How Trump and Brexit are shaking up investment portfolios for 2017

A lot of things happened in 2016 that most people didn’t see coming: Prince and David Bowie died. The Chicago Cubs won the World Series for the first time in 108 years. And among economic and political shockers, the U.K.’s vote to abandon Europe’s trade bloc, dubbed “Brexit”, and Donald Trump’s stunning presidential win, despite polls that indicated both outcomes were unlikely, left financial markets gobsmacked.

The lessons for investors from the litany of 2016 surprises for next year: Brace for a whole new trading landscape as the political bombshells sink in with policy makers.

Analysts say the rising populism sweeping across the U.S. and Europe is forcing politicians and central bankers to shift their focus and priorities, portending a sea change to the regime investors have grown accustomed to since the financial crisis.

“Central banks were in the driving seat, but what we’ve learned this year is that there’s this saturation with monetary policy. At a high level, people are starting to see that monetary policies have mainly benefited asset prices and not the real economy,” said Mislav Matejka, J.P. Morgan’s chief European equity strategist.

“So there’s this shift now in focus away from monetary easing and [quantitative easing] towards more fiscal easing, more infrastructure spending, a bit more support in the final demand. And I think that will probably be the ongoing theme going into next year,” he added.

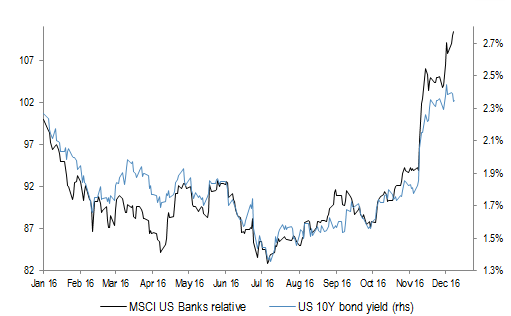

Goodbye to bond rallies, hello to bank stocks

And that’s where it becomes interesting for investors. The change of tune likely signals a farewell to a protracted period of ultralow interest rates and a multiyear bull market for bonds, and instead a hello to stocks that will benefit from higher growth and rising interest rates. Bond prices move inversely to yields, so when bonds sell off, yields move higher.

That’s a particularly beneficial scenario for the banking sector because higher rates and a so-called steepening yield curve in government bonds means banks can charge more for long-term loans than they pay to fund themselves in the short term. The yield curve refers to a plot of bond yields by their maturity.

Matejka said fund managers who have outperformed the market over the past six or seven years have succeeded by focusing on companies with dividend yields, solid cash flows, certainty and visibility—basically so-called “bond proxies.” Bond proxies are stocks, including those in sectors such as telecommunications, real estate and utilities, that offer dividends but limited growth prospects, which can be attractive in a yield-parched environment.

“With this shift now, the bondlike equities—the safer stuff, the yield plays—will get left behind and we should start to see a rebound in the reflation plays, particularly the financial sector,” he said. “There’s a big shift beneath the market surface that started 2-3 months ago, but we think it will continue.”

Policy shift ‘supercharged’ by Trump win

Financial stocks have already soared since Election Day, boosted by expectations U.S. President-elect Donald Trump will make good on his promises to boost fiscal spending and lower taxes. That combination should spur inflation and lift interest rates, which usually is a good sign for bank earnings. Moreover, he has vowed to loosen regulatory oversight on Wall Street and cut taxes.

The SPDR S&P Bank ETF KBE, +1.43% has rallied more than 24% since the vote, while Stoxx Europe 600 Banks Index FX7, -0.51% is up 15%. But the sector likely isn’t done rallying, according to J.P. Morgan Chase & Co., whose analysts are maintaining the financial sector as their key equity call for 2017, with the equivalent of buy ratings on banks in Japan, the U.S. and Europe.

“If you look at banks, the direction of bond yield is key. If bond yields keep moving up as we expect, this rotation into value and out of growth should continue and financials will be the big winner,” Matejka said.

J.P. Morgan’s upbeat tone on the banking sector is echoed by researchers at Citigroup.

More political risks loom

There are caveats to the upbeat forecasts, however. As much as Brexit and Trump unexpectedly have brightened the outlook for stocks, the same underlying dissatisfaction is still brewing in other countries and holds the potential to deliver shocks to the financial system. Most recently, the Russian ambassador to Turkey was killed on Dec. 19 and a series of attacks in Europe raised the specter of terrorism and geopolitical unrest fomenting around the globe.

Against that backdrop, the emergence of populism around the globe is likely to result in more changes to political leadership, with a spate of upcoming elections in France and Germany and elsewhere on the horizon.

France holds its presidential election in the spring, while the Germans head to the polls in September. Some analysts fear an election in Italy, after Prime Minister Matteo Renzi resigned following a rejection of constitutional reforms he championed, could pave the way for euroskeptic and antiestablishment parties to gain more power.

“We remain concerned about political risks. We suspect that a populist outcome in next year’s French presidential election would be much less equity market friendly than the Brexit or Trump votes,” Citigroup analysts said.

Article and media originally published by Sara Sjolin at marketwatch.com