PDD Stock: Hidden Gem or a Value Trap

Insights on Temu’s Parent Company, PDD Holdings

PDD stock, which represents the Chinese online retailer Pinduoduo, experienced a significant drop of over 30% after the company reported its earnings in the last week of August. According to Wikipedia, PDD focuses on the traditional agriculture industry and is the largest product of PDD Holdings, which also owns the online marketplace Temu. Although PDD beat earnings estimates, it missed revenue estimates by 4%, contributing to the sharp decline in its stock price.

That attracted our attention. If you have seen or used their services in Temu, you would know that the site actually has attractive and, most importantly, cheap offerings. Could this be the next Amazon?

PDD Stock Valuation: Analyzing Financial Metrics

Digging further into the accounting value of the company, courtesy of Finviz.com, we found this about the company’s valuation:

There is a lot of data here, but we will focus only on a few numbers. First, sales growth over the last five years – 80% annually! Second, a net profit margin of 29%, and finally, a forward PE ratio of 6.56!

Not only is the valuation incredibly cheap given its historical performance, but if stock analysts are to believe, their next 5-year earnings growth will be about 44% annually. Moreover, this is not some small or unfollowed company; PDD has a market capitalization of 133 Billion USD.

Looking at their balance sheet, we also found that the company has a book value of 25 USD/share and cash of nearly 35 USD/share. Yes, it seems like this company is incredibly cheap. Yes, Chinese companies are not in favor right now, but even BABA, a company that faces flat earnings growth, according to stock analysts, is trading at a multiple 2 times higher than this. Not only that, but BABA is utilizing its cash, nearly 15% of its market value, to purchase its stock at a pace of nearly 3% of shares outstanding quarterly or slightly above the 10% annual rate.

PDD Stock: Concerns and Future Outlook

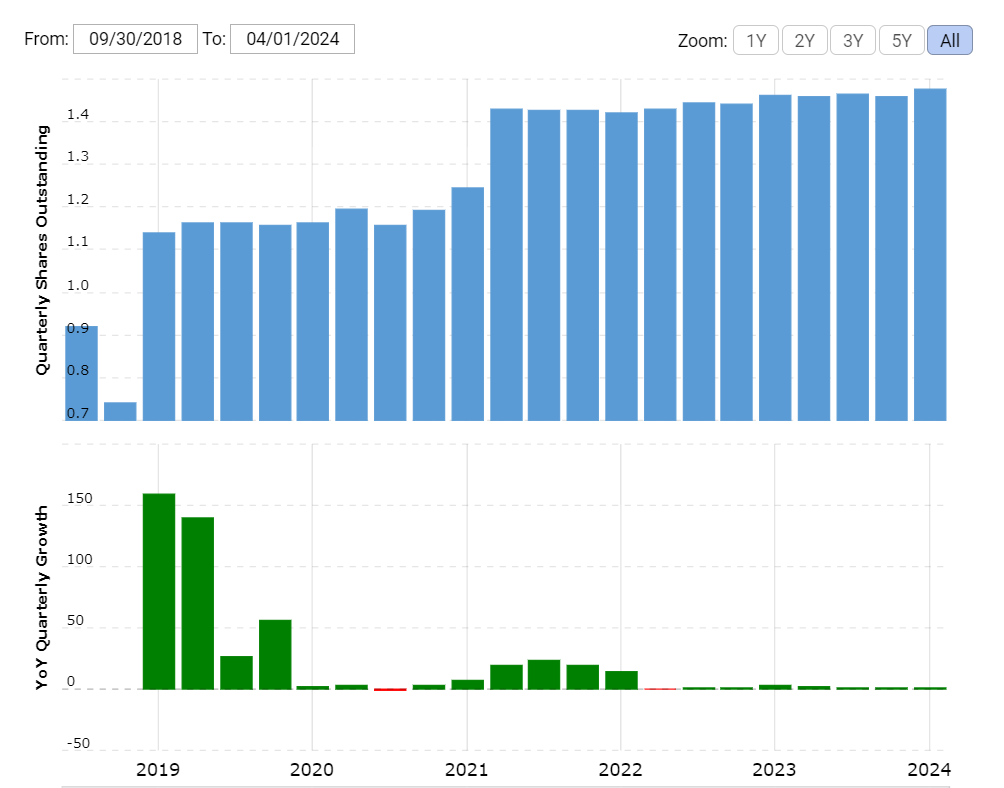

When examining PDD’s current approach to its financial strategy, a crucial question arises: What is PDD doing on the front of share buybacks and capital allocation?

Pictured above, PDD shares outstanding. Courtesy of macrotrends.com.

The answer is obvious – nothing.

Having lived through several high-profile corporate frauds, such as Enron (2001), WorldCom (2002), and Parmalat (2003), we are very uncomfortable that PDD is not doing the obvious thing—buying back its shares.

We are not necessarily saying that PDD is fraud—not at all—just that it is our experience that companies with so much cash on their balance sheet and a low valuation usually start buying back their shares.

Investing is a business where the concept of margin of safety is very important. The forward price distribution for PDD is, in our opinion, too broad. This stock could go up 100%, 200%, or even 500% in the next few years if the future for PDD looks what stock analysts expect it to. However, it is also possible that PDD’s prospects are also not so rosy.

Is it possible that future sales growth will be much smaller? Is it possible that PDD’s earnings growth comes significantly short of analysts’ expectations? We do not know. And when we do not know, we stay away.

One factor that could cause us to change our minds is if PDD starts buying a meaningful percentage of its float. What could that meaningful percentage be? Is it similar to what BABA is doing, or about 3-5% quarterly?

Anyway, they seem to have the cash available. If the company does not see value in buying back its shares at current valuations, there may be no value.

Key Takeaway

PDD stock presents a complex investment scenario. Despite its low valuation and attractive financial metrics, including high sales growth and significant cash reserves, the lack of share buybacks and the broad uncertainty around its future growth make it a risky proposition.

The company’s current approach to capital allocation raises concerns, especially given historical cases of corporate missteps. Investors should carefully consider these red flags and assess whether the company’s actions align with its valuation before making investment decisions.