ECB Interest Rates Cut: A Global Rate Cycle Begins

On the 6th of June, the European Central Bank (ECB) made a significant move with its latest ECB rate cuts, lowering its deposit rate and two other key ECB interest rates by 0.25%. This decision, effective from the 12th of June, 2024, reduces the rates from 4.5% to 4.25%

Although widely expected, this decision has far-reaching implications beyond the initial muted market reaction.

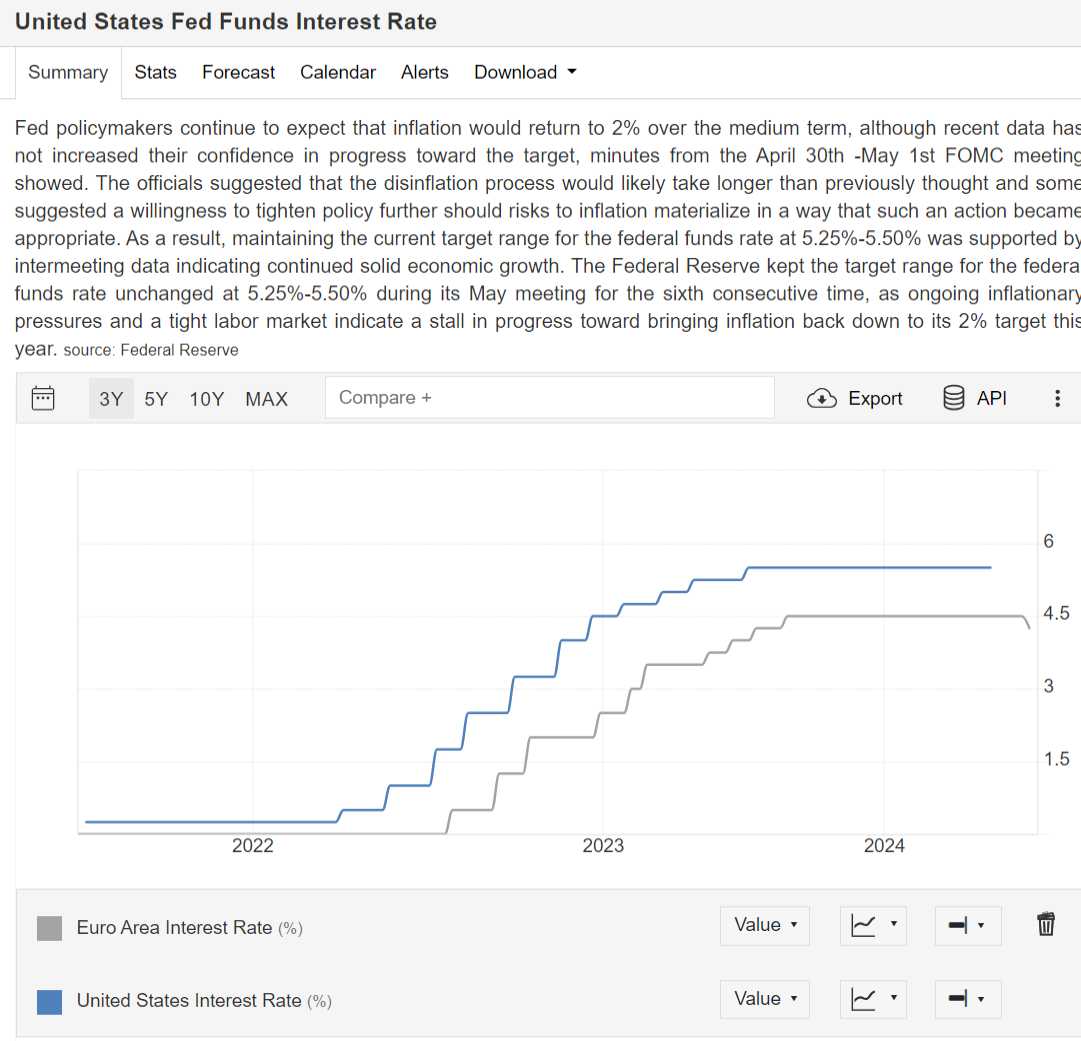

Let’s start with the context. Central Banks’ rate decisions nowadays tend to be coordinated and correlated. Please see the ECB’s deposit rate and Fed Funds rate for the last three years:

We have plotted only the ECB and the Fed, but we could have added most of the G7 countries’ central banks. We still would have seen similar dynamics – a coordinated and relatively fast pace of interest rate rises in 2022 and early 2023, followed by a long pause in the second half of 2023 and the first quarter of 2024.

he ECB has not been the first central bank to lower rates. The Swiss National Bank already lowered its rate on the 21st of March this year, but given that Switzerland is a much smaller economy, the ECB’s decision is much more important.

Ok, so those were the facts. Now, let’s look at the meaning behind these facts.

Interpretation 1)

Given the strong correlation in the interest rate decision-making process between the ECB and the Fed, it is highly likely that the Fed will follow suit and begin lowering rates in 2024.

This is not a radical interpretation. Мarket expectations align with this, anticipating the Fed to lower rates twice in 2024.

Interpretation 2)

Small crops get smaller, big crops get bigger.

This is, relatively speaking, an extreme interpretation and would require a further explanation. The statement above is a common saying among agricultural traders. It arises out of the fact that markets are rarely completely rational but rather tend to often overreact to positive or negative data.

The implications for interest rates are that once the process of interest rate rises or cuts starts, it tends to go much further than most market participants expect at the beginning of the process.

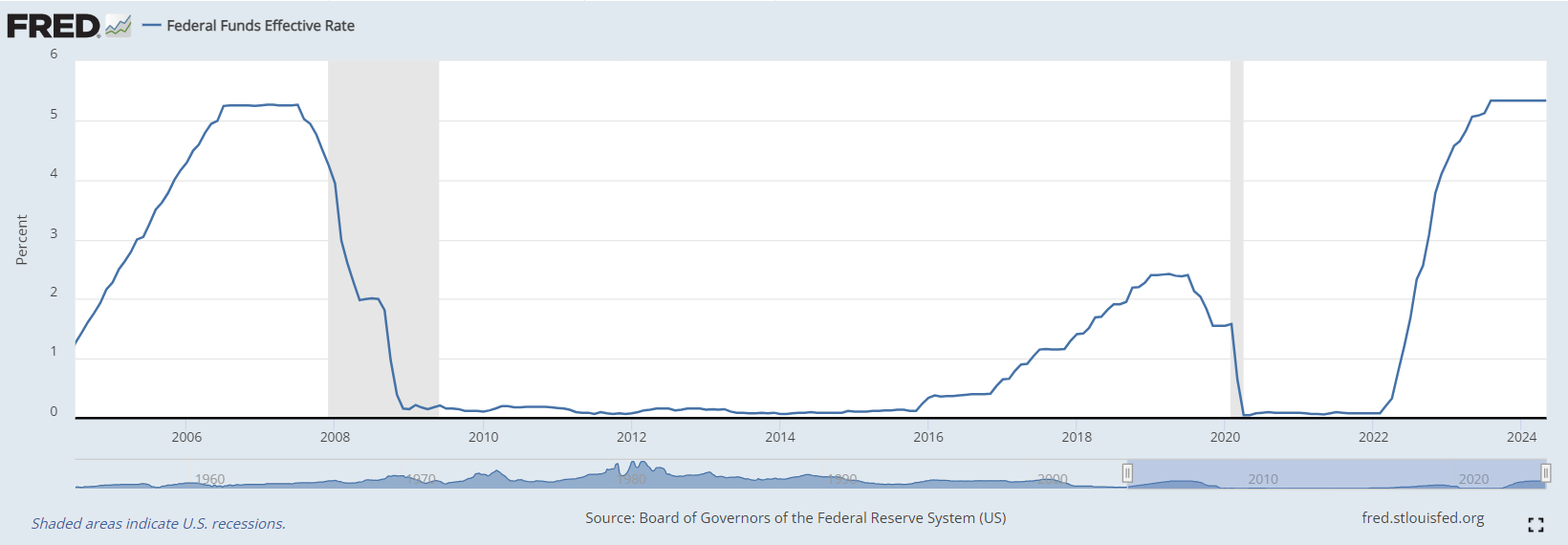

Let’s see below the history of US Fed Funds for the last 20 years.

As you can see for themselves Fed Funds have been near 0% quite a bit over the last 20 years. While inflation is still elevated, and most market participants expect the Fed to lower rates in 2024 and 2025 only by 1% to 4.25% overall, one can’t help but wonder if rates will really be lowered by only 1%.

The saying ““Small crops get smaller, big crops get bigger” exists for a reason – because it is usually true. What has been the reality for the last 20 years is statistically favorite to stay. Statistically speaking overnight drastic changes in large populations and economies are nearly impossible.

Call us crazy but we think that Fed Funds are at least probable to head much lower than the 4% level in the not-so-distant future. Why not eventually go to 2% or even 1%? Small crops get smaller, and big crops get bigger for a reason.

Key Takeaway

In conclusion, we are going to say that the ECB rates cuts signals the beginning of a new interest rate cycle for most advanced economies – a cycle of rate cuts. History suggests that market expectations at the beginning of such a cycle are quite conservative.

In our opinion it is quite possible to see EUR and USD short-term rate head much lower over the next several years than what most people currently expect. The inflation levels we saw in 2021 and 2022 were an anomaly that is unlikely to be repeated in the future, and expectations of USD rates not lower than 4% and EUR rates not lower than 2.5% are quite conservative.

However, the most important thing is for investors to buy fixed-income instruments. Even shorter-dated, up-to-1-year instruments have quite a bit of value. Interest rates in the developed world economies are going down, and present levels of government bond yields are unlikely to stay.