Service Now Stock: Fear Priced In, Growth Priced Out

The SaaSpocalypse That Never Came

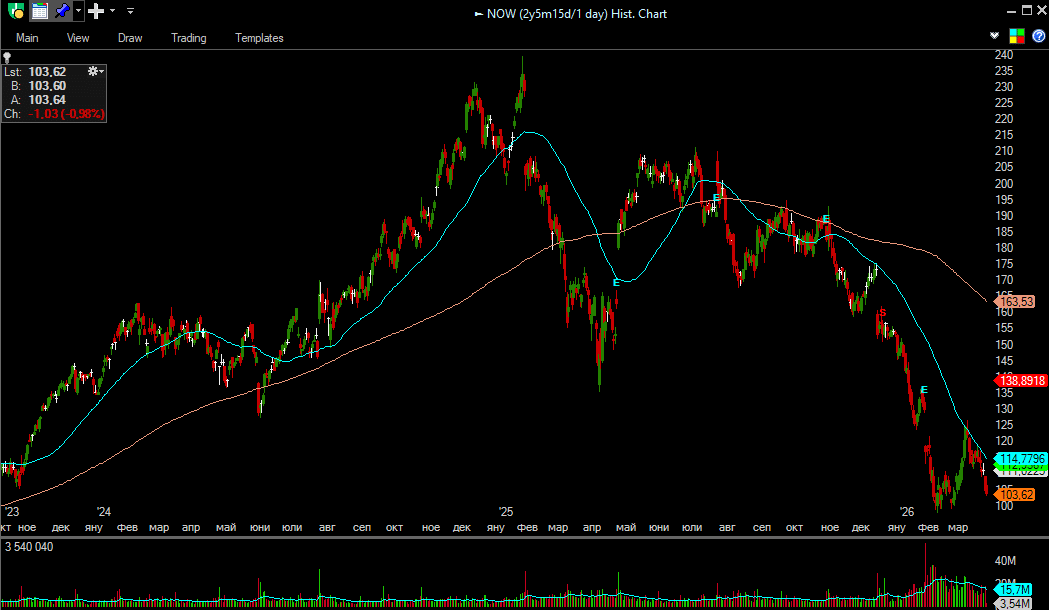

Service Now (NOW) has emerged as one of the most compelling opportunities in the software sector, as it recovers from its largest drawdown ever. The asset is currently trading over 55% below its all-time high – a casualty of the “SaaSpocalypse” narrative, which presumes that Generative AI will render legacy software obsolete. However, this fear ignores a critical architectural nuance: the difference between a replaceable interface and an essential database.

Chart – Historical Data Service Now Stock (NOW), Source: Hammer Pro Trading Platform

More Than Just Interface

Most investors treat Service Now stock as part of the vulnerable “Systems of Engagement” category. The fundamentals tell a different story. While it does provide an engagement interface, ServiceNow combines all three critical layers of enterprise software. Its real strength lies in being a legally and operationally entrenched “System of Record,” tightly integrated with a powerful “System of Intelligence and Automation.” It serves as the central nervous system for Enterprise IT. Its proprietary Configuration Management Database (CMDB) maps every part of an enterprise’s digital infrastructure.

This creates what we call the “Hallucination Barrier.” In high-stakes environments, accuracy is non-negotiable. No enterprise can afford an AI agent guessing a server’s dependency. A recent MIT study found that 95% of enterprise Generative AI deployments fail to generate ROI because they run on disconnected data silos. ServiceNow’s “Workflow Data Fabric” breaks down these silos so AI can learn continuously. When a server goes down, an isolated AI has no idea what the business impact is. Service Now knows the exact purpose, function, and dependency of every node in the infrastructure.

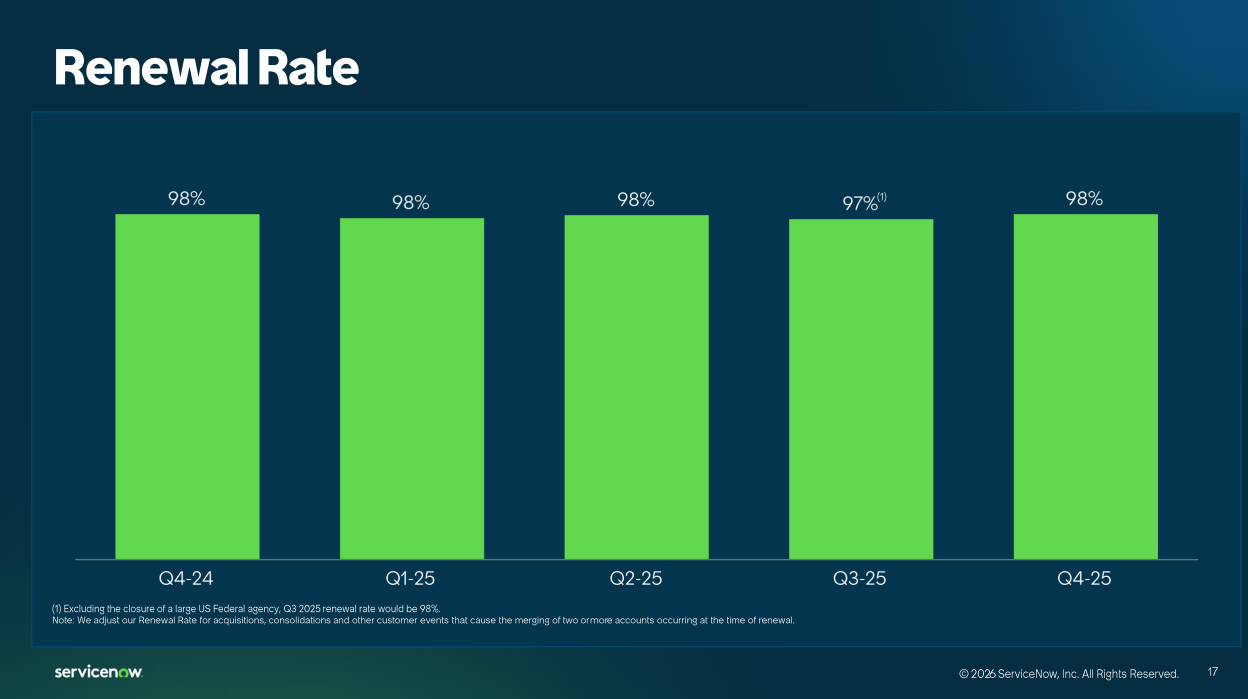

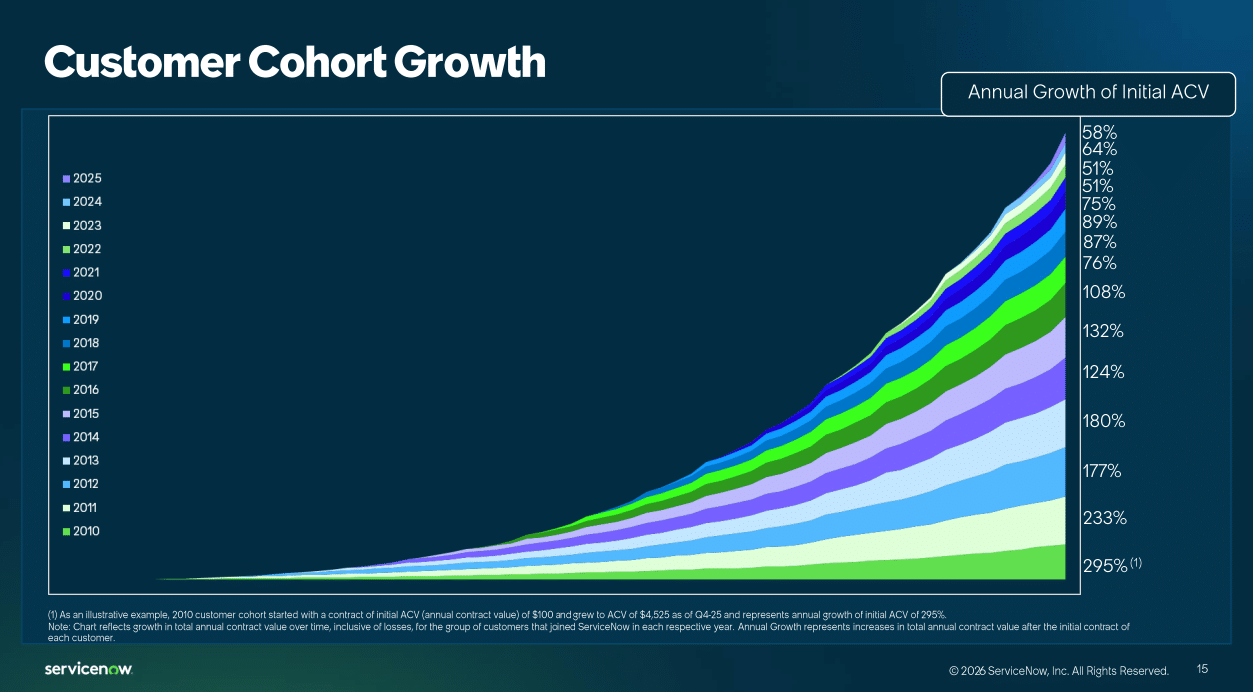

Customers Stay and Spend More

Source: ServiceNow 4Q25 Investor Presentation

Retention rates confirm this entrenchment. The company holds renewal rates above 97%, proving that customers are not leaving despite the AI hype — they are expanding. The cohort that joined in 2010 has grown its initial contract value by 295%.

Source: ServiceNow 4Q25 Investor Presentation

Furthermore, the company now boasts 603 enterprise customers spending over $5 million annually, with an average contract of $14.7 million. ServiceNow is no longer just an “IT helpdesk.” A staggering 53% of its Net New Annual Contract Value (ACV) now comes from outside IT, driven by HR, Customer Service, and Creator workflows.

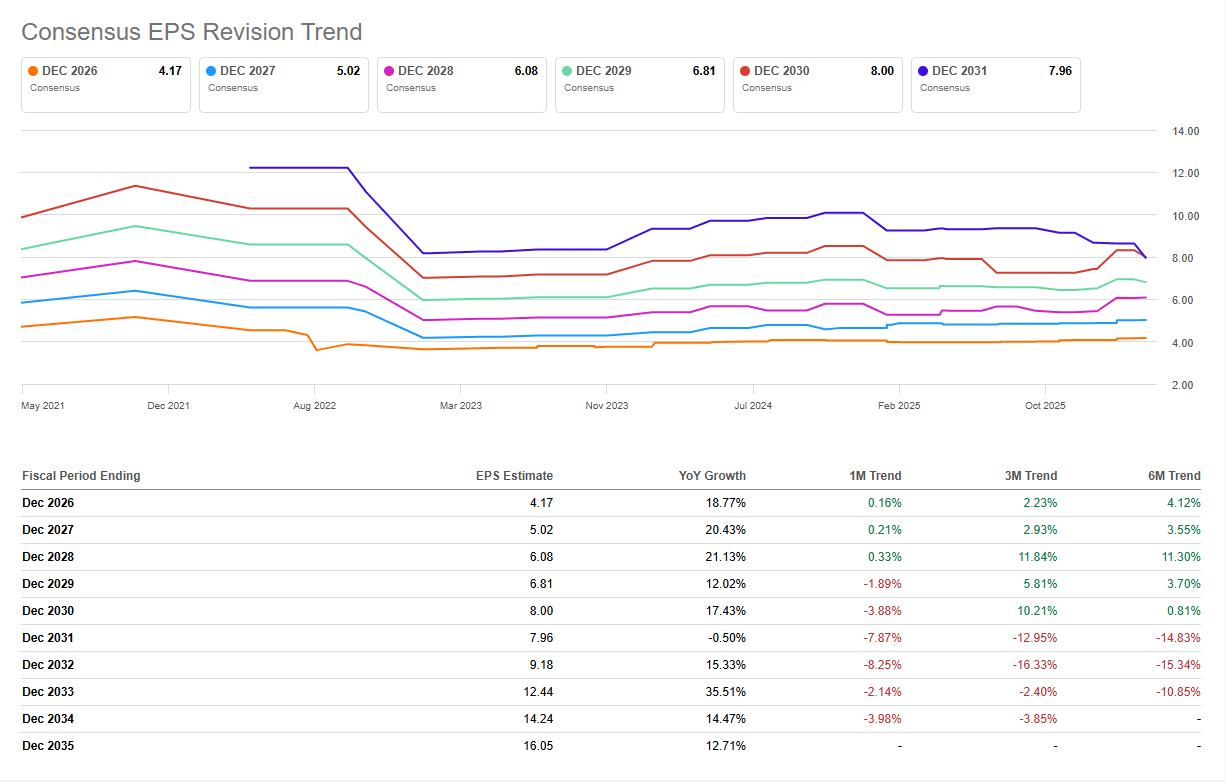

Growth Is Accelerating, Not Fading

The disconnect between the narrative and the fundamental reality is clearly visible in the consensus EPS data, which directly refutes the “secular decay” thesis priced into the stock. Instead of fading, growth is ramping up.

Source: Seeking Alpha

Service Now is projected to accelerate from 18.77% growth in 2026 to over 21% by 2028. We are effectively seeing a “growth anomaly” where the market anticipates existential displacement, but the analysts project a fundamental re-acceleration.

If genuine obsolescence were imminent, short-side activity and institutional ownership would reflect it. Instead, we don’t see any strong bearish conviction from market participants. Short interest currently sits at just 2.69%, according to Finviz.

For an asset that has shed half its market value, these levels are immaterial. In a terminal decline scenario, the short book would typically swell into the double digits – often exceeding 10% would be concerning. The fact that short interest remains pinned near 2% indicates that the recent drawdown was driven by broader portfolio derisking, not a targeted attack on the fundamentals. Large asset managers are simply trimming their exposure, as evidenced by the massive institutional ownership base (87%+) that remains firmly intact.

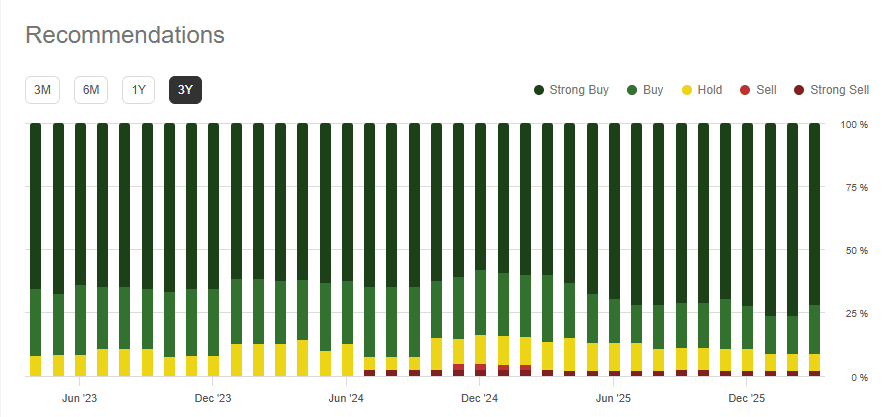

This institutional confidence is mirrored by Wall Street analysts, who have consistently maintained over 70-75% “Buy” and “Strong Buy” ratings over the last three years, even through the absolute peak of the AI panic.

Source: Seeking Alpha

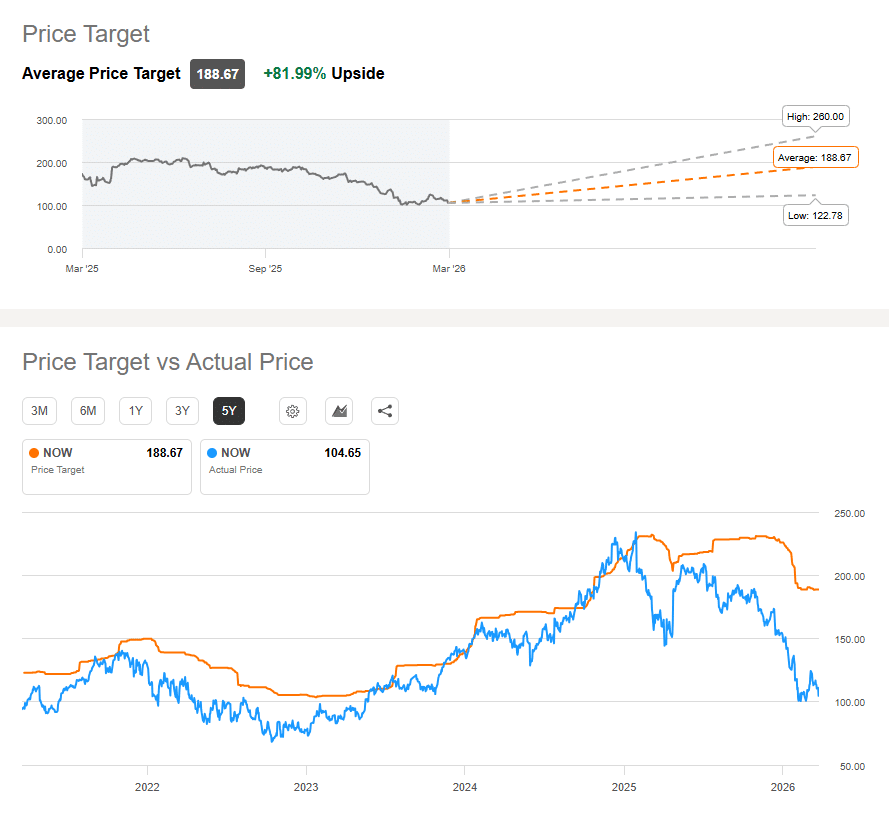

The Numbers Behind the Thesis

Because Service Now is a mega-cap stock trading at roughly a $130 billion valuation, its aggressive growth projections aren’t just hopeful guesses – they are heavily scrutinized and vetted by Wall Street. Looking at their targets, the absolute lowest, most pessimistic estimate on the Street is $122.

Source: Seeking Alpha

Meanwhile, the average target is $188, implying an enormous 82% upside. Management clearly agrees, having just authorized a massive $5 billion share repurchase program. This buyback is backed by an absolute fortress balance sheet boasting nearly $4.8 billion in net cash and incredibly low-interest debt – a tiny 1.4% fixed-rate note that isn’t due until 2030.

Positioned to Run the AI Layer

AI will not destroy Service Now Stock. It will need Service Now. CEO Bill McDermott projects 2.2 billion AI agents in operation by 2030. Millions will run natively on the platform. The rest will need Service Now to govern, secure, and route them through its “AI control tower.”

The market worries that AI will eliminate human workers and kill per-seat subscription revenue. ServiceNow is already ahead of this shift, moving toward outcome-based and consumption-based pricing. Every task an autonomous agent runs requires a query to the underlying system of record. That drives higher transaction volumes back to the core database. The company monetizes machine activity, not just human headcount.

Investors now have a rare chance to buy critical infrastructure at a distressed price, just as the growth engine shifts into a higher gear.