Start every trading day with a quick, actionable snapshot of global markets, key earnings, and the biggest movers across US, Europe, and Asia. Get the insight before your first coffee is gone.

September 27, 2023 | Issue 40

Oil Price Projections: The S-Curve, EVs, and the Future of Energy

Nikolay Stoykov

Managing Partner at Alaric Securities

If I could turn back time 20 or 30 years, one concept I’d want to grasp sooner is the S-Curve. Understanding the S-Curve and its implications on oil price projections would have been invaluable.

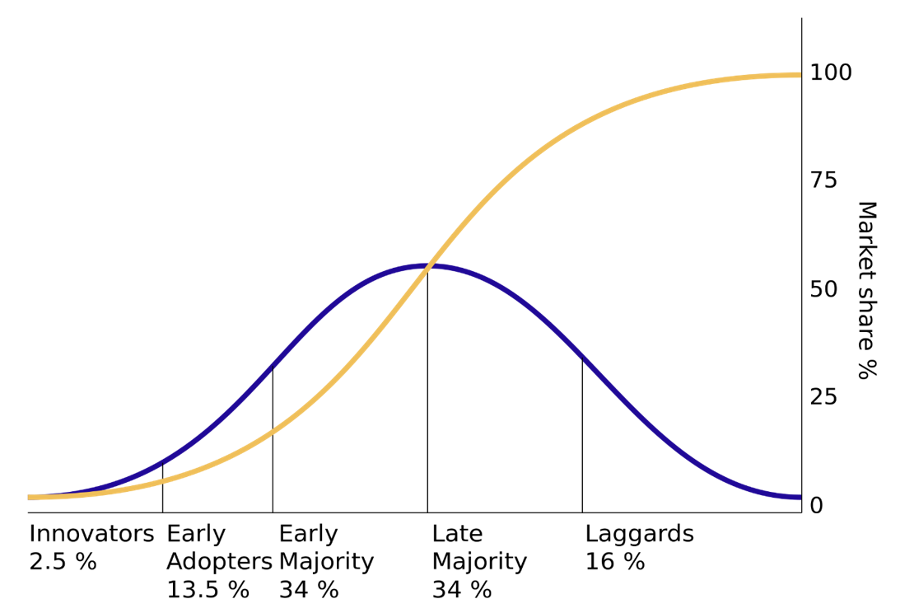

The S-Curve and Its Influence

The S-Curve, popularized by Everett Rogers in his 1962 book ‘Diffusion of Innovations,’ plays a pivotal role in shaping our insights into adopting new technologies and ideas within society. Examining this concept through the lens of oil price projections provides valuable insights into the future of the energy sector.

Here is an excellent classical example:

The critical point in the S-Curve is between early adopters and the early majority. This is usually when companies supplying the technology see a lot of growth.

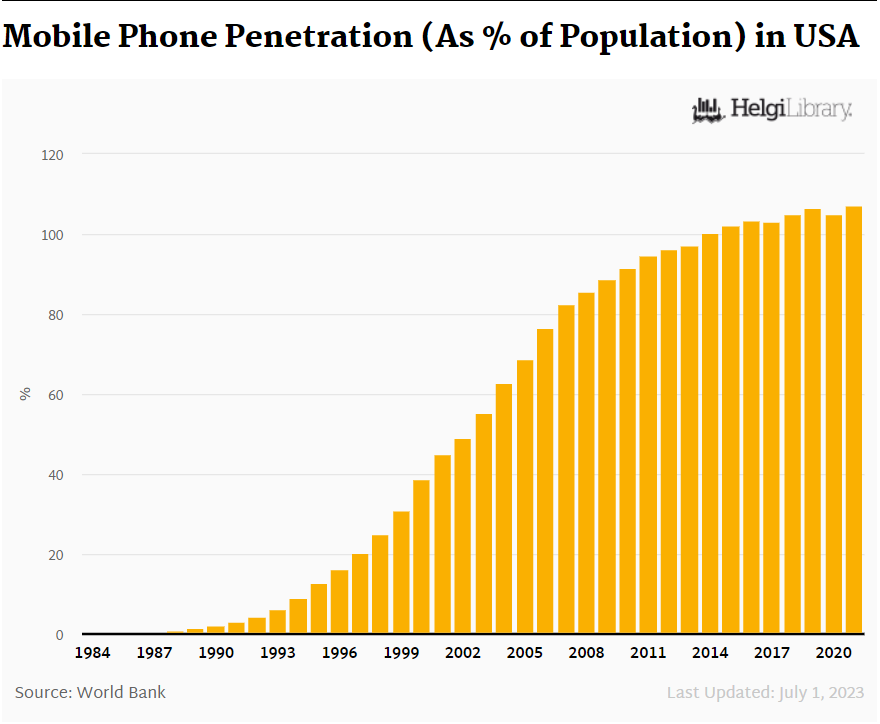

Looking back, it’s evident that the S-Curve has played a crucial role in the evolution of various innovations. Take, for instance, the mobile phone revolution—a classic example that can offer parallels and valuable lessons.

Here is the data on US mobile penetration rate, according to the World Bank:

If you remember those times, the crucial period between early adopters and the early majority must have been the mid-to-late 1990s. The chart shows that it took ten years for the penetration rate to go from 0% to 20% (1987-1997) but only four years from 20% to 40% (1997-2001).

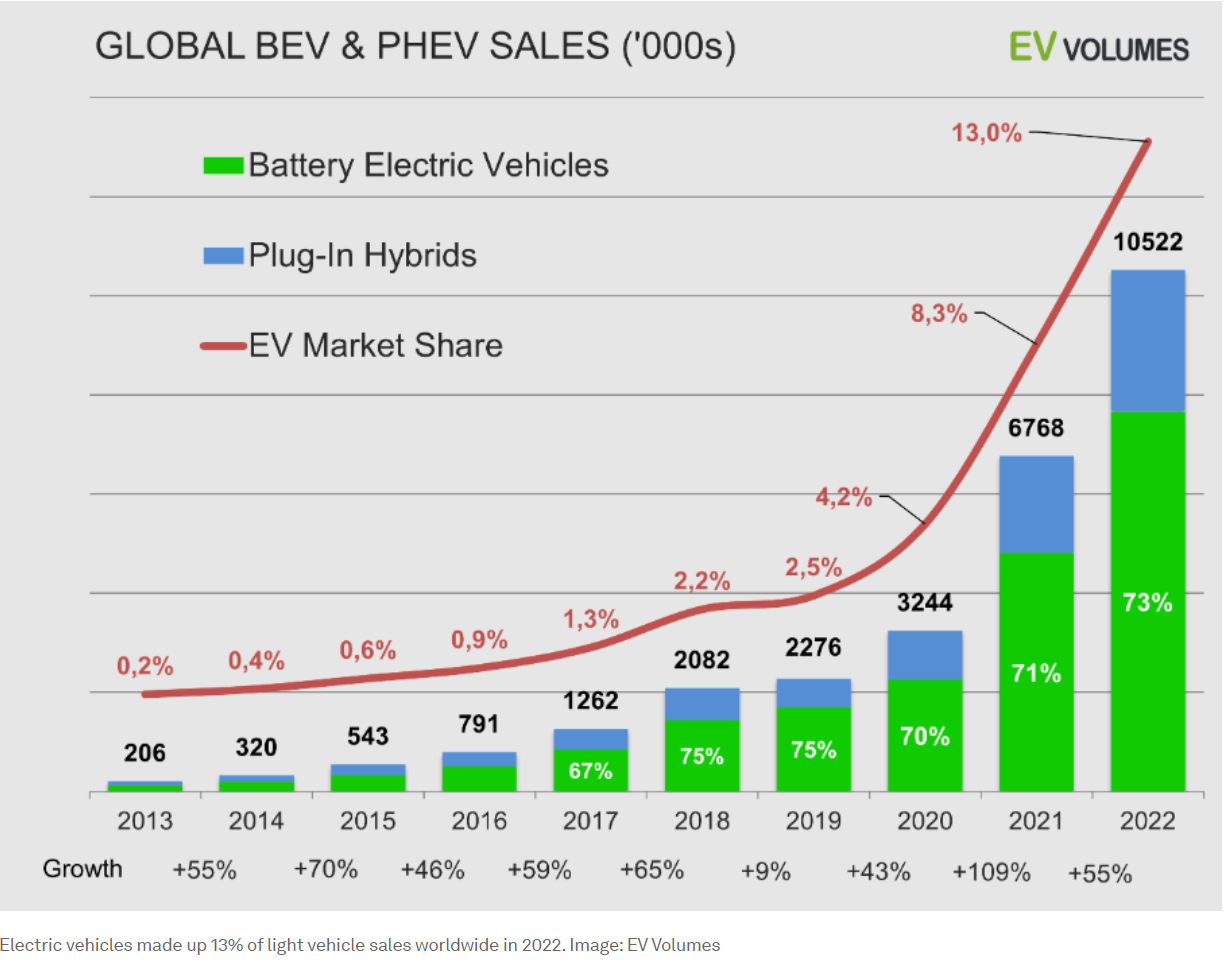

I was reminded of the S-Curve when I was looking at the growth of Electric Vehicles sales nowadays:

I don’t know about you, but looking at the chart above, I get reminded of what Mark Twain said about history – “History does not repeat itself, but it rhymes.”

Electric Vehicles and Their Impact on Oil Price Projections

Taken in the context of the S-Curve – it seems that EVs are here to stay, and soon, maybe in the next ten years, it is possible for practically all new vehicles sold in the world to be EVs. Yes, it does seem a bit aggressive on the surface, but the phenomenon of the S-Curve strongly suggests that it is indeed possible, maybe even unavoidable, even if it takes longer than ten years.

Myriad implications arise out of the possibility of this being true. One of the obvious is that TSLA might be a good investment. But this is not what we want to talk about. We want to talk about oil and oil stocks.

50% of global oil consumption comes from vehicles – cars and trucks. If, within four years, 40-50% of new global vehicle sales are EVs, what would that mean for global oil consumption? It should be down, down a lot.

What if, within ten years, 80%-100% of new global vehicle sales are EVs? Global oil demand should be practically obliterated – very similar to what happened to the need for landline phones in the late 2000s.

Market Trends and Expectations

Market trends and expectations are vital factors in shaping oil price projections. There is a surge in oil prices and a simultaneous decline in futures. This divergence prompts us to question what it signifies long-term for oil price projections.

To a degree, the markets already expect scenarios like the one described. Here are the prices for WTI Oil Futures:

| Date | WTI Price | WTI Price in 2023 dollars |

| Dec 2023 | 88.34 | 88.34 |

| Dec 2024 | 78.89 | 75.49 |

| Dec 2025 | 73.84 | 67.62 |

| Dec 2026 | 70.02 | 61.36 |

| Dec 2027 | 66.91 | 56.11 |

| Dec 2028 | 64.26 | 51.57 |

| Dec 2029 | 61.94 | 47.56 |

| Dec 2030 | 59.70 | 43.87 |

| Dec 2031 | 57.69 | 40.57 |

| Dec 2032 | 55.81 | 37.55 |

| Dec 2033 | 54.57 | 35.14 |

Since those prices reflect prices in the future, we have discounted those future prices at 4.5% a year to get the present purchasing value of those future prices. We used 4,5% because this is where current 10-year yields are.

The Future of Energy: Insights from Oil Price Projections

Many implications arise if the scenarios we described above are roughly accurate. One of the most important ones is that countries that rely heavily on oil exports, like Russia, Saudi Arabia, Iraq, and Kuwait, will likely not do that well. As a side note, the 2023 budget of the Russian Federation assumes the price of Urals Oil (most exported Russian oil) at 70 USD/barrel.

What would happen to Russia if the price of oil in 10 years drops by 50% in purchasing power from the current levels?

Conversely, countries heavily reliant on oil imports, like India, China, Japan, and South Korea, can expect to benefit from the expected lower price of oil.

But we are not here to discuss global politics; we are here to discuss financial markets.

One of the historical implications of the S-Curve is that companies that end up on the opposite side of the curve tend to trade cheaper and cheaper. Benjamin Graham would have called stocks like that “cigarette butts.”

The problem with perceived value in “cigarette butt” stocks is that extracting value from them is surprisingly tricky, and they usually end up being “value traps” – ask the shareholders of AT&T.

In conclusion, we see plenty of risks in oil and oil stocks. Yes, oil has rallied more than 20% from recent 3-month lows, but the light at the end of the tunnel is sometimes an oncoming train! We do not suggest the sector for our clients’ investments.

Disclaimer

The articles, podcasts, and newsletters from Alaric Securities OOD solely represent the authors’ views affiliated with the company; they do not represent the perspectives of Alaric Securities OOD or any of its subsidiaries or affiliates. They are provided for informative purposes and do not constitute recommendations for or against purchasing or selling security. Digital assets (such as cryptocurrency) or other assets in any account. They are neither research reports nor meant to be the foundation for any investing decisions. Any third-party information given does not represent the views of Alaric Securities OOD or any of its subsidiaries or affiliates. All investments carry risk, including the potential loss of principal, and past success does not assure future success.

Stay Ahead with Alaric Securities Newsletters

Traders and investors don't need more information - they need better information. That’s what we deliver!

Step back from the daily noise. Each issue explores market trends, industry shifts, trading opportunities, and exclusive updates — learn what's shaping the markets, not just what's trending online. Ready to get the edge?