Draghi Sends Corporate Yields So Negative He Can’t Buy Them

- Yields on some company bonds are quoted below minus 0.4%

- Central bank asset purchases now exceed 1.3 trillion euros

The European Central Bank is starting to price itself out of the corporate-bond market as yields plumb such lows that some notes are no longer eligible for its purchase program.

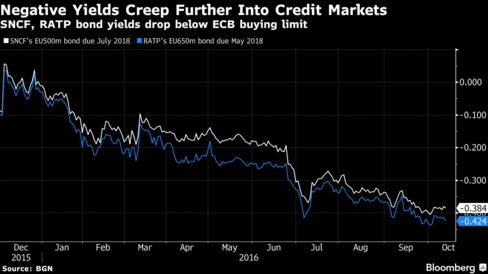

ECB President Mario Draghi’s unprecedented buying of corporate debt has sent borrowing costs tumbling to a record and now yields on some securities are so low they fall outside the ECB’s own criteria. Yields on bonds from Paris’s public transport network have already dropped below the threshold of minus 0.4 percent, while those from Siemens AG, Europe’s biggest engineering company, French train operator SNCF and Sagess, which manages the nation’s strategic oil reserves, are also approaching the cut-off point.

The increasingly negative yields are raising questions about how much more the ECB can do in credit markets to stimulate growth. Yields on 2.6 trillion euros ($2.9 trillion) of government bonds in Europe have already turned negative after the central bank bought 1.3 trillion euros of fixed-income assets, including 32 billion euros of corporate bonds.

The ECB has bought an average of about 7.4 billion euros a month of investment-grade notes, beating estimates of a maximum of 5 billion euros by analysts at Commerzbank AG and Morgan Stanley before buying started in June.

That pushed the average yield on euro corporate bonds down to a record-low 0.59 percent last month, and the rate was 0.74 percent on Thursday, according to Bloomberg Barclays bond index data. The dynamic has been exacerbated by investors piling into the safest securities as concern about Deutsche Bank AG’s financial health roiled market sentiment.

The notes from Regie Autonome des Transports Parisiens are quoted at a yield of minus 0.42 percent and yielded as little as minus 0.44 percent in the secondary market earlier this month, according to data compiled by Bloomberg.

Relative Value

The ECB lists bonds from state-owned RATP and SNCF among its corporate-bond holdings. The notes offer a premium over two-year French sovereign bonds which yield minus 0.61 percent, Bloomberg data show.

“It’s a relative game,” said Rik Den Hartog, a portfolio manager at Kempen Capital Management in Amsterdam, which oversees about $5.9 billion of credit and invests in negative-yielding bonds. “If I keep the money in a bank account, or buy a government bond that yields even less, that hurts more than investing in a corporate bond, even at a negative yield.”

Other securities may be poised to follow suit. Bonds of Sagess are quoted at a yield of minus 0.29 percent, while Siemens notes due June 2018 trade at minus 0.24 percent, according to data compiled by Bloomberg.

While the ECB’s job could get harder if more bond yields fall below the threshold, there may currently be as much as 671 billion euros of corporate notes still available for purchase, according to analysis of the bank’s criteria and bond data by Bloomberg. There’s also nothing stopping the bank buying bonds near the threshold since they won’t have to sell them even if they subsequently fall below the limit.

‘Feels Wrong’

“As long as the ECB sticks to its buying limit of the deposit rate, there are lots of corporate bonds they can still buy,” said Den Hartog. “Most are trading at a level where they’re still eligible.”

Negative rates are also a concern for investors, especially pension funds and insurers, which need a certain level of yield to provide the return they guarantee to policy holders. Investors are buying longer-dated and riskier securities to generate returns. Thomas Kristiansson, head of credit fixed-income at SEB Investment Management refuses to buy bonds with negative yields and tries to sell holdings whose yields drop below zero.

“It’s crazy,” said Kristiansson at SEB in Stockholm, which manages more than 100 billion euros. “It feels wrong to buy something at a negative yield. It’s definitely become harder to generate returns. This year the market has performed well but next year it will be very difficult to generate value for clients, starting from zero.”

ECB Tapering

Negative yields have put credit investors between a rock and a hard place. Low rates may be making it harder to generate income for savers but any withdrawal of quantitative easing risks sparking a selloff in fixed-income assets.

Euro-area central bank officials are expecting the ECB to gradually wind down bond purchases before the conclusion of quantitative easing, possibly in steps of 10 billion euros a month, Bloomberg News reported earlier this month. European bonds fell the day after the report.

The central bank has said it would be willing to extend the program beyond the end date of March 2017, if euro-area inflation weren’t on track for a target of just under 2 percent. With the rate at 0.4 percent last month, investors are hopeful the buying may be expanded or extended.

“The purchases have only been going for four months and already investors are thinking of how they can be expanded,” said Zoso Davies, a credit strategist at Barclays Plc in London. “Investors appear to be 100 percent convinced that the buying will go on forever. Instead, they should be thinking about the risk that it is tapered or stopped.”

Article and media originally published by Katie Linsell at bloomberg.com