55.00 | 22.1M | +1,000% |

| Mar 19 (Day 3) | $52.57 | $61.00 | $44.10 | $52.55 | 11.7M | +951% |

| Mar 20 (Day 4) | $49.92 | $55.00 | $35.11 | $36.71 | 6.1M | +634% |

Day 1 opened at a 150% premium before a single retail order was processed, closing at $31 after multiple exchange-triggered trading halts. Day 2 saw 22.1 million shares change hands — more than six times the entire float — pushing the stock to its $65.04 intraday peak.

By Friday, March 20, the first real reversal arrived. SWMR opened at $49.92, briefly touched $55, then dropped sharply to close at $36.71 — a 33% single-session decline. After-hours pushed it further to $36.28. Total retracement from peak: approximately 44%.

The Financials: What the S-1 Actually Says

| Metric | FY2025 | FY2024 |

|---|---|---|

| Revenue | $309,920 | $329,410 |

| Gross profit | $127,757 | $141,562 |

| Gross margin | 41% | 43% |

| Operating loss | $(5,116,107) | $(1,238,731) |

| Net loss | $(8,529,263) | $(2,069,642) |

Two things stand out immediately. Revenue declined year-over-year — from $329,410 in FY2024 to $309,920 in FY2025. And operating losses expanded sharply, driven by a fourfold increase in both SG&A ($2.67M) and R&D ($2.58M) — consistent with a company spending ahead of anticipated contract execution.

The forward pipeline tells a more interesting story: $16.3 million in firm contract commitments and $16.8 million in memoranda of understanding, for a total of $33.1 million in expected revenue. The company projects roughly $20 million of that to be recognized in 2026, with the balance in 2027 and early 2028 — subject to customer acceptance milestones and funding availability.

Valuation Disconnect

At peak, SWMR’s market cap reached approximately $680 million — roughly 2,000x current reported revenue. For context:

- High-growth SaaS: typically 10–20x revenue

- Defense primes (Northrop Grumman, Raytheon): 1–2x revenue

- Pure-play drone companies: well below triple-digit revenue multiples

The forward picture moderates this somewhat. If the company delivers approximately $20 million in 2026 revenue as projected, the peak multiple compresses to approximately 34x — aggressive, but within range for early-stage defense tech with proven combat deployment. The 41% gross margin, while on a small base, is structurally sound for a software business.

The risk that cuts the other way: dilution. Swarmer’s 2026 equity incentive plan reserves 5.4 million shares for stock-based compensation, with the pool eligible to grow by up to 5% annually. Against 12.3 million shares outstanding, that’s a meaningful overhang as vesting occurs.

Takeaway

Swarmer’s first week of trading illustrates a well-documented pattern: when a credible growth narrative meets a structurally constrained supply of shares, conventional valuation metrics temporarily cease to function as price anchors.

The Friday pullback is the first indication that supply-demand dynamics are beginning to normalize. Whether SWMR stabilizes at current levels or continues to correct will depend on two variables: the pace at which institutional investors establish positions at scale and the company’s ability to convert its $20 million revenue projection into reported results.

Until those data points arrive, SWMR remains a momentum instrument rather than a fundamental one — and should be evaluated accordingly. Clients considering exposure should be aware that current pricing reflects momentum dynamics rather than fundamental valuation, and that position sizing should align with that risk profile.

Data as of market close, March 20, 2026.

Sources: Nasdaq, Bloomberg, Yahoo Finance, SEC S-1 Filing — File No. 333-293123, Stocktwits