Investing in NVIDIA: Is Now the Right Time?

As investors weigh the future of the AI industry, investing in NVIDIA has come under scrutiny following Deep Seek’s disruptive entry with its affordable and capable AI, DeepSeek-R1. This unexpected development rattled NVIDIA’s stock, sparking debates about its long-term position. With the company’s earnings report set for February 26, 2025, now is a good moment to take a look at it.

Why Wait Two Weeks to Weigh In?

We prefer to wait at least two weeks before analyzing major stock events. This waiting period allows stock analysts to process new developments and issue updates. As a group, stock analysts are often the most informed experts on a company’s prospects.

Additionally, short-interest data, a reliable indicator of investor sentiment on potential downside risks, takes time to be updated. According to finviz.com, short-interest information is refreshed twice a month. We waited for the latest update from the end of January 2025 to get the most accurate picture.

Analyst Ratings: What the Experts Are Saying

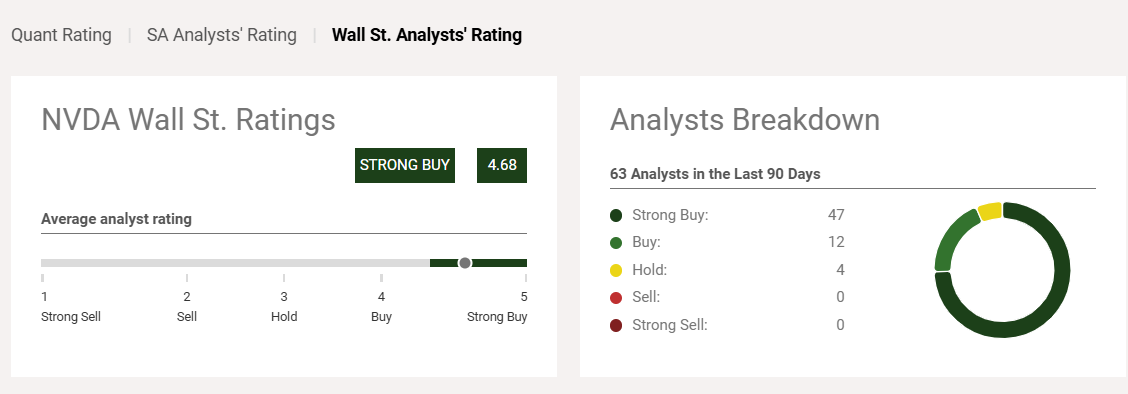

Without further ado, let’s dive into analyst ratings sourced from seekingalpha.com:

In the last 90 days, 63 stock analysts have issued updates on NVDA. The stock has been and continues to be loved by stock analysts—over 93% of all NVDA ratings are Buy or Strong Buy. Only 7% have a Hold, and there are no Sell recommendations. This is as good as it gets in terms of ratings.

Price Targets: Is NVIDIA Still Undervalued?

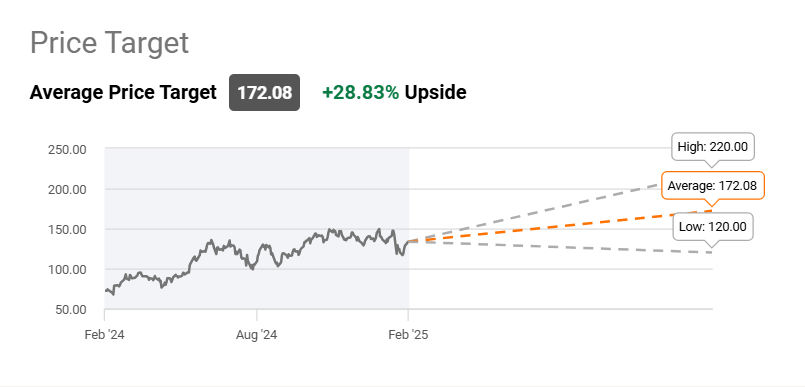

Again, using Seeking Alpha data:

Relative to the average price target of the stock, NVIDIA has about a 30% upside from current levels. The lowest price target is about 8% lower relative to current levels. Using this metric (average and lowest price target), NVDA is one of the cheapest stocks among the US Top 100 companies. Yes, the stock has climbed about 10% since its lows, but it is still undervalued.

Short Interest and Institutional Ownership

According to finviz.com, Short Interest is at a very benign 1.22% float – in line with such statistics for most large companies. However, institutional and insider ownership rates are at an average of 69%. We have covered NVDA before, and this rate has been relatively stable – yes, institutions are not in love with NVDA. This is a very worrisome fact. NVDA’s business model is vulnerable due to technical innovations, which are primarily unpredictable. We are not sure if Deep Seek will be responsible for the death of NVDA, but the threat from competitors is real and can materialize at any time.

However, since stock analysts continue to be very positive on NVDA, two weeks after the news on Deep Seek hit the newswires, we have to accept their opinions just like we take the opinions of our doctors, accountants, and mechanics. While new competitors will always threaten NVDA, according to most stock analysts, Deep Seek is not the NVDA killer, and the stock could have a significant upside – as much as 50% from current prices!

NVIDIA’s Valuation: Comparing Key Metrics

NVDA’s forward PE ratio is 26.22 versus 24.01 for the S&P500 and 29.53 for the S&P500 Technology Index. 2025 earnings growth is expected to be 50% for NVDA, 13.3% for S&P500, and 17.4% for S&P500 Technology Index. Yes, NVDA is incredibly cheap! Estimates for NVDA for 2026 are also not so elevated – only about 25% earnings growth. However, estimates beyond 2026 are quite a few – indicating uncertainty amongst stock analysts who are probably waiting for guidance at the earnings call.

Conclusion: Is the DeepSeek Threat Overblown?

The threat to NVIDIA’s business model from Deep Seek appears to be exaggerated. While competition is always a risk, it is too early to determine if NVDA will face significant disruption soon. Analyst sentiment and valuation metrics suggest that investing in NVIDIA remains a strong opportunity among large-cap US stocks.

Earnings Insights: What History Tells Us About NVDA

NVDA has beaten earnings 18 out of the last 20 times. The average beat was around 10%, and the average miss was around 13%. While not exactly comforting, those statistics are not discomforting enough for us to avoid taking a long position before the earnings date. There are risks to doing so, but we think the risk/reward ratio is worth it.