German 10 Year Bond Yield Spikes as ECB Rate Cuts Fuel Eurozone Debt Fears

The first week of March 2025 was quite an eventful week for European interest rates. First, the European Central Bank (ECB) lowered its deposit facility rate for the sixth time over the last 12 months. At the same time, the German 10 year bond yield made a fresh new 10-year high, pun intended, and traded above 2.90%.

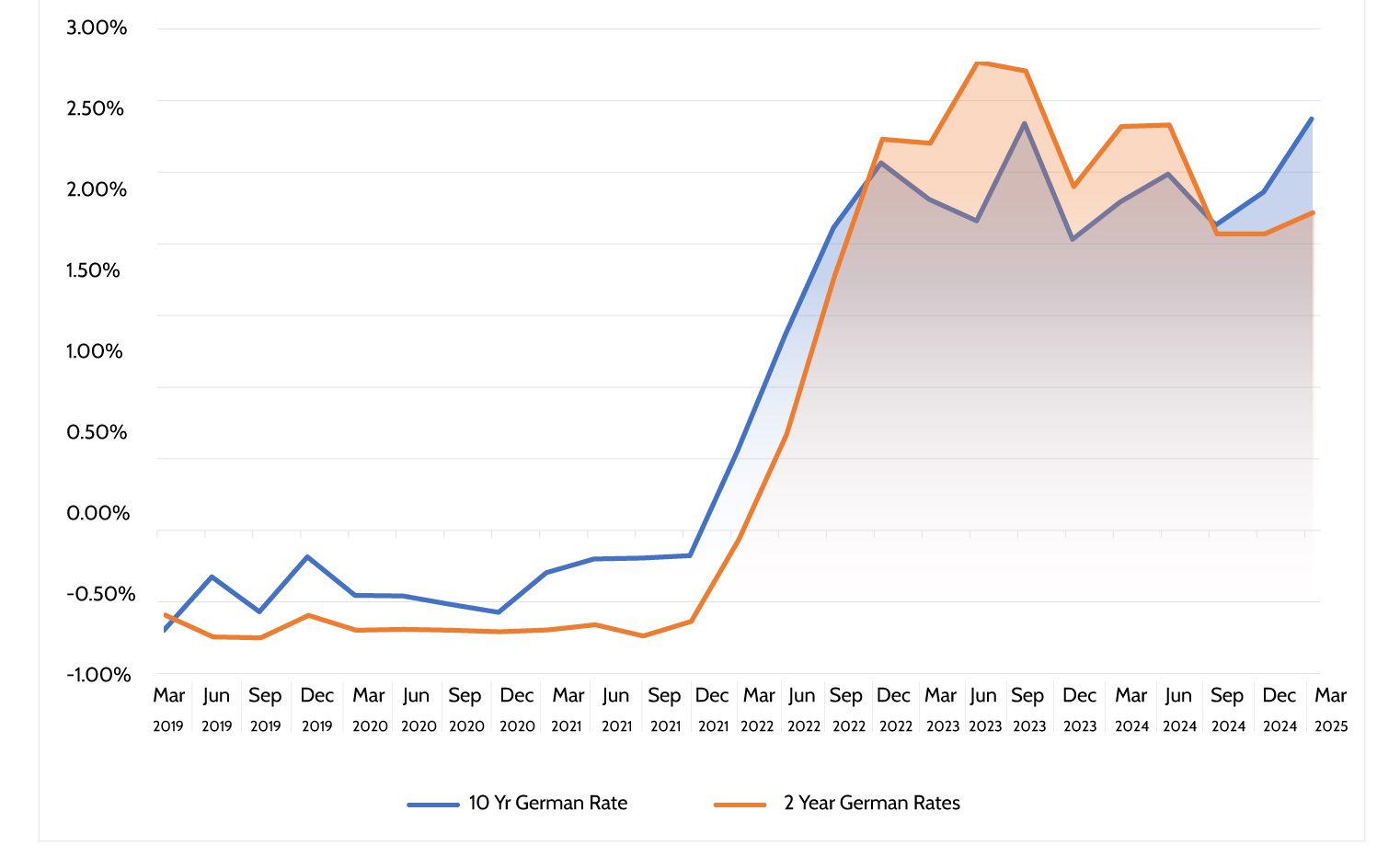

For a clearer perspective on the scale of this movement, consider the one-year historical chart of German 10-year rates below, courtesy of Trading Economics.

The Dramatic Move: German 10-Year Bond Yield Spike 0.50% in One Week

Yes, the move in the German 10-year bond yield was quite dramatic. The rate moved by 0.50% in one week. Similar moves were observed in all European interest rates, mainly the Euro Area, but moves of such magnitude were observed in the UK (GBP 10-year rates) and Switzerland (CHF 10-year rates).

Let’s examine the relationship between German 2-year and German 10-year rates:

While the spread between German 10-year and 2-year rates is near its 5-year high, the shorter-term (2-year) rates remained relatively stable—nearly all the movement took place in the long-dated yields.

Germany’s €500 Billion Borrowing Plan: Necessary or Excessive

The sudden rise in the German 10-year bond yield wasn’t random. It was driven by Germany’s announcement of a plan to borrow approximately 500 billion euros for future infrastructure and military investments.

So, the big question is – is the move in rates justified?

There are few specifics about Germany’s borrowing proposal, including the timeline and detailed breakdown.

Few specifics about the proposal have emerged, and as of now, it remains only a preliminary plan—with no clear timeline or detailed breakdown of the borrowing needs.

However, we can gain insights from key statistics:

- Germany’s GDP was $4.5 trillion in 2024, with government debt at approximately 63% of the GDP ($2.8 trillion).

- The proposed borrowing could push this debt ratio up by about 11%.

Considering the broader context, total Eurozone government debt was approximately 88% of the GDP in 2024. Germany’s proposed new debt would represent just 3.5% of total Euro Area debt, suggesting the market’s dramatic reaction may be disproportionate.

Market Expectations vs. Fiscal Reality

The proposed new debt is 3.5% of all Euro Area Debt, hardly the Armageddon the market seems to be implying. Our interpretation of the market reaction is that the market believes that all Euro Area countries will increase borrowing by a similar percentage of GDP. That is quite the extreme interpretation.

While Germany seems in a perfect fiscal position, many other Euro Area countries like France (111% Debt/GDP) and Italy (135% Debt/GDP) cannot increase government spending by anything nearly as big.

European interest rates markets are now predicting something quite extreme—nearly 100% certainty that within 2 years, ALL, or practically all, European governments, including Switzerland, will increase spending by at least 2%- 4% of GDP annually on their militaries. We find this to be quite the extreme interpretation.

To begin with the obvious, Switzerland is not a member of NATO and, as such, will not spend to the degree Germany has undertaken.

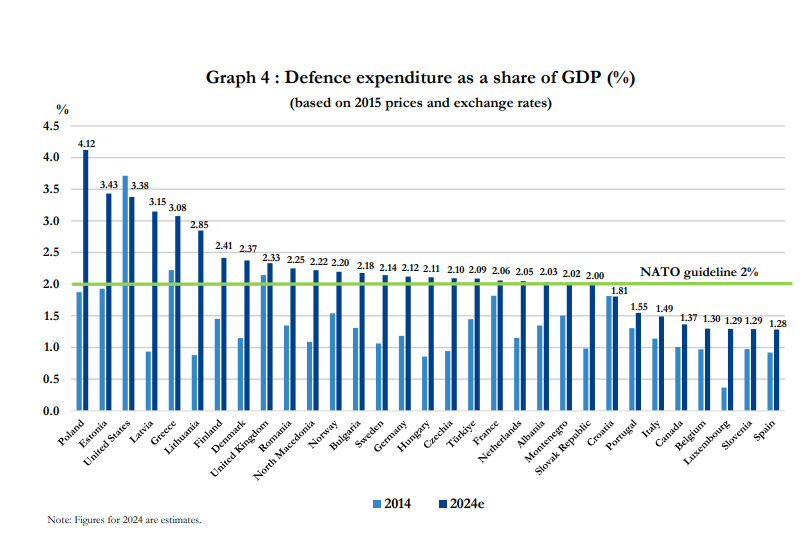

Moreover, even within NATO country members and Euro Area country members, there is no consensus for such a drastic increase in military or any government spending for that matter:

According to NATO data, most European NATO members are now spending above the 2% of GDP target. However, most are barely above the targets, and some South European NATO members like Italy and Spain are still well below it. And if history has taught us anything, it is that the status quo is always favorable to stay – yes, on January 1, most people aspire to change, but by February 1, that aspiration is long forgotten. Call us skeptics if you want, but we are unsure if Germany will undertake such dramatic military spending. However, for Spain, Italy, and even France to follow suit any time soon is hard for us to believe.

Investment Opportunities

The recent spike in European interest rates may create attractive opportunities for bond investors, especially in Euro Area government debt outside Germany. Romanian euro-denominated bonds stand out as particularly appealing, offering yields exceeding 5%, with some longer-term bonds reaching as high as 6.5%. These elevated yields present notable value for long-term investors.