Market Outlook 2025

At the beginning of 2025, the investment landscape presents a mix of opportunities and challenges across various asset classes. The S&P 500 is poised to build on its strong historical performance, Chinese equities hint at recovery potential, and fixed-income markets are stabilizing amid central bank shifts. With Donald Trump back in the White House, policy changes could further shape the year’s dynamics. This Market Outlook 2025 examines our view on the prospects for equities, fixed income, currencies, and key economic indicators.

1. Equities in focus

1.1. The S&P 500 and Beyond in the Market Outlook 2025

According to State Street Global Advisors, the S&P500 has returned, including dividends, an average of 10.7% a year over the last 30 years. For the last 10 years, the index’s return has been 13.35% a year. Since analysts expect earnings growth of 14.7% in 2025, the logical conclusion is to expect a return similar to the recent 10-year performance—between 13-15%.

If the S&P500 is trading around 5900, our “naïve” forecast for 2025 will be around 6700-6800.

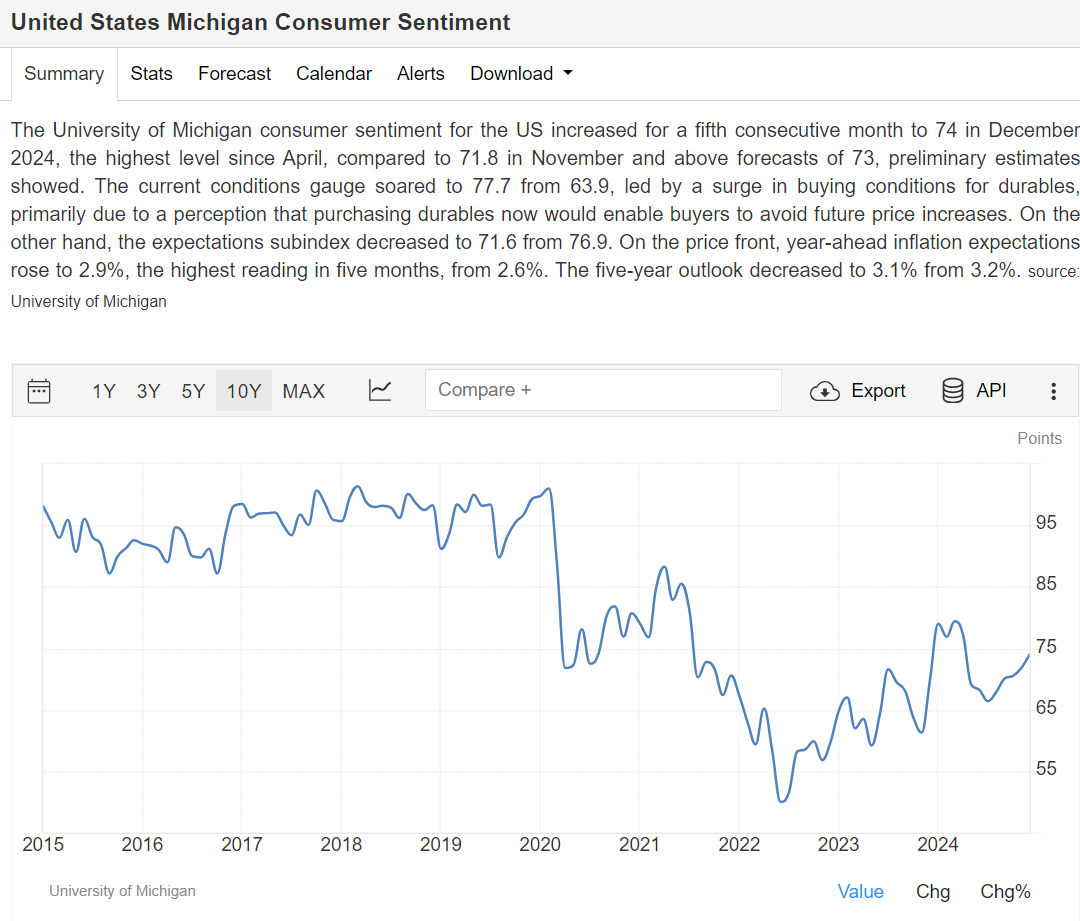

That forecast is confirmed by the relatively low consumer confidence in the US:

The chart above, provided by Trading Economics, illustrates the 10-year history of the University of Michigan consumer sentiment index. While the S&P 500 is trading at all-time highs, consumer confidence remains subdued.

This aligns well with our bullish outlook, as historical trends suggest that periods of low but improving consumer confidence often coincide with strong market performance.

1.2. Chinese Markets (FXI ETF)

Usually, we would not be making a forecast for the Chinese markets, but there are several factors that cause us to include them in this year’s outlook. First, Chinese stocks are extremely cheap. As we wrote about PDD Holdings and Chinese stocks in early December 2024, valuations are now at rock bottom. Moreover, with annual inflation in China at 0.20% for 2024, the China Central Bank has indicated that it will deploy its version of quantitative easing.

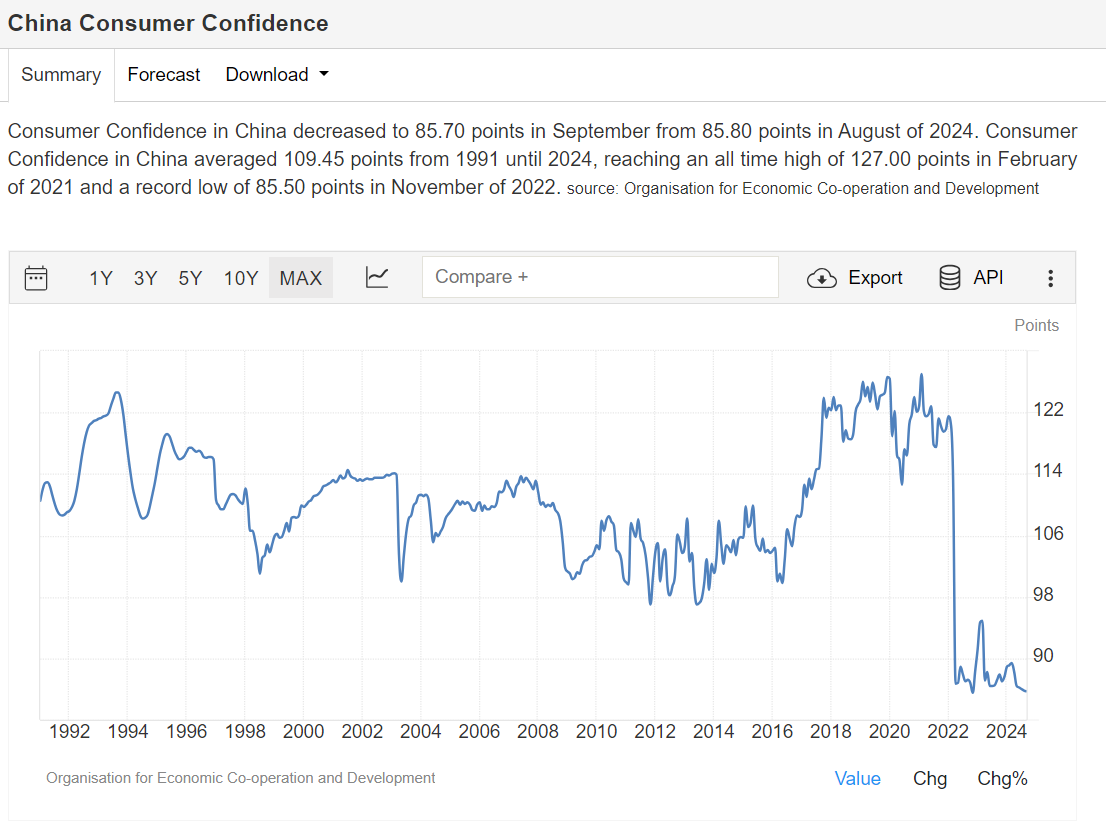

The markets have been somewhat skeptical of their efforts. Still, with inflation so low, the Central Banks have many tools at their disposal, and they may introduce new, even more aggressive measures if the currently proposed don’t work. In the meantime, Chinese 10-year rates are at an all-time low of 1.7% per annum, and consumer confidence in China is now way worse than in 2008:

It is important to note that the composition of the FXI ETF and most other China-focused ETFs today is vastly different from that of the ETF 10 or even 5 years ago. Many of the companies that are now the primary constituents of the ETF were not even listed 10 years ago.

Moreover, stock analysts universally recommend them, and we believe that the current levels of the ETF offer incredible upside.

2. Fixed Income

2.1. US 10-Year Treasury Rates

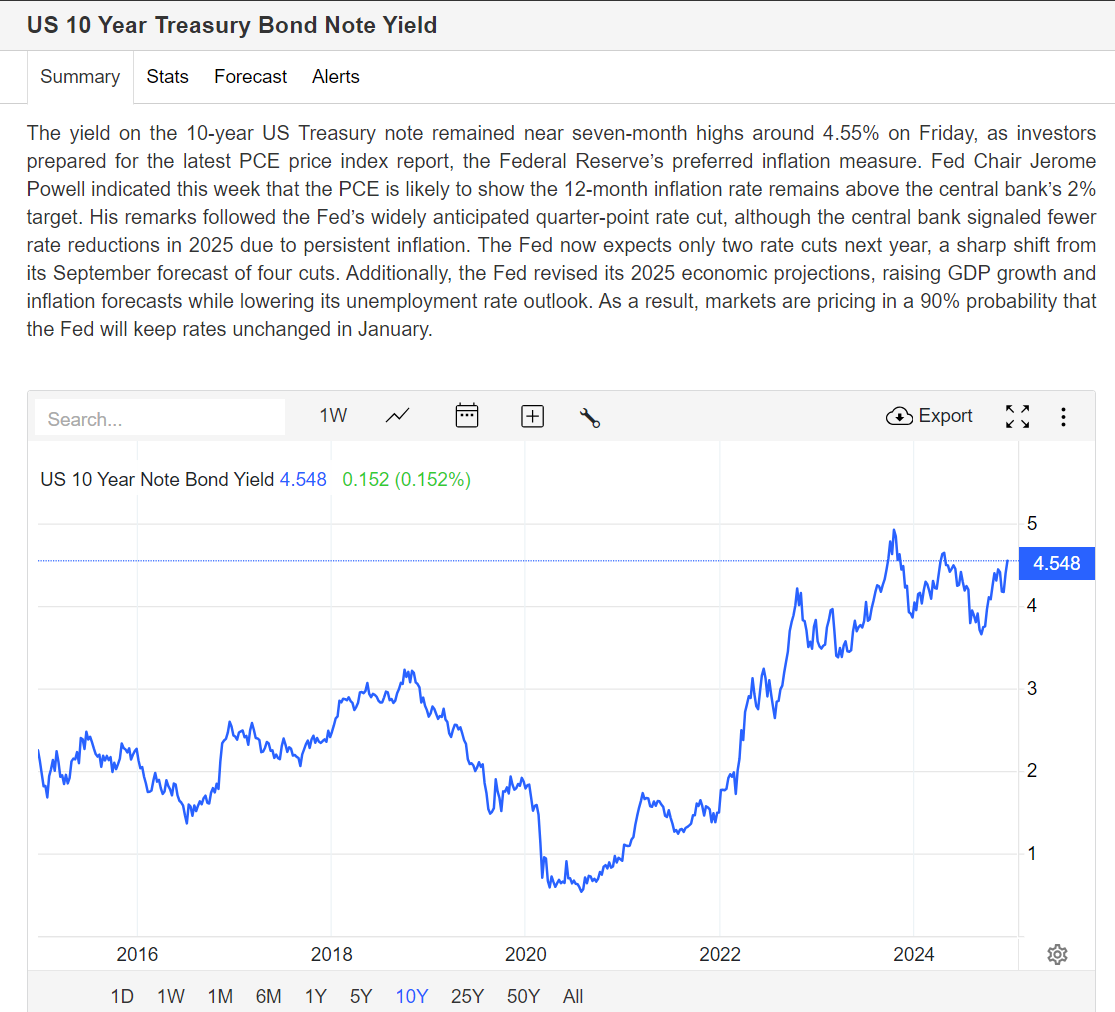

Pictured above is the 10-year history of US 10-year rates, courtesy of Trading Economics. While interest rates are hovering near their recent highs of 4.55%, 2024 was a different year from 2023 and 2022. The most significant difference is that the Fed started lowering rates, and short-term rates are now below the 10-year benchmark (normal interest rate curve). In our opinion, this normalization indicates lower volatility in the future.

While inflation remains above the target rate of 2%, the 1-year expected inflation, which includes President-elect Trump’s tariff impact, is at 2.65%. That level is not low, but it is way below the current Fed Funds rate of 4.25%-4.50% and way below the 10-year rate of 4.55%. It is important to keep in mind that before 2020, Fed Fund rates were around inflation levels, while 10-year rates have averaged a premium of 1% relative to inflation.

The Fed is keeping that premium high but long-term averages are long-term averages for a reason. We really think present levels of US long-term rates are high and unlikely to stay at present levels. We certainly believe that 10-year rates will drop below 4% in 2025.

2.2. EUR Rates

Similarly to US Rates, the interest rate curve in EUR has largely flattened—interest rates are roughly around 2.5% in most parts of the curve. This is actually an incredible transformation, as only one year ago, short-term rates were above 3.5% while long-dated rates were close to 2.5%.

While inflation continues to be elevated at 2.2% annually, growth in the Euro Area is quite anemic—0.4% annually, which is 3.1% in the US. Yes, the ECB is working hard to ensure that rates do not suffocate Europe’s fragile economies.

Given the weak economic growth and strong trend of declining inflation, we expect rates in EUR also to go significantly lower if inflation subsides below the 2% annualized rate. We expect Germany’s 10-year rate in EUR to drop below 2% in 2025.

3. EUR/USD Exchange Rate

As we wrote in November 2024, we are bullish on the EURUSD (long EUR, short USD). Here’s what the chart, courtesy of Yahoo Finance, reveals:

We are using a weekly chart with a 50-week moving average, which we deem to be a proxy for fair value. The present level is 1.04, and the moving average is 1.0824 (where we roughly think fair value is). Here is the reason for our opinion: The reason for the recent move from 1.10 to 1.04 is the hawkish Federal Reserve. Inflation expectations for the Euro Area in 2025 are for 2.5% annual inflation, while those in the US are for 2.6%.

However, the German 1-year rates in EUR are already at 2.22% while the US 1-year rate is 4.25%. Given that expectations for the next 12 months of Fed policy actions are modest, we think the dollar strength is already priced in. If there is a surprise, that surprise should be in the form of more aggressive lowering of interest rates by the Fed. Anyway, if ECB short-term rates are already at the expected inflation level, why would the Fed keep rates so high? What if expected inflation is lower – just 3 months ago, markets were pricing 4 rate cuts for the next 12 months instead of the current two cuts.

It is important to note that while the high interest rates in the US have not significantly hurt the stock market, they have had a tangible impact on the real economy, especially the housing market. Existing home sales are near a 20-year low, and the high cost of mortgage financing will be an essential issue for President-elect Donald Trump. While the Fed is technically independent, it is not immune to pressure from the government or the public at large.