Start every trading day with a quick, actionable snapshot of global markets, key earnings, and the biggest movers across US, Europe, and Asia. Get the insight before your first coffee is gone.

January 28, 2025 | Issue 95

UBER Stock: Buy, Sell, or Hold

Nikolay Stoykov

Managing Partner at Alaric Securities

Uber Technologies, Inc. (NYSE: UBER) will release its Q4 2024 earnings report on Wednesday, February 5. The $144.81 billion company dominates ridesharing, food delivery, and logistics.

Analysts expect Uber to post earnings of $0.50 per share for the current quarter, reflecting a 24.2% year-over-year decline. The Zacks Consensus Estimate has dropped by 11.6% over the past 30 days, signaling cautious sentiment.

On the other hand, analysts project earnings of $1.86 per share for the full fiscal year, marking an impressive 113.8% increase from the prior year. However, this estimate has been adjusted downward by 7.9% over the past 30 days. The upcoming report will be crucial in revealing how Uber navigates its strong growth amid regulatory pressures and rising competition.

With that in mind, let’s examine why analysts remain bullish on Uber, starting with their recommendations and price targets.

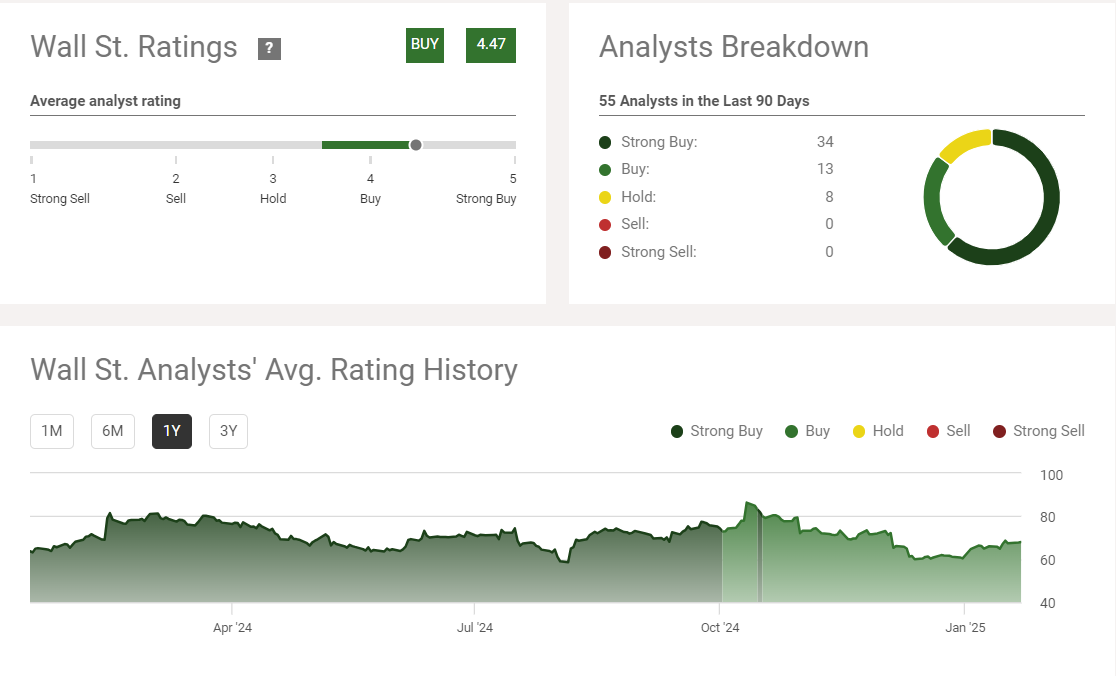

Analyst Recommendations: Strong Confidence in Uber Stock

As highlighted by SeekingAlpha.com, Uber has consistently been endorsed as a “Buy” by stock analysts. Over the past 90 days, 55 analysts have provided updates, with 34 issuing Strong Buy ratings (62%), 13 giving Buy ratings (24%), and only 8 assigning Hold ratings (14%). This comfortably exceeds our benchmark threshold of 75% Buy or Strong Buy ratings. Notably, there is not a single Sell rating among them.

This overwhelmingly positive sentiment reflects strong confidence in Uber’s prospects. To get a clearer picture of their outlook, let’s examine the analysts’ price targets.

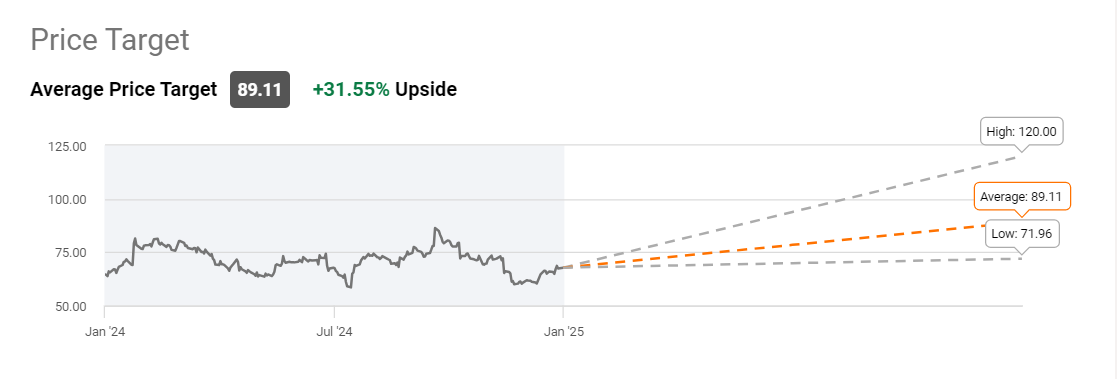

Analysts’ Price Targets: Promising Upside Potential

Uber’s stock price is currently around 68, while according to seekingalpha.com, the lowest analyst price

target is 71.96. Moreover, the average price target is 89.11, or roughly 31% upside from current levels.

This is a very reassuring price target range. If we use the most optimistic projection (120 USD),

the upside of the trade could be as high as 75%, but let’s be conservative and aim for an average – 31%.

Uber Stock Valuation: Growth Outpacing the S&P 500

According to finviz.com, Uber’s forward PE ratio is high—28.48. However, EPS in 2024 increased by 109%, while 2025 earnings are expected to increase by 30.67%. Using those, we can calculate the expected PEG ratio for 2025 to be 0.93. Just as a comparison, according to State Street Global Advisors, S&P500’s forward PE ratio is 24.24, with earnings growth in 2025 expected to come at 13.71% for a PEG ratio of 1.77.

In our opinion, while Uber is not a value stock, it is still very cheap relative to the S&P500 as the expected growth in earnings is more than two times higher, while the forward PE ratio is only 20% higher.

Ownership and Short Interest: A Strong Foundation

Uber nails both those parameters as well. As reported by finviz.com, insider and institutional ownership combine for 84% of the float, comfortably above our 70% target rate. Also, the short float is only 2.6% of the float. Yes, institutions love Uber, and practically nobody is short the stock. While our analysis indicates that Uber is potentially a very good investment, it is important to disclose that the company faces challenges and threats to its business model.

Key Risks to Consider: Regulatory and Technological Challenges

Regulatory Risks

One of those challenges is regulatory—the company could be subject to new labor regulations in the many locations it operates. While this is unlikely to be a big problem with the new Trump administration, the company is also subject to state regulations.

Also, Uber is a largely multinational company nowadays—50 % of its revenue comes outside of the US. That adds another layer of regulatory risks that could negatively impact the company.

Autonomous Driving: A Double-Edged Sword

Another risk is the emergence of autonomous driving. Uber, Tesla, and Google are a few companies working on autonomous driving. While autonomous driving has made tremendous progress over the last several years, it is still not a viable, safe, and reliable mode of transportation.

Technological progress remains unpredictable, and a competitor developing a safe and reliable autonomous driving business model could threaten Uber’s business model. We won’t speculate on this risk’s likelihood but believe analysts have factored it mainly into their expectations and price targets—for now.

Disclaimer

The articles, podcasts, and newsletters from Alaric Securities OOD solely represent the authors’ views affiliated with the company. They do not mean the perspectives of Alaric Securities OOD or any of its subsidiaries or affiliates. They are provided for informative purposes and do not constitute recommendations for or against purchasing or selling security. Digital assets (such as cryptocurrency) or other assets in any account. They are neither research reports nor meant to be the foundation for any investing decisions. Any third-party information given does not represent the views of Alaric Securities OOD or any of its subsidiaries or affiliates. All investments carry risk, including the potential loss of principal, and past success does not assure future success.

Stay Ahead with Alaric Securities Newsletters

Traders and investors don't need more information - they need better information. That’s what we deliver!

Step back from the daily noise. Each issue explores market trends, industry shifts, trading opportunities, and exclusive updates — learn what's shaping the markets, not just what's trending online. Ready to get the edge?