The Fed is Fighting Inflation That No Longer Exists

‘Once you get burned by hot milk, you tend to blow even on yogurt’ — Turkish Proverb

On November 8th, 2022, we published a blog, ‘US Inflation in 2023 at 1.3? Is the Fed Wrong Again?’ It has been three months since that issue, so let’s revisit the data since the case.

| Year | Inflation | M2 | Velocity of M2 | Total M2 Supply | GDP | MS as % GDP | Predicted Next Year Inflation |

| 2002 | 1.59% | 5772.0 | 1.927 | 11122.6 | 10936 | 101.7% | 1.7% |

| 2003 | 2.27% | 6067.3 | 1.940 | 11770.6 | 11458 | 102.7% | 2.7% |

| 2004 | 2.68% | 6418.3 | 1.958 | 12567.0 | 12214 | 102.9% | 2.9% |

| 2005 | 3.39% | 6681.9 | 2.001 | 13370.5 | 13037 | 102.6% | 2.6% |

| 2006 | 3.23% | 7071.6 | 1.997 | 14122.0 | 13815 | 102.2% | 2.2% |

| 2007 | 2.85% | 7471.6 | 1.977 | 14771.4 | 14452 | 102.2% | 2.2% |

| 2008 | 3.84% | 8192.1 | 1.813 | 14852.3 | 14713 | 100.9% | 0.9% |

| 2009 | 0.36% | 8496.0 | 1.726 | 14664.1 | 14449 | 101.5% | 1.5% |

| 2010 | 1.64% | 8801.8 | 1.745 | 15359.1 | 14992 | 102.4% | 2.4% |

| 2011 | 3.16% | 9660.1 | 1.648 | 15919.8 | 15543 | 102.4% | 2.4% |

| 2012 | 2.07% | 10459.7 | 1.586 | 16589.1 | 16197 | 102.4% | 2.4% |

| 2013 | 1.46% | 11028.8 | 1.560 | 17204.9 | 16785 | 102.5% | 2.5% |

| 2014 | 1.62% | 11681.5 | 1.537 | 17954.5 | 17527 | 102.4% | 2.4% |

| 2015 | 0.12% | 12344.0 | 1.493 | 18429.6 | 18238 | 101.1% | 1.1% |

| 2016 | 1.26% | 13209.6 | 1.441 | 19035.0 | 18745 | 101.5% | 1.5% |

| 2017 | 2.13% | 13852.3 | 1.440 | 19947.3 | 19543 | 102.1% | 2.1% |

| 2018 | 2.44% | 14358.8 | 1.458 | 20935.1 | 20612 | 101.6% | 1.6% |

| 2019 | 1.81% | 15319.1 | 1.425 | 21829.7 | 21433 | 101.9% | 1.9% |

| 2020 | 1.23% | 19124.7 | 1.146 | 21916.9 | 20893 | 104.9% | 4.9% |

| 2021 | 4.70% | 21490 | 1.142 | 24541.6 | 22996 | 106.70% | 6.7% |

| 2022 | 6.45% | 21207.4 | 1.225 | 25979.1 | 26132 | 99.4% | -0.6% |

What is different this time? The data for 2022 in our previous issue included data as of the end of September. We have updated ALL data with the LAST data available as of the end of December 2022.

We will go over the details of the model again but in less fact. So, the US Total Money Supply M2 at the end of 2002 (first row of the table) is 11122.6 Bln USD while the US GDP was 10936 Bln USD. This means that the Total Money Supply M2 is 101.7% of the GDP. That excess over 100% is 1.7%, which becomes the expected inflation for the following year — 2003.

In our November Issue, the data pointed to 1.3% expected inflation in 2023; however, as of the end of December 2022, the model predicts a NEGATIVE inflation of 0.6% (deflation). The forecast change is reduced M2 Supply and higher than expected US GDP growth in Q4 of 2022. It is important to note that while M2 and velocity of M2 are not expected to be adjusted, nominal GDP CAN be revised! As such, the model is ONLY as good as the data it uses…

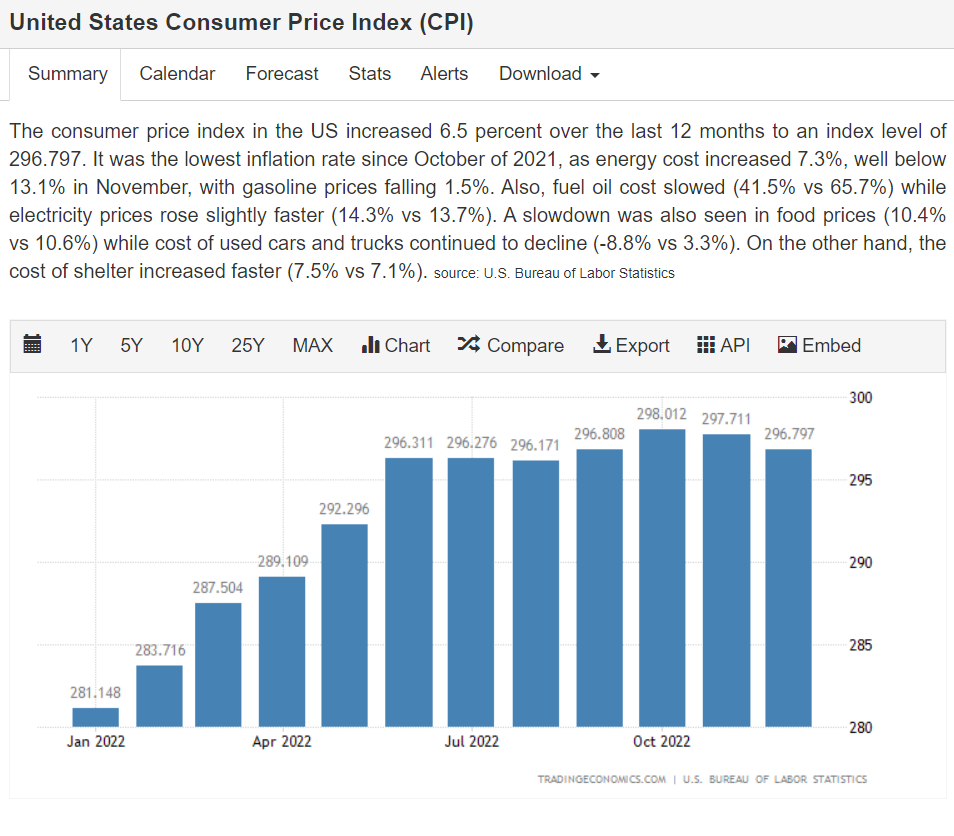

However, we will not try to “play around” with the model, nor will we try to estimate the nominal GDP of the US better. Instead, we will look at the latest inflation data. Here is the US CPI for the last 12 months:

That is right. The narrative everywhere in the media is about inflation, but the inflation, as measured by the US CPI since Jun 2022, has yet to be practically non-existent! Let’s examine those numbers a bit further:

| Year | Quarter | CPI | 3 Mo Change in CPI | 1 Yr Change in CPI |

| 2018 | Q1 | 249.55 | ||

| Q2 | 251.99 | 0.98% | ||

| Q3 | 252.44 | 0.18% | ||

| Q4 | 251.33 | -0.44% | ||

| 2019 | Q1 | 254.2 | 1.14% | 1.86% |

| Q2 | 256.14 | 0.76% | 1.65% | |

| Q3 | 256.55 | 0.16% | 1.63% | |

| Q4 | 256.97 | 0.16% | 2.24% | |

| 2020 | Q1 | 258.11 | 0.44% | 1.54% |

| Q2 | 257.79 | -0.12% | 0.64% | |

| Q3 | 260.28 | 0.97% | 1.45% | |

| Q4 | 260.47 | 0.07% | 1.36% | |

| 2021 | Q1 | 264.87 | 1.69% | 2.62% |

| Q2 | 271.69 | 2.57% | 5.39% | |

| Q3 | 274.31 | 0.96% | 5.39% | |

| Q4 | 278.8 | 1.64% | 7.04% | |

| 2022 | Q1 | 287.5 | 3.12% | 8.54% |

| Q2 | 296.31 | 3.06% | 9.06% | |

| Q3 | 296.8 | 0.17% | 8.20% | |

| Q4 | 296.79 | 0.00% | 6.45% |

Let’s split the period from 2018 to 2022 into two parts, period I from 2018 to 2020 and period II from 2021 to 2022. Period I is described by low inflation; annual inflation in any quarter is below 2.25%, and during every quarter, inflation is more volatile; it never exceeds 1.14% for any quarter!

Period II is quite more volatile! As predicted by our earlier model, inflation will show up in 2021 and it shows up with a bang! Quarter over Quarter inflation for ALL quarters of 2021 is averaging about 1.5%, and annual inflation for most of 2021 is CLEARLY above the stated inflation target of the Fed. Then 2022 arrives, and inflation gets entirely out of control! Some of the reasons are an overhang from the loose monetary policy of 2021, but some of it is due to the war in Ukraine. However, notably since Q2 of 2022 — there has been no inflation! Well, no inflation is a little of a stretch, but inflation for the second half of 2022 has been 0.17% or 0,34% on an annualized basis — well below the target inflation rate of the Fed!

Six months is not a significantly long enough time, but it is NOT an insignificant period either! The period is relatively short to be saying that inflation is under control in the US conclusively. However, coupled with the increase of interest rates from nearly 0% to almost 5% in one year and the reduction of the M2 Money Supply, we see no reason why inflation would magically reappear.

The important thing here is that this is NOT just our opinion but also the market expectations — markets believe that by the end of 2024, the Fed will lower short-term rates to 3%. Currently, market expectations are that this loosening of the monetary policy will start at the end of 2023. We really don’t know what the Fed will do or when; however, given our model and meager inflation for the last six months, we believe that the Fed might start lowering rates BEFORE Dec 2023 as it is currently priced in the government bond markets.

Sources:

Disclaimer: