Trade War Escalation: Is it Time for Treasuries

Spotlight: IEF and TLT treasury ETFs

Key Points

-

The U.S.–China trade war escalation has ended months of market calm, triggering renewed volatility across global equities.

-

Analysts see limited upside for stocks after strong gains this year, with potential 8–10% downside from recent S&P 500 peaks.

-

As the Federal Reserve cuts rates and yields fall, Treasury ETFs like IEF and TLT are emerging as preferred defensive plays.

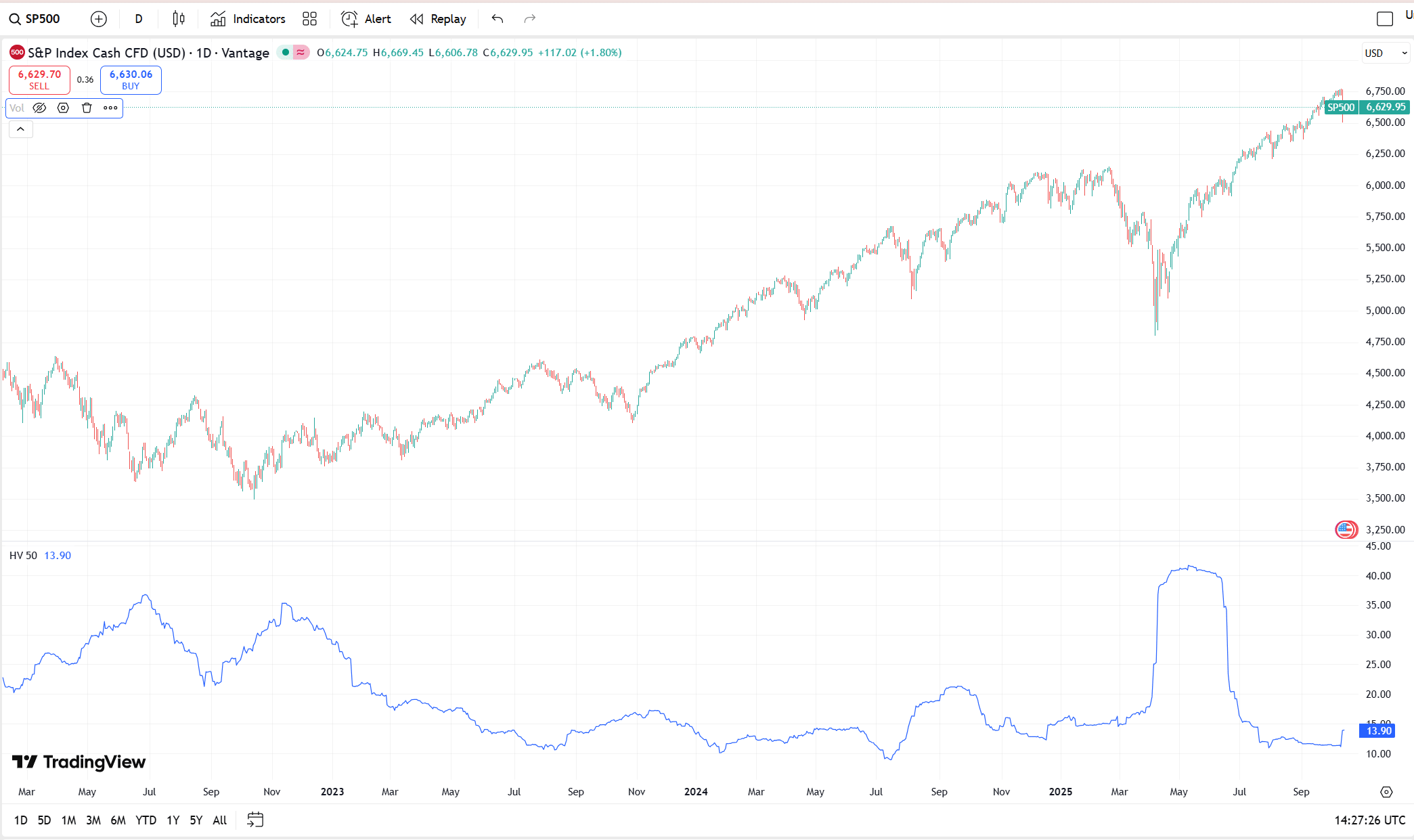

Ever since the market correction in the spring, equity markets have delivered enviable returns. Up until last week, the S&P 500 was up more than 30%, and the NASDAQ-100 nearly 50% from their respective lows in early April. While those gains are impressive, what makes them unusual is that they occurred amid exceptionally low realized volatility — a rare calm for such a strong rebound.

The S&P 500 50-day rolling historical volatility has remained near multi-year lows, reflecting tranquil markets throughout the summer. That calm, however, has been shattered by an escalation of the trade war between the United States and China, a new and serious threat that roiled global markets last week.

Source: TradingView – S&P 500 50-day rolling historical volatility

A New Source of Market Stress: The Trade War Escalation

This renewed escalation of the trade war has introduced multiple risks. The first is the threat of additional 100% tariffs on Chinese imports — a move few investors had expected. Second, the short-term ability to replace Chinese imports is limited. Even if substitution were possible, the timing is poor, with the holiday season fast approaching. U.S. retailers and manufacturers will find it difficult to adjust quickly, creating new pressures on margins and supply chains.

In our view, resolving this new round of trade tensions will likely take months, not weeks. A realistic timeline is 4 to 6 weeks, assuming constructive negotiations.

Given the strong year-to-date equity performance, institutional investors may hesitate to increase exposure here. Some may even reduce equity allocations to lock in profits. We don’t expect markets to climb to new highs in the near term. Instead, we see a potential 8%–10% downside from the S&P 500’s recent peak of 6750, a reasonable estimate given the market’s reaction to prior tariff announcements.

Positioning for the Next Phase: Bonds Over Shorts

Contrary to what many expect, even when we anticipate a correction, we don’t necessarily short the market — not when there are better alternatives. Our preferred approach is to build long positions in U.S. Treasury ETFs, which typically benefit from risk-off moves.

The vehicles of choice depend on an investor’s risk tolerance, but we focus on a mix of:

-

IEI – iShares 3–7 Year Treasury Bond ETF

-

IEF – iShares 7–10 Year Treasury Bond ETF

-

TLT – iShares 20+ Year Treasury Bond ETF

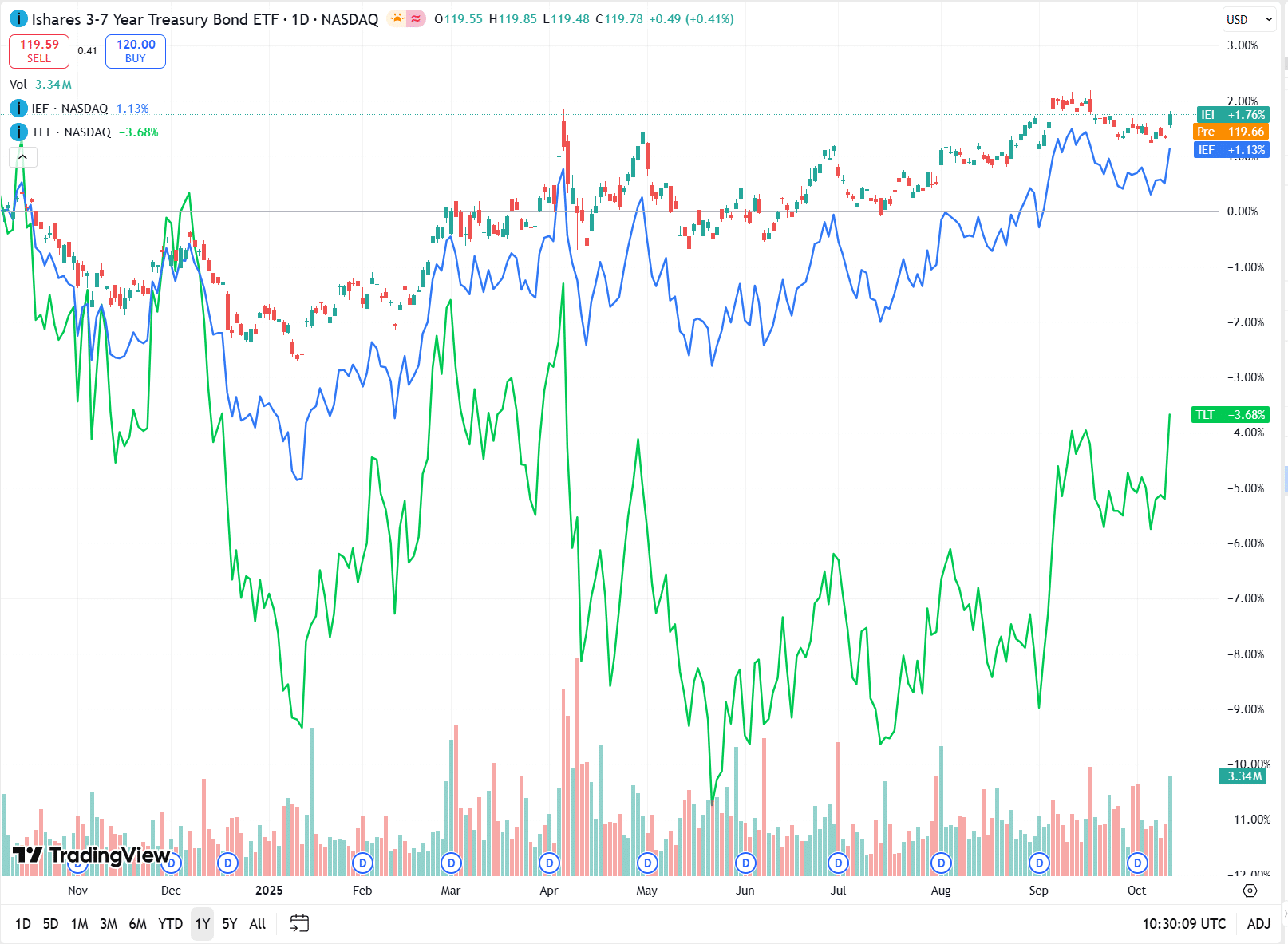

Let’s take a look at the performance of the ETFs mentioned above for a period of one year, courtesy of tradingview.com:

Over the past year, long-dated Treasury ETFs have underperformed shorter-duration ones by a wide margin. Even so, we’re concentrating on a balanced allocation between IEF and TLT, which we believe offers favorable asymmetry if yields decline further.

The Fed’s Policy Shift and Real Rates

The Federal Reserve has already embarked on the second leg of its long-delayed rate-cutting cycle. Market expectations suggest the Fed Funds rate could fall to around 3% by the end of 2026, well below the current 4.09%.

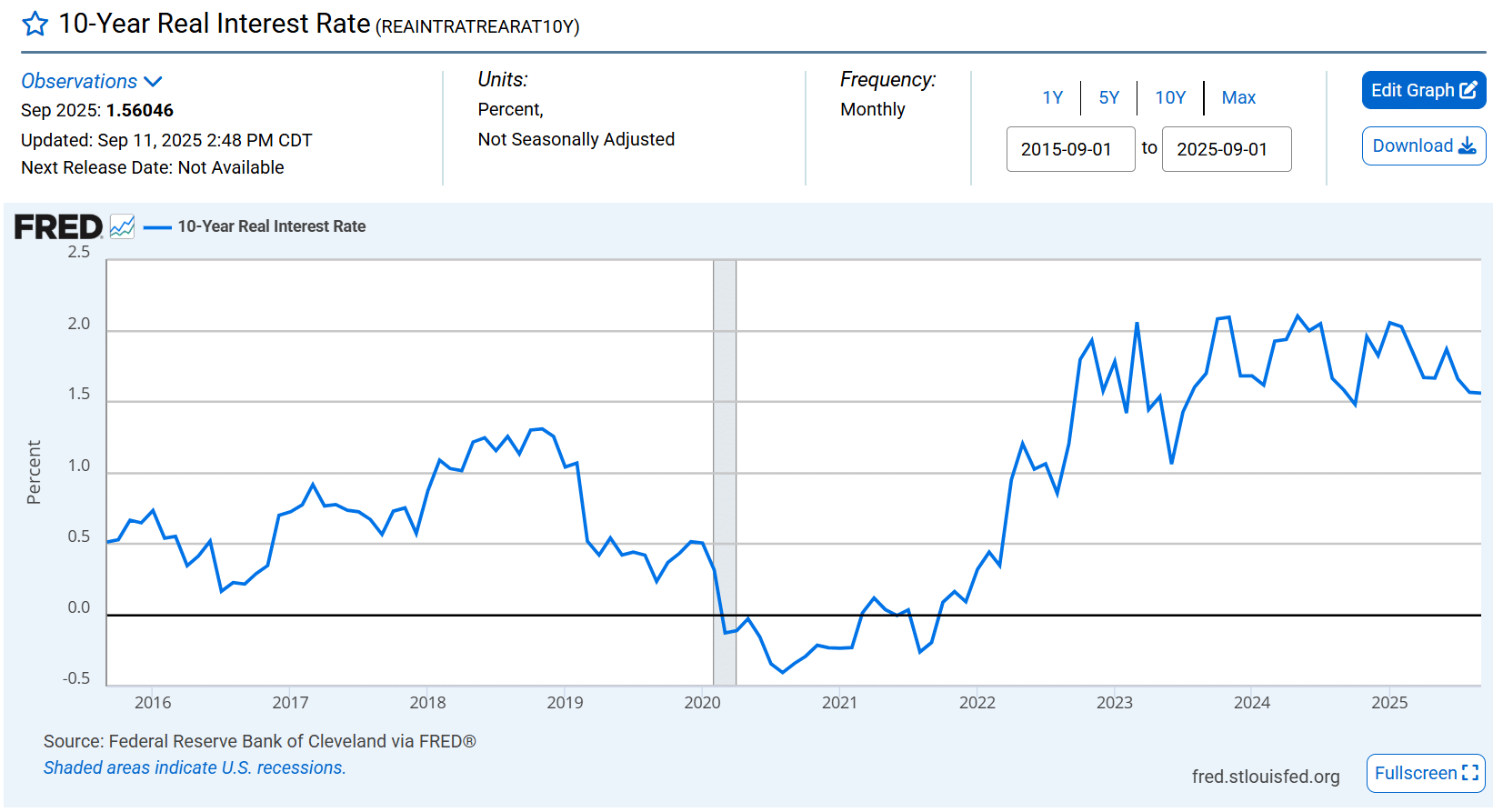

Meanwhile, the 10-Year Real Interest Rate remains high relative to its 10-year average — an anomaly likely to normalize. Now that inflation appears contained, we expect this premium to compress to around 1%, implying a potential 0.5%–0.6% drop in the 10-year yield from 4.05% to roughly 3.55%.

Even if this adjustment takes time, the current real rate looks excessive. Should a market correction coincide with this process, yields could compress sharply — possibly to 3.6%–3.7%. Based on duration sensitivity, such a move could translate into price gains of roughly 8%–12% in TLT and 4%–6% in IEF. These projections are estimates, not guarantees, but they illustrate the potential upside in quality fixed income during periods of stress.

Labor Market Weakness and the Inflation Outlook

Another crucial factor is the weakening labor market observed in recent months. Even if inflation were to reappear temporarily, the Fed is unlikely to reverse course. Interest rates remain well above inflation levels, and the softening labor market signals deflationary pressures may be taking hold.

That dynamic supports lower yields and stronger bond performance, particularly if equity markets react negatively to ongoing trade war escalation and global growth concerns.

Bottom Line

The trade war escalation has reintroduced volatility to a market that had grown complacent. With equity valuations stretched and policy uncertainty rising, the risk-reward balance increasingly favors Treasury ETFs over additional equity exposure.

In our view, defensive positioning through IEF and TLT provides an effective way to benefit from potential yield compression while reducing overall portfolio risk, especially if the trade war escalation persists and a broader market correction unfolds.