Should I Buy Apple Stock Now

A Timely Decision: Bullish or Bearish on AAPL

As Apple (AAPL) gears up to unveil its second-quarter fiscal 2024 results today, investors wonder: Should I buy Apple stock now? Revenue and earnings forecasts hint at a slight drop from last year. Despite beating earnings estimates regularly, Apple faces challenges like reduced iPhone demand, tough competition, and regulatory issues, causing its stock to lag behind the tech sector.

AAPL vs. QQQ ETF

So the question is, is APPL a good fit for your portfolio? Let’s start with an examination of the 10-year price history of AAPL and QQQ ETF.

Picture in blue – AAPL, pictured in red and green bars – QQQ. As you already know, AAPL has outperformed QQQ quite a bit over the last 5 years. AAPL is up 550%, while QQQ is up only 350%.

However, over the short term, a period of 1 year, the opposite is true:

Over the last 12 months, AAPL’s price has been virtually unchanged, while QQQ has appreciated over 30% for the same period.

AAPL looks like a bargain here, but is it?

First, let’s start with valuations – the 12-month trailing PE ratio for AAPL is 26, while for QQQ, that ratio is 34.50. Just as a comparison, SPY’s PE ratio is 24.65. It does appear that AAPL looks cheap on a PE ratio basis.

Second, why is AAPL so cheap?

AAPL’s underperformance relative to QQQ started in the middle of 2023, but a slight underperformance turned into a massive divergence at the start of 2024.

What happened in the beginning of 2024?

We don’t want to take too much space over APPL’s myriad issues, but it concerns regulatory problems. The question is not necessarily what the issues are but rather what stock analysts think about those issues.

Analyst Consensus and Fair Price

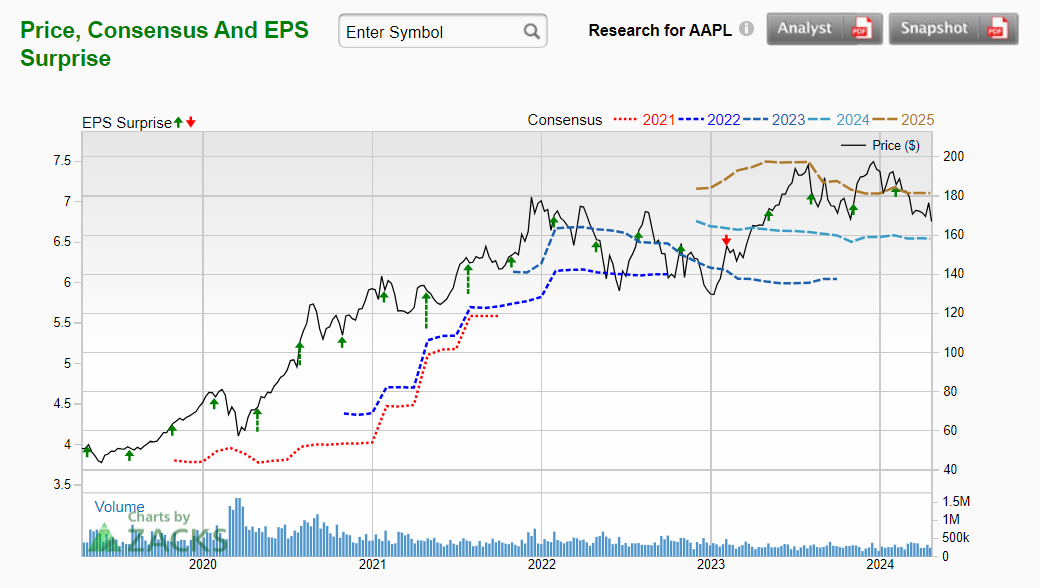

Here are AAPL’s consensus for earnings estimates according to Zacks.com:

As you can see, while APPL’s stock price is down 15% YTD, APPL’s earnings estimates for 2024 and 2025 are unchanged.

Analysts remain confident in AAPL’s profitability, with forecasts suggesting minimal impact. Even more impressive, Apple boasts a remarkable track record of exceeding earnings expectations. In fact, they’ve beaten estimates a staggering 19 out of the last 20 earnings announcements.

Apple (APPL) is one of the best companies in the world, routinely beating earnings expectations, and we see no reason why that should not continue into the future. It is important to note that while analysts can be wrong about AAPL’s prospects, their opinion, especially as a group, indicates what that future will likely be.

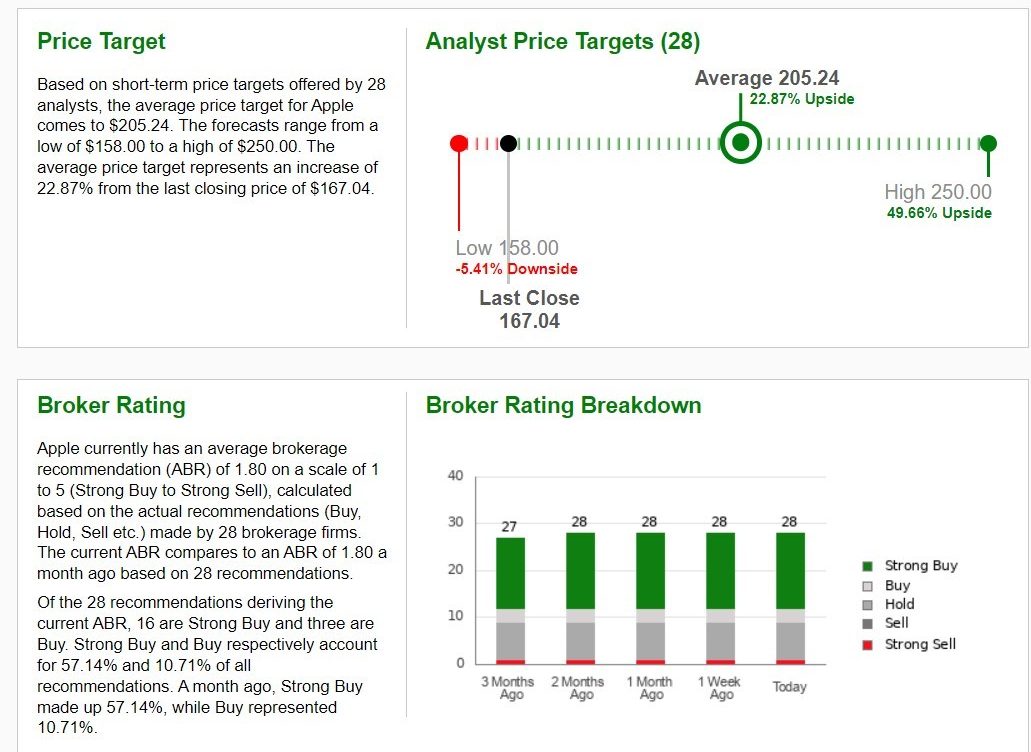

Maybe you would be interested in what analysts consider a fair price for AAPL. Here it is, according to Zacks.com.

Apple (AAPL) Price Targets

| Average Price Target | Highest Price Target | Lowest Price Target | Upside to Average Price Target |

| 205.24$ | 250.00$ | 158.00$ | 22.87% |

Analysts are practically shouting “buy” on AAPL, with a whopping majority recommending it. And who can argue with Warren Buffett? The legendary investor holds a hefty 40% stake in Apple – a clear vote of confidence.

Apple’s loyal fanbase is another reason to be bullish. They not only boast incredible brand loyalty, but also massive potential for future revenue growth. Consider iPhone penetration: it’s over 50% in the US, nearly 25% in China, and a wide-open market of 1.5 billion people awaits in India. Apple may be a giant, but its growth potential is far from limited. In fact, analysts believe the current price significantly undervalues AAPL.

Key Takeaway

We tend to agree with analysts and believe you should consider buying AAPL at current prices. While a compelling case has already been built, Apple’s aggressive share buyback program adds another layer of value for investors.

Since 2014, AAPL has repurchased a staggering 45% of its own shares, a strategy unmatched by any other company. Share buybacks directly increase earnings per share (EPS) by reducing the number of outstanding shares. They can also boost stock prices by increasing demand for the remaining shares. Additionally, AAPL leverages buybacks to lower its effective tax rate, benefiting the company and long-term shareholders who eventually sell their shares.

For comparison, the typical S&P 500 company trades at a similar P/E ratio of 25 but pays out a much higher 30% of its profits in dividends. These dividends are taxed twice at the corporate level and again as regular income for investors. In stark contrast, AAPL takes a different approach, prioritizing share buybacks while offering a more tax-efficient 15% dividend payout. This strategic move demonstrates AAPL’s strong commitment to shareholder value and potentially justifies a higher P/E ratio compared to its peers.