Trump Tariffs Are Fueling Fear, Not Inflation

We’ve already explained how Trump tariffs function as a tax on imports—now it’s time to look at their broader impact. Although Trump introduced these tariffs to boost domestic production and cut the U.S. trade deficit, those goals take time to achieve.

In the meantime, Trump’s tariffs are already squeezing U.S. consumers by driving up the cost of imported goods and eroding purchasing power. Even more concerning, they’ve triggered a sharp drop in consumer confidence—a critical signal of where the economy may be headed next.

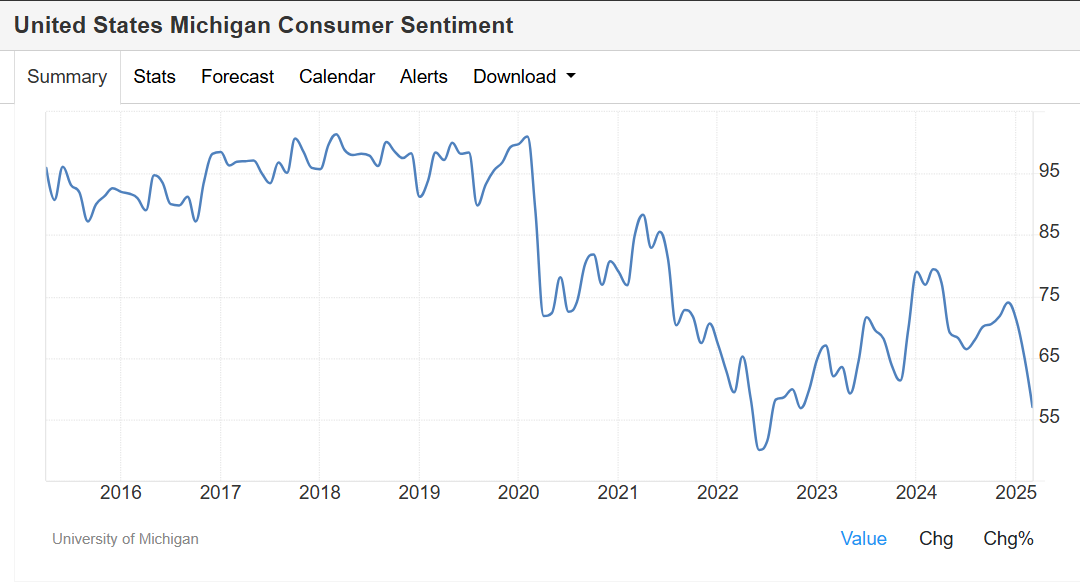

Consumer Confidence Takes a Hit

According to Trading Economics, U.S. consumer sentiment has declined over the past six months, falling from nearly 75 to a 10-year low of 57. This steep drop doesn’t bode well for future economic activity or the employment market.

Certainly, import prices may rise, but we see strong evidence that demand destruction will occur; imports, while important, account for only a fraction of the US GDP. The value of all imports in 2024 was slightly over $ 4 trillion, while the US GDP for the period was nearly $ 30 trillion. Yes, we might see some inflation in the month(s) following the tariff imposition, but that would be a temporary blip. Demand destruction will be more certain and likely permanent.

Let’s view another chart, courtesy of tradingeconomics.com again:

Pictured in green is the 1-year US rate, and pictured in blue is the 10-year US rate. As we can see from the 25-year chart, there is clear cyclical behavior in both one-year and 10-year rates. That cyclicality is significantly stronger for the 1-year rates – when 1-year rates start rising, they tend to continue growing.

When one-year rates start falling, they continue to decline. The dynamics nowadays, at least to us, appear to be very close to those of 2007-2008. 1-year rates have decreased significantly and are now under the 10-year rates.

Given the imposition of Trump tariffs and a sharp decline in consumer confidence, we believe there’s very little chance of sustained future inflation. As a result, we expect 10-year U.S. Treasury yields to move lower from their current level of 4.2%.

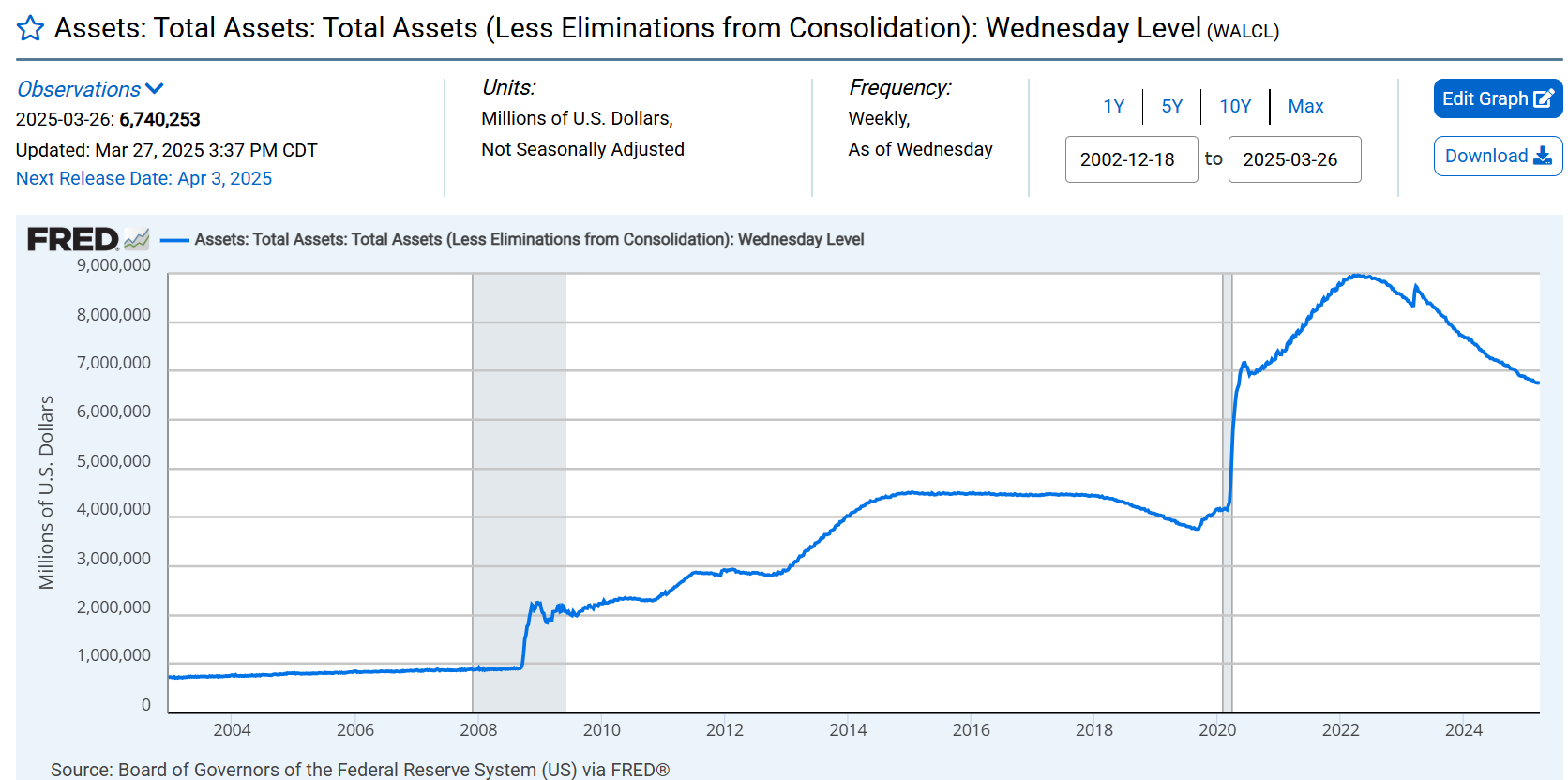

The Fed’s Balance Sheet and the Inflation Equation

Further supporting this thesis is the Federal Reserve’s shrinking balance sheet.

Pictured above, courtesy of fred.org, is a 25-year chart of the Federal Reserve’s balance sheet size.

It is essential to recognize that inflation, or at least sustained inflation, has two primary sources: an increased money supply, typically in the form of an expanding central bank balance sheet, or an increased velocity of money, often driven by rising consumer confidence.

We do not have any of those ingredients present. The Fed is decreasing its balance sheet, and tariffs have scared the general public. Moreover, short-term interest rates are at nearly 20-year highs and much higher than current inflation, and the cycle of lowering short-term rates has started.

Conclusion: Tariffs May Hurt More Than They Help

Although the U.S. stock market may face turbulence, broader economic signals point toward a potential recession. Treasury yields appear poised to trend lower, and Trump tariffs are likely accelerating that shift—not by overheating the economy, but by cooling it down.

Rather than boosting confidence and growth, the current trajectory of tariffs has raised costs and fueled economic uncertainty.

The result? America may be paying again—this time, for its own policy choices.