BABA Stock Valuation: A 33% Discount Story

Last week in our blog, we covered the most loved U.S. large-cap stocks for 2025, including names like MSFT, AVGO, NVIDIA, WMT, and AMZN (aka MANWA). While these stocks are favorites among analysts, they’re also trading at high valuations.

That’s why this week, we’re shifting focus to a stock that offers a rare opportunity: a top-rated large cap trading at a significant discount. We’re talking about BABA stock valuation and why Alibaba Group (BABA) may be one of the most compelling large-cap investments of 2025.

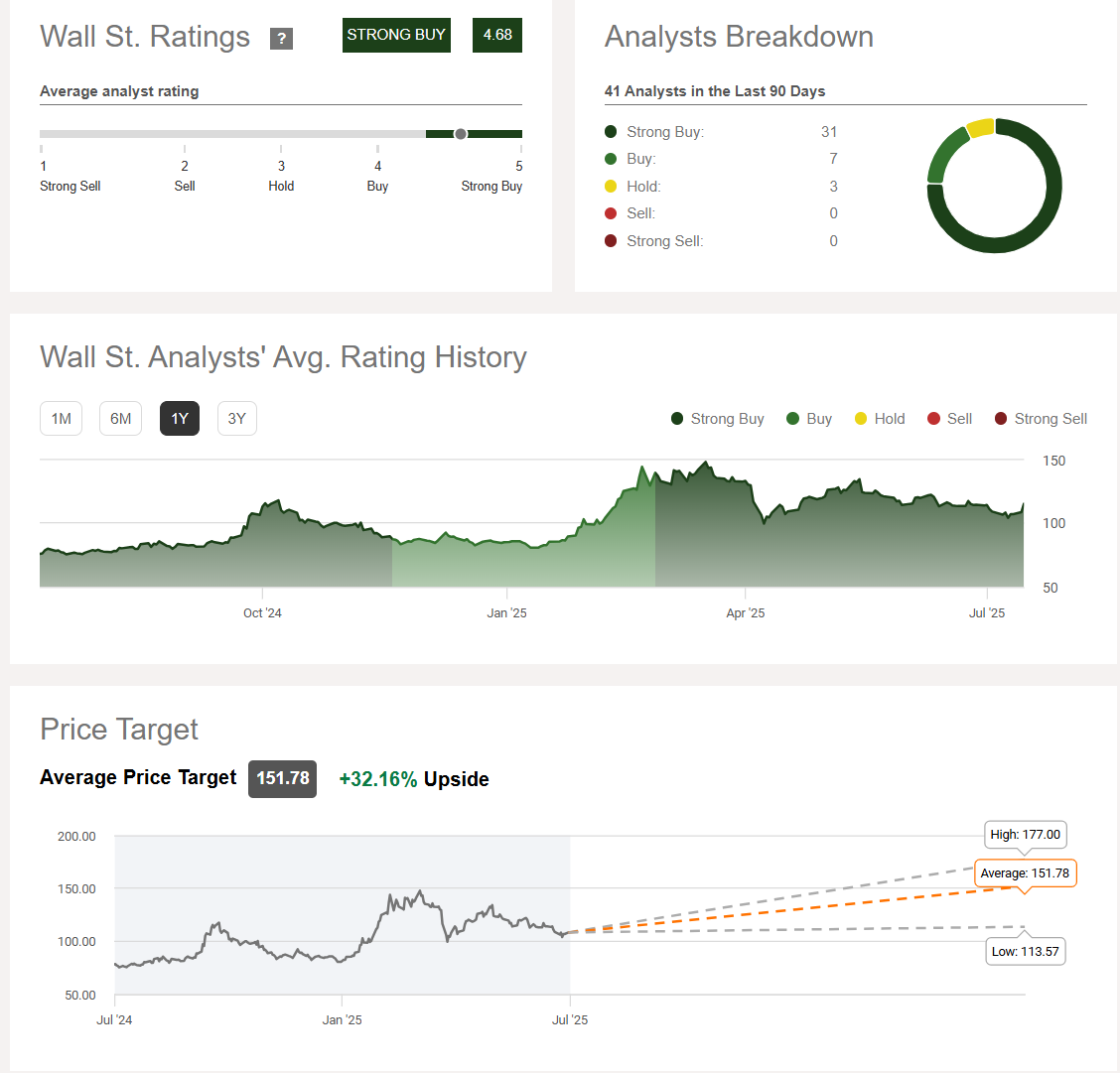

BABA Stock Rating: Higher Than Amazon

According to Seeking Alpha reports that BABA stock has a Wall Street analyst rating of 4.68. To put that in perspective, Amazon (AMZN), the top-rated U.S. large-cap stock, has a slightly lower score of 4.64.

Even more striking: BABA is trading at a 33% discount to the consensus price target. The current share price is around $115, close to the lowest target of $113.36, while the average price target stands at $151.78.

Large-cap stocks, such as BABA, rarely trade more than 30–35% below the consensus value. It’s even rarer to see them fall below the lowest target. That gap is the kind of pricing edge savvy investors look for.

Alibaba at a Glance

According to Wikipedia, Alibaba is a Chinese multinational technology company that operates across e-commerce, cloud computing, digital media, and logistics.

Since its U.S. listing, BABA stock valuation has ranged significantly, often trading at a P/E ratio of 20 to 30, consistent with its U.S. tech peers. But post-2022, a shift occurred.

What Happened to BABA’s Valuation?

Starting in 2022, BABA’s valuation sharply contracted. The P/E ratio dropped to around 10, a level more typical of stagnant or declining industries, rather than one of China’s largest tech giants.

Why the shift?

-

The Chinese government launched a tech crackdown, with BABA being a primary target.

-

The Chinese economy slowed, particularly in the real estate sector, which reduced consumer demand and put pressure on margins.

-

Global investors became wary of geopolitical and regulatory risk in Chinese stocks.

Despite that, signs point to recovery: consumer sentiment is improving, and macro growth is beginning to stabilize. That could mean earnings growth is poised to rebound, and with it, the stock price will likely follow.

BABA Stock Valuation: Metrics That Matter

Here’s a snapshot from Finviz:

-

Price: ~$115/share

-

Cash per share: $28.61

-

Book value per share: $60.30

-

Forward P/E: 10.91

-

5-Year EPS Growth Estimate: 8.94%

If next year’s EPS is projected at $10.50 and we exclude just the cash, BABA trades at a forward P/E of 8.2—an extraordinary value for a global tech leader.

Conclusion: The Case for BABA Stock in 2025

With a strong analyst rating, a valuation gap of over 30%, and signs of earnings recovery, BABA stock valuation presents a compelling opportunity in an otherwise expensive large-cap landscape.

Yes, China risk is real, but so is the potential upside. When Wall Street gives a stock higher marks than Amazon, yet it trades at one of the deepest discounts in the large-cap space, it’s worth more than a passing glance. That kind of disconnect doesn’t happen often and rarely lasts.

Looking for more high-conviction opportunities? Don’t miss our latest take on Circle Internet, which skyrocketed over 700% after its IPO but now faces tough questions on valuation: Is It Time to Go Long or Short?

So, Wall Street loves BABA.

Shouldn’t you at least take a closer look?