The Fed Funds Rate Increase History and Inflation

What Markets Knew That the Fed Didn’t

The Federal Reserve controls the most powerful tool in the economy: interest rates. The Fed Funds Rate increase history is an important lesson in how monetary policy shapes inflation and economic trends. But what if the markets knew better? What if the Fed has been consistently late—late to fight inflation and late to stop? This is not just speculation; history proves it.

Each rate hike and policy decision has shaped inflation trends, often with unintended consequences. By analyzing past rate hikes, we can see how the Federal Reserve’s actions align—or fail to align—with market signals.

To understand this, we will analyze past Fed rate hikes and their impact on inflation. Two key graphs will guide our discussion.

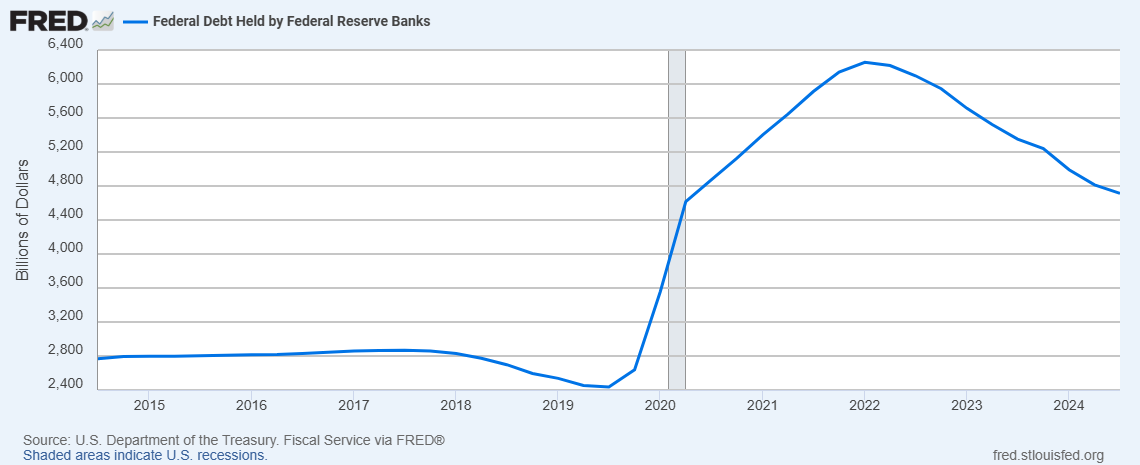

The first graph presents the Federal Reserve Balance Sheet, data courtesy of the St. Louis Fed.

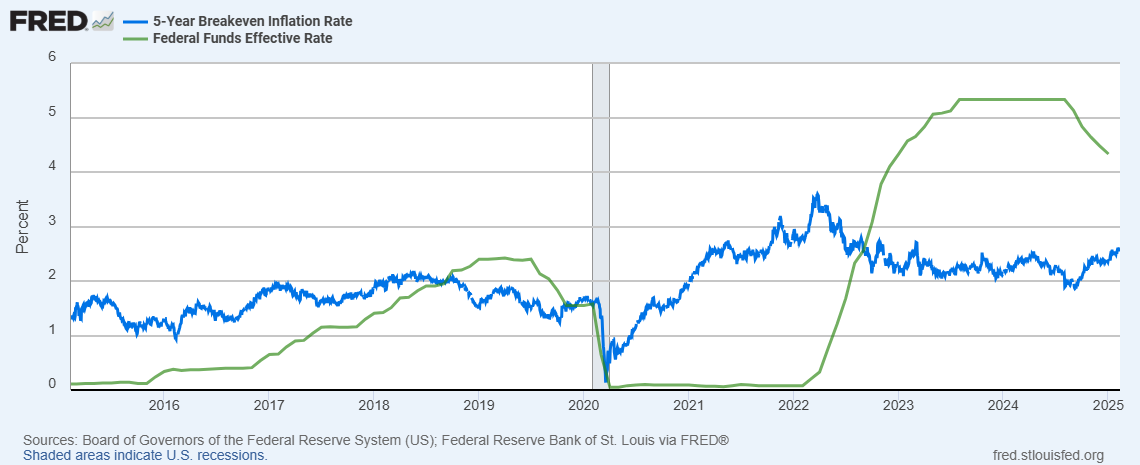

The second graph, also courtesy of the St. Louis Fed, includes two series: the Fed Funds Rate and the 5-year Breakeven Rate.

Graph 1: The Fed’s Balance Sheet and Its Impact on Inflation

The significance of the first graph is best explained by Prof. Milton Friedman’s words: “Inflation is always and everywhere a monetary phenomenon.” In other words, sustained inflation begins with the central bank’s balance sheet. While strong labor markets, tariffs, or tax increases can create temporary inflationary pressures, long-term inflation is only possible if the central bank expands its balance sheet.

This is not just Prof. Friedman’s opinion—it is widely accepted among economists, as evidenced by his Nobel Prize in Economics for this work.

Now, let’s turn our attention to the Fed Funds Rate increase history.

Graph 2: Fed Funds Rate and 5-Year Breakeven Rate – What History Tells Us

Markets consistently interpret information better than any individual or group, including the Fed. This is why the 5-year breakeven rate, derived from 5-year TIPS (Treasury Inflation-Protected Securities), is a reliable forward-looking measure of inflation. Reviewing historical trends, we can assess how well the Federal Reserve’s rate hikes aligned with inflation expectations.

Rate Hikes from Q3 2016 to Q3 2017

During this period, the Fed Balance Sheet increased by 2%, and the Federal Reserve was concerned about rising inflation. As a result:

- The Fed Funds Rate was raised from 0.35% to 1.70%.

- The 5-year Breakeven Inflation Rate rose from 1.3% to 1.70%.

After this, the Fed stopped increasing its balance sheet. According to Modern Monetary Theory, monetary policy changes have an average lag of nine months. As expected, inflation expectations continued rising, reaching 2.1% by Q2 2018. However, the Federal Reserve continued hiking rates, reaching 2.5% by December 2018. In hindsight, this last increase was likely unnecessary, given that inflation expectations had already begun to decline. The Fed would have been wise to stop at 2.0% or 2.25%, as indicated by TIPS market signals.

Rate Decisions from Q4 2019 to Q2 2021

During this period, the Fed’s balance sheet more than doubled, surging from $2.6 trillion to $5.6 trillion. This led to:

- A sharp increase in 5-year Breakeven Inflation Rates, rising from 1.7% to 2.6%, well above the 2% inflation target.

- The Fed Funds Rate remained at 0.25%, despite clear inflation signals.

In April 2021, Fed Chair Powell described inflation as “transitory”—a statement that did not age well. The Federal Reserve’s reluctance to tighten monetary policy earlier allowed inflation to rise further. Not only did the Fed fail to react, but it continued expanding the balance sheet by another 10% in the latter half of 2021. In hindsight, this was an avoidable mistake.

The Present and Future Rate Path

Currently, the Fed Funds Rate stands significantly higher than both annual inflation and 5-year inflation expectations. Since the Fed is not expanding its balance sheet, sustained inflation is unlikely. Short-term factors like tariff wars and strong labor markets may create temporary inflation spikes, but they do not justify maintaining excessively high rates for long.

In our opinion, the Federal Reserve would be wise to continue its gradual course of lowering rates in 2025 and possibly 2026, as inflation is unlikely to surge.

Conclusion: Key Lessons from the Fed’s Rate Increase History

Systemic risks could be greatly reduced if central banks worldwide gave more weight to market-derived inflation estimates in their decision-making processes. Most major economies—including the U.S., France, Germany, and India—now have Treasury Inflation-Protected Securities, which provide valuable forward-looking data.

The key lesson from the Fed Funds Rate increase history is that the Federal Reserve tends to be late—late to start fighting inflation and late to stop. A more proactive approach, guided by market indicators, could improve monetary policy outcomes and avoid unnecessary economic disruptions.